A new Global Ad Trends report explores the issue of media inflation and the challenge of finding both cost-efficient and campaign-effective incremental reach elsewhere.

The importance of reach is well-understood among marketers. As explained in WARC’s recently-updated Anatomy of Effectiveness whitepaper, the work of Professor Byron Sharp, Les Binet, Peter Field and others has highlighted the importance of brand and penetration growth. Yet maintaining campaign reach in a fragmented media market is a growing challenge.

TV remains a pre-eminent channel for delivering mass, cost-efficient reach, but its share of total media consumption is declining, particularly among younger audiences.

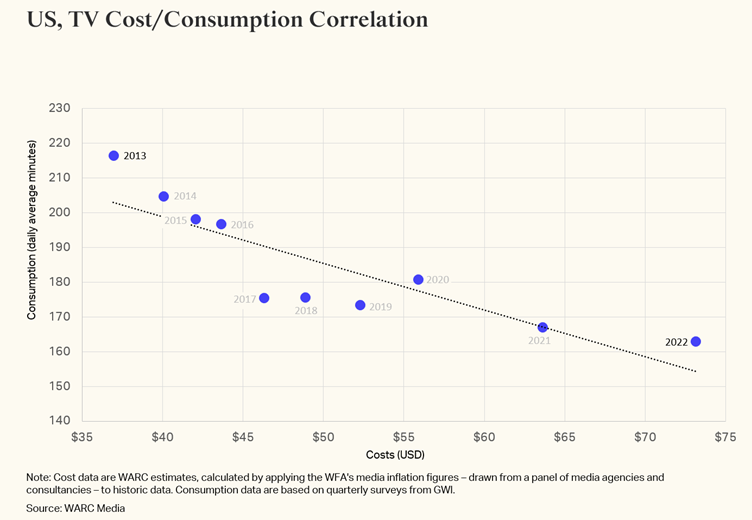

In 2013, linear TV represented 37.9% of daily media consumption in North America, across more than 125,000 16–64-year-olds surveyed by GWI; by 2022, that percentage is forecast to have fallen by a third to 24.5%, albeit in the context of increased total cross-media consumption. In the case of 16–24-year-olds, linear TV will only account for 15.5% of total daily consumption this year.

Furthermore, TV costs have spiked since the pandemic, meaning brands must spend more to maintain previous levels of reach and exposure to target audiences. Globally, TV CPMs (cost per thousand) have increased 31.2% since 2019 – the highest leap in more than two decades – and are up 9.9% year-on-year in 2022, according to WARC Media data. In the US, TV CPMs are forecast to reach $73.14 in 2022, an increase of 40.0% on pre-COVID costs.

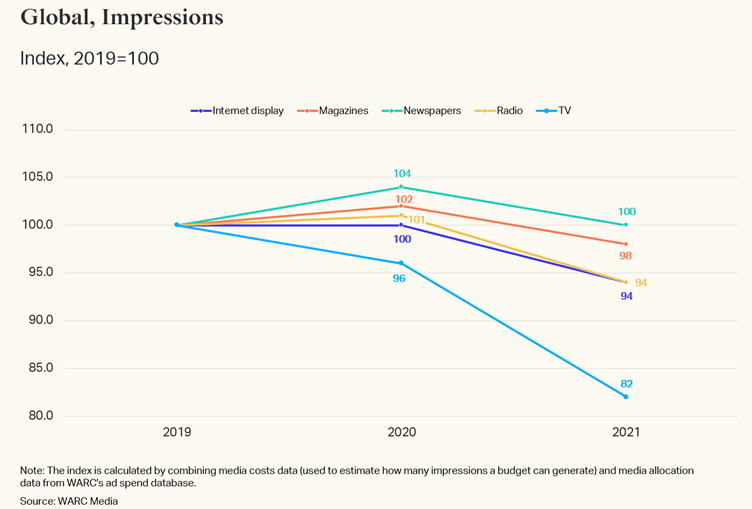

For some categories the impact is heightened. According to WARC Media data, advertisers in the food category spent on average 79.8% of their budgets on TV media in 2019. As demonstrated by this data point, if they were to have maintained that same level of investment, by 2021 the volume of impressions they could expect to gain would have decreased by 18 percentage points.

Of course, the concept of ‘linear TV’ itself is evolving – parts of the addressable and connected TV landscape are, strictly speaking, linear. Yet perceptions of a correlation between declining linear television viewership and rising TV media costs is encouraging advertisers to pursue incremental reach elsewhere, with audio-visual channels – from online video to social media – the favoured alternative for many.

However, the efficiency of delivering reach via non-TV channels is being threatened by rising costs across the media ecosystem. Furthermore, attention research is questioning the effectiveness of pursuing incremental reach away from brand-safe TV screens.

Digital media is becoming more expensive

Price pressure is being felt across the online media landscape.

Data from marketing platform Skai show that paid social CPMs increased by 33% between the fourth quarters in 2019 and 2021. The rise in social costs has been further exacerbated by data privacy trends and Apple’s ATT policy, which has weakened mobile ad targeting, meaning advertisers may have to spend more to reach their target users.

Many consumer goods manufacturers have turned to retail media as a means of driving purchases with in-market shoppers. While Amazon has led the way in the development of an ad sales business, omnichannel retailers including Walmart, Kroger and Target also have fast-growing media arms.

However, the growing popularity of retail media formats is pushing up the cost of advertising on platforms like Amazon. Data from Perpetua, WARC’s sister company, shows rising CPCs across Amazon’s Sponsored Products (+25%), Sponsored Brands (+10%) and Sponsored Display (+120%) formats between Q1 2021 and Q1 2022. (Read WARC Digital Commerce’s latest report on how to win on Amazon).

Online video costs are growing, too

Brands have enjoyed some success by using on-demand and OTT video as a means of incremental reach.

Indeed, when reporting the results of its first post-Nielsen measurement project with iSpot.tv, NBCUniversal recommended that advertisers weight TV plans to include at least 30% OTT impressions to maximise incremental reach and optimise frequency management.

Similarly, early data from CFlight, the UK’s unified TV advertising metric based on a tool created by NBCUniversal, shows a “clear relationship” between BVOD share and incremental reach. Among campaigns that bought 200-plus linear ratings, BVOD added an average incremental reach of 0.5% (260,000 people) for every 1% of campaign ratings. Where BVOD accounted for 5% of ratings, average incremental reach was two million.

A study published in 2020 by UK insurer Direct Line Group (DLG) found it only needed to spend £0.60 on YouTube to achieve the same attentive and viewable incremental reach that would have cost £1 with linear TV, and £0.70 in the case of broadcaster video on-demand (BVOD).

Yet marketers must also be wary of rising costs in these channels.

While not matching the increases seen in linear TV, the latest data from the World Federation of Advertisers (WFA) forecasts average inflation of 9.9% for ‘advanced TV’ in the US in 2022, incorporating addressable ads in linear TV, connected TV streaming and VOD platforms. In comparison, inflation for advanced TV ad channels stood at 3.0% in 2020.

A similar picture emerges in social video: the WFA reported high levels of price inflation in 2021, including in Australia (+17.8%), China (+6.6%), Germany (+13.7%), Japan (+9.3%) and the UK (+7.8%).

Adjusting for attention

The opportunity for advertisers to gain cost-efficient incremental reach through online video channels is further complicated by issues around viewer attention.

A study by Ebiquity discovered that, when factoring in criteria such as viewability and dwell times, a 30-second TV spot delivers the highest number of attentive seconds per 1,000 impressions, followed by 15/20-second ads on YouTube. Facebook’s in-feed format and desktop display ads perform significantly worse.

Ebiquity recently interrogated claims made by Facebook to an adult health brand in Canada, that it could completely replace TV in the advertiser’s media plans. Whilst not stopping TV support altogether, the advertiser switched a significant amount of spend to Facebook. Yet econometric modelling concluded that ROI on Facebook was nearly four times lower than TV.

To quote Professor Karen-Nelson Field, all media channels and formats are restricted by ‘elasticity’ in the attention they can deliver, no matter how compelling the creative. Incremental reach will be limited by this elasticity.

Everything’s not lost

That’s not to say there are no bargains to be had. Offline channels in particular are under-utilised in the pursuit of incremental reach, and have not witnessed the same levels of price inflation since 2019.

Take radio, for example: in Australia, the cost of radio media in 2022 remains 4.7% below pre-pandemic levels, while it is 3.6% lower in the US. A similar picture emerges in OOH, encompassing both static and digital panels: in the UK, outdoor media costs are 3.1% lower than before COVID-19, while in the US OOH is 5.8% cheaper than it was in 2019.

Malcolm Devoy, Chief Strategy Officer EMEA at PHD Media, recommends marketers look beyond efficiency metrics, whether total cost or attention-adjusted CPMs. Instead, he advocates optimising towards ‘weekly attention-adjusted reach’, which combines attention-adjusted costs with reach curves and calculates the speed with which a channel builds reach.

This, argues Devoy, transforms reach into an effectiveness metric that can be better aligned with campaign goals.

Tricky outlook

Yes, in many markets, linear TV reach is slowly being eroded, especially when it comes to younger audiences. And yes, TV costs have risen at a striking rate since the pandemic. As long as these patterns continue, advertisers will look elsewhere to drive the incremental reach they perceive they are losing in TV.

Yet those alternative channels – whether social media or OTT – have also seen significant price inflation. Furthermore, in the case of mobile-centric formats, they may be delivering poorer levels of attention when compared with TV advertising.

The pursuit of incremental reach is completely understandable, but the devil is in the detail. A great place to start is WARC’s recently-updated Evidence report, How do I build incremental reach?. Nonetheless, this is a highly-complex issue and is likely to keep media planners occupied for some time to come.

Click here to read Global Ad Trends: The rising cost of incremental reach