As marketing budgets rebound in 2024, uncertainty swirls around where best to direct investments in media, the role of AI in planning, and how to assess media quality.

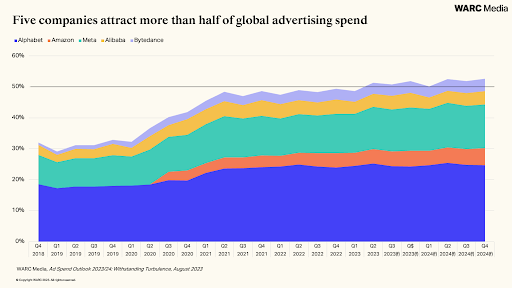

After a challenging 2023, WARC Media predicts global advertising spend will double its growth in 2024, with spend expected to top $1 trillion for the first time. The big winners from this are the major tech companies, five of which now account for more than half of the total money spent on advertising.

Key to the growth of these companies over the last 12 months has been the adoption of AI, which has made an enormous leap forward in 2023. From Amazon’s ‘Q’, to Google’s ‘Performance Max’, it would appear that many of the major players have pegged future ad revenue growth to their AI-based advertising solutions.

While this approach is paying dividends, the growth of AI raises difficult questions about the ideal relationship between humans and machines; the power of platforms; and the future of news, information and entertainment on the open internet.

Without proper guardrails in place, there are concerns that the open web will soon see a huge uptick in AI-generated misinformation and disinformation. If the quality of the open web is undermined in this way, then brands may be increasingly reluctant to advertise because of brand safety and ad fraud concerns. This is a particular worry with several major elections due to take place this year.

As politics temporarily engulfs culture, and the threat of low-quality AI-generated content looms large, media environments that can offer suitable guarantees around brand safety will take on extra value.

A case in point is linear TV - which despite dropping off marketers’ lists of ‘preferred’ marketing channels - remains uniquely placed to deliver high impact advertising to a mass audience, and critically, in a brand safe environment.

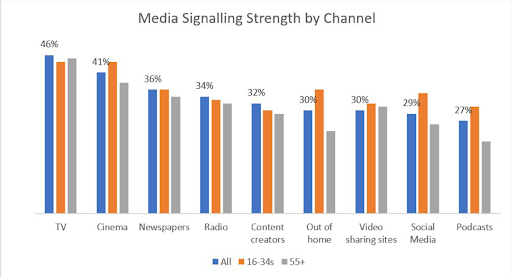

As recent research has shown, TV also carries a ‘signal strength’ unmatched by other channels, meaning it is more likely to leave a positive impact on consumers' perceptions of a brand.

Of course, signal strength is just one part of a much larger and evolving discussion about how we quantify media quality.

While many have pinned their hopes on attention measurement, there are methodological and evidence-based barriers that remain.

Ironically, the more we learn about attention the more we recognise the need for other, complementary measures that give us a more rounded view of media quality. Take ‘Right Reach’, for example, a media quality metric developed by Zenith that examines different contextual signals, as well as attention, to improve channel planning.

The need to find new models for measuring media quality takes on extra importance in the era of AI. Not only because of the dangers posed by AI-generated content, but because automation is driving down the costs of many agencies’ core services (e.g. campaign management, content production), prompting a pivot to new sources of value.

These are just some of the trends we examine in this year’s Future of Media report, which focuses on the question of how advertisers can plan for quality in the era of AI.

WARC subscribers can read the full report here. If you’re not a subscriber, then fill out your details here to obtain a copy of the sample report.