Last week Warc published the June results of its Global Marketing Index, one of the main ways we track current marketing activity in order to benchmark the health of the industry.

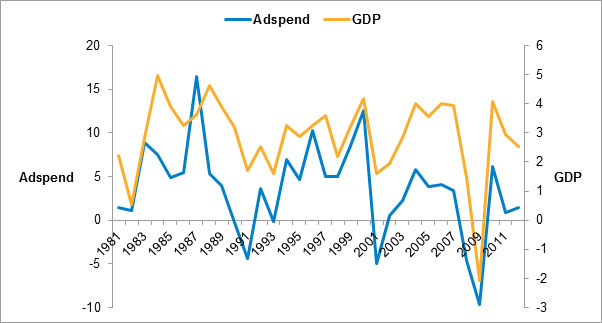

For those of you not familiar with this report, let me provide a bit of background. Back in October 2011, in partnership with World Economics, Warc launched the Global Marketing Index (GMI). Our aim was to provide a unique monthly indicator of the state of the global marketing industry by tracking current conditions among marketers all around the world. The data would also provide useful information for the financial markets relating to the state of global economic activity. Advertising expenditure has traditionally had a clear relationship with GDP, as you can see in the chart below.

Annual % change in global advertising spend vs GDP (at constant 2005 prices)

Notes: Global adspend % change calculated based on PPP totals. Please note that chart axes operate on different scales

Source: Warc Data (global adspend); IMF (GDP)

From the start, a big thing for us was the issue of 'current': all too often the lag between the data collection and release is too long and by the time you actually publish the results they're out of date. That's why our report of results is released just four days after the close of the panel to ensure timeliness. Our 1,200+ strong global marketing panel was recruited from Warc's database of marketing people working for brand owners, media owners, creative and media agencies and other organisations serving the marketing industry.

Now in its third year, we have a solid set of trended data for analysis that really shows the way that industry sentiment is shifting. The GMI quizzes the global panel on current trading conditions, marketing budgets, media allocation within those marketing budgets and staffing levels. Results can also be viewed as an overall headline number – the appropriately named 'headline GMI'.

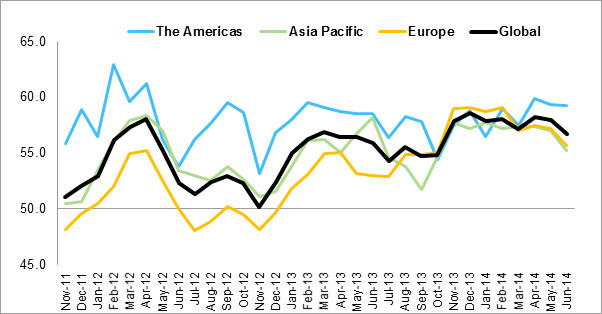

The chart below shows the latest headline GMI data across the four featured regions. A reading above 50 indicates generally improving conditions, while a reading below 50 indicates generally declining conditions. The further the index is from the amount that would indicate 'no change' (50 points), the greater the rate of change indicated.

Headline GMI results by region

Notes: Combines data for trading conditions, marketing budgets and staffing

Above 50.0 = generally improving; Below 50.0 = generally declining

Source: Warc Data (Global Marketing Index)

If we look at the headline GMI in the early months, we can see that the readings for each region were fairly divergent, with the Americas ranking the most positive, while growth in Asia Pacific was more muted and Europe experienced deteriorating business conditions. The chart shows sharp dips for all regions in June and November 2012, largely due to various macroeconomic factors – the eurozone crisis, the prospect of a slowdown in China and the looming 'fiscal cliff' in the US. By early 2013 the outlook was improving for all regions and since the end of last year has remained fairly consistent, with values for each region converging as the economic outlook stabilised.

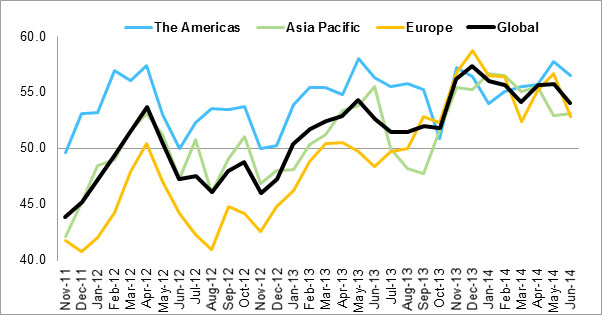

Within this, the component index for marketing budgets shows a lesser degree of optimism long-term, and is resonant of the cautious approach that advertisers have been taking in the wake of the global recession.

Marketing budgets by region

Notes: Above 50.0 = generally improving; Below 50.0 = generally declining

Source: Warc Data (Global Marketing Index)

While panellists in the Americas have typically been the most confident about increasing budgeted spend, the index has been consistently tracking low to mid fifties rather than the more bullish headline GMI which recorded mid to late fifties and rarely dipped to neutral sentiment (index value of 50). So, while consistently improving general trading conditions and employment bolstered the headline indicator, this confidence was not being translated into budgeted marketing dollars.

The same is true of the other featured regions, with advertisers reluctant to commit increased spend during periods of economic volatility. Not surprisingly, Europe was worst hit as key countries struggled to emerge from recession. But, similarly to the headline GMI, since the end of 2013 the index of marketing budgets has stabilised and moved firmly into positive territory for all regions.

In other words, according to the GMI, things are looking up for both the advertising industry and the global economy as a whole.

Would you like to join Warc's global marketing panel? We're always looking to add new recruits – so please don't hesitate to register via our website or find out more about the GMI.