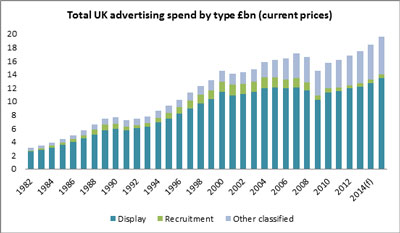

During the next two years, total UK advertising expenditure is forecast to accelerate way beyond levels recorded prior to the financial crisis, according to the latest data from the Advertising Association/Warc Expenditure Report released last week. This is no small feat, as the recession in 2008/9 was the sharpest since the AA/Warc began collecting quarterly adspend data back in 1982.

But looking at the trends in context, we can see that the UK ad market is a long-term success story. Other than the recent downturn and smaller dips around the global recession in the early 1990s and the dotcom crash in 2001, the growth trajectory for UK adspend has been impressive. Indeed, the impact of the three big recessions faced by the UK, seem mere blips in the sector's steady expansion.

Note: Total adspend excludes TV sponsorship and radio branded content

Source: AA/Warc Expenditure Report.

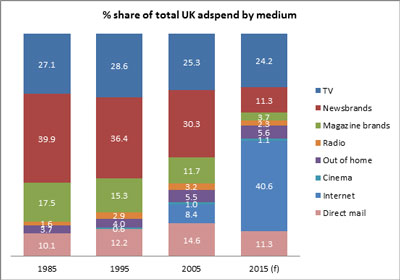

That said, these topline numbers that track annual total adspend for all main media, shield a big shift in media budget allocation. In the chart below, we lay bare the seismic impact of the digital revolution on the UK advertising landscape.

Note: TV data is for spot advertising only. Radio data excludes branded content. Newsbrands and magazine brands are print only. Internet adspend includes digital revenues for newsbrands and magazine brands, broadcaster VOD and radio station websites.

Source: AA/Warc Expenditure Report.

Looking at the share of adspend by medium in 1985, we can see that print adspend for newsbrands (both national and regional) took a majority 40% share, followed by TV (27%) and magazine brands (18%). Ten years later in 1995, small gains for TV, direct mail, radio and out of home had caused print to lose share but it still dominated the market.

Then came the digital revolution. Internet was starting to make inroads by the early 2000s and in 2005 had achieved an 8% share of total UK adspend, largely at the expense of the print sector. The classified advertising sector – the traditional mainstay of print – was starting to move online.

Over the next 10 years, advertisers shifted budgets online at an unprecedented rate. By 2015, AA/Warc estimates predict that internet will take a dominant 41% share of total UK adspend, while print will account for just 15% of total spend altogether. Though newsbrands and magazine brands are also expected to boost their digital revenues in the coming years – the medium may have changed but the format is still very much alive.

And despite the massive growth of internet adspend, some media have remained consistent throughout the 30 year period. Look at the top and bottom sections of the chart above: both TV and direct mail have held share, while out of home has boosted revenues throughout. In other words, the UK ad market is evolving rapidly with the shift to digital – but it's far too early to call the death of the traditional media.

To find out more about subscribing to the AA/Warc Expenditure Report please visit the website or contact Suzy Young for additional information. This blog post was originally published on MediaTel.co.uk.