The platform’s e-commerce domination may be stifling hopes of a multifaceted worldwide retail media market, a new Global Ad Trends report finds.

At the recent IAB UK Digital Upfronts in London, a panellist quoted WARC contributor Colin Lewis when reflecting on the changing power dynamics in retail media between brands and merchants. “Who is taking who out for lunch?” It’s a question worth asking.

A prevailing narrative in the advertising industry tells us that brands are in the driving seat. They spend the money that makes the media world go round, and the sell-side must work hard to win its share of the spoils. When Procter & Gamble CMO Marc Pritchard gives agencies and publishers a year to fix the “crappy media supply chain”, everyone stands to attention and looks busy.

Except, of course, that isn’t how it works.

Six years on from Pritchard’s call to arms, the Association of National Advertisers continues to find $20bn of digital ad spend is being “wasted” by murky trading methods and murkier content – with $13bn alone swallowed up by the scourge du jour, ‘Made For Advertising’ websites (read WARC’s excellent Future of Programmatic report for more on this).

As long as advertisers continue to target audiences wherever they may travel across the web, there is little hope for systemic change. Even The New York Times, one of the few publishers to emerge mostly unscathed from the collapse in publishing advertising, has been forced to reopen the door to open exchange programmatic ads after a four-year hiatus.

Brands can withhold investment if they don’t like what they see, of course. But – as we saw with the ad boycott of Facebook in 2020 – such measures are unlikely to have a material impact on the bottom line in the digital world, where platforms have millions of advertisers of all shapes and sizes across the world to soften the blow.

Put simply, the forces underpinning digital advertising appear to have become too powerful for brands to rein in, no matter how big a budget they can bring to bear.

It’s Amazon’s world and brands have to live in it

All of which brings me back to retail media.

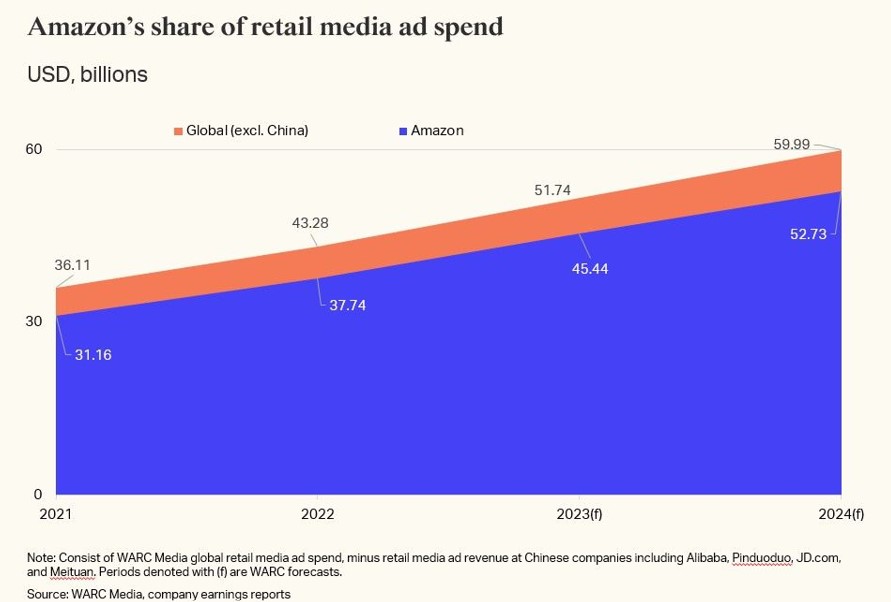

For all the hype about the growth of the commerce media, the latest Global Ad Trends report from WARC Media (Retail media’s path to consolidation) suggests that Amazon has already achieved something of a stranglehold on the market.

WARC Media estimates that Amazon’s share of worldwide retail media investment (excluding China) in 2023 will stand at 87.8%. And that dominance is likely to grow, with Amazon’s ad revenue set to expand twice as quickly (+20.4%) than the overall global retail media market (+10.5%) in 2024.

Of the additional $8.3bn to be spent on retail media in 2024 in all markets bar China, $7.3bn will go to Amazon – leaving the remaining players, from Walmart and Target to Instacart and Uber, to scrap over the remaining $1bn.

Much as we saw with Google and the rise of paid search, and then Facebook in social media, Amazon has been able to harness a nascent advertising channel and continue to ride the rocket as it takes off.

There will be room for some others, of course: Walmart in particular is developing into a multibillion-dollar ad business. However, in a market lacking standards in areas such as measurement and creative formats, a media owner as large as Amazon will possess significant incumbency advantages.

Wake up and smell the coffee

None of this is necessarily a problem for brands; they have benefited from the reach and data provided by other Big Tech walled gardens, no matter their monopolistic position. The difference with Amazon may lie in the power that platform has over conversion in endemic categories.

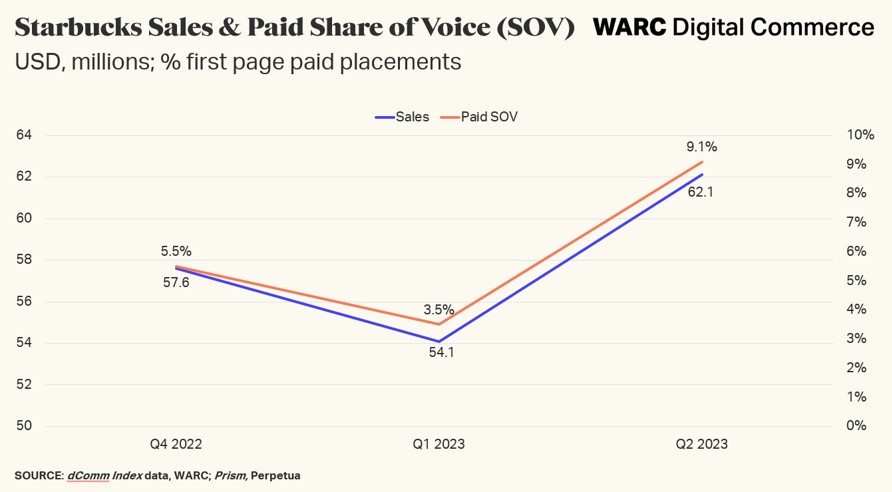

An analysis of Starbucks’ retail media strategy by WARC Digital Commerce found a correlation between paid share of voice (SOV) on Amazon (i.e. the share of first page placements occupied by a brand in its category, in this case coffee and tea) and product sales. A one percentage point change in Starbucks’ paid SOV was typically followed by a c.$1.6m increase or decline in Amazon sales.

Similarly, analysis of WARC’s dComm Index in the Global Ad Trends report found that investment in paid retail media can boost organic search results – which, in turn, is often a better indicator of brand purchase intent.

Cases like these appear to give credence to concerns that platforms like Amazon are becoming “pay to play” environments for advertisers, where paid media is required to maintain visibility and access to customer data. It is one of a number of issues listed in the Federal Trade Commission’s ongoing legal battle with Amazon.

And that – to return to Colin Lewis’s earlier comment – raises questions about who is buying who lunch in the retail media world. After all, this is a market where Amazon can demand $100m-plus commitments from agencies for its latest ad venture in video media. There is a danger that the relationship becomes too lop-sided, with Amazon holding all the cards.

That unparalleled, full-funnel package of customer data and mass reach may taste good to advertisers, but they’ll be left paying the bill in every sense.