WARC’s latest Global Ad Trends has found that cinema growth will outpace the global ad market this year, while UK admissions were at a record high in 2018. Netflix’s rise appears to have had little impact on the allure of the silver screen, writes WARC Data's Managing Editor, James McDonald.

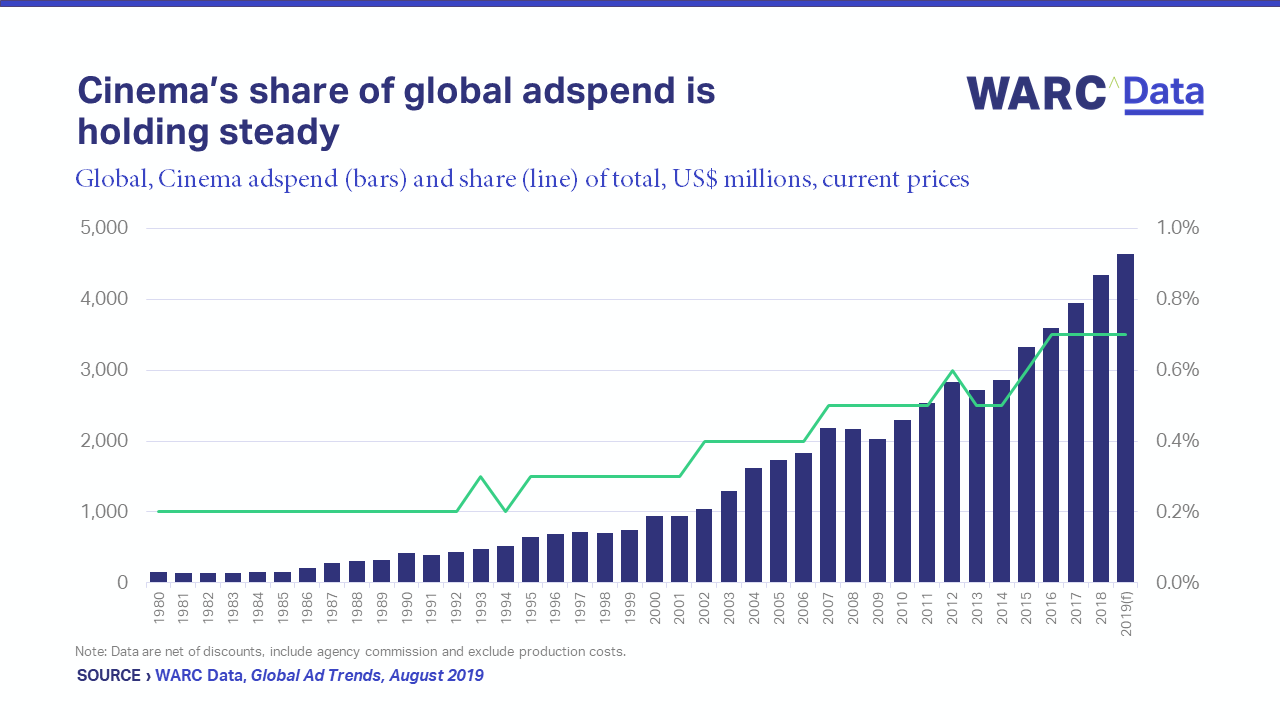

Investment in cinema advertising is set to rise for the sixth consecutive year in 2019, to a total of $4.6bn worldwide. Further, the projected growth of 6.8% is ahead of WARC’s all media forecast of 4.6% and is behind only internet (+13.2%). This means that, on current trends, cinema will be the only ad medium other than internet not to lose share of global advertising spend this year.

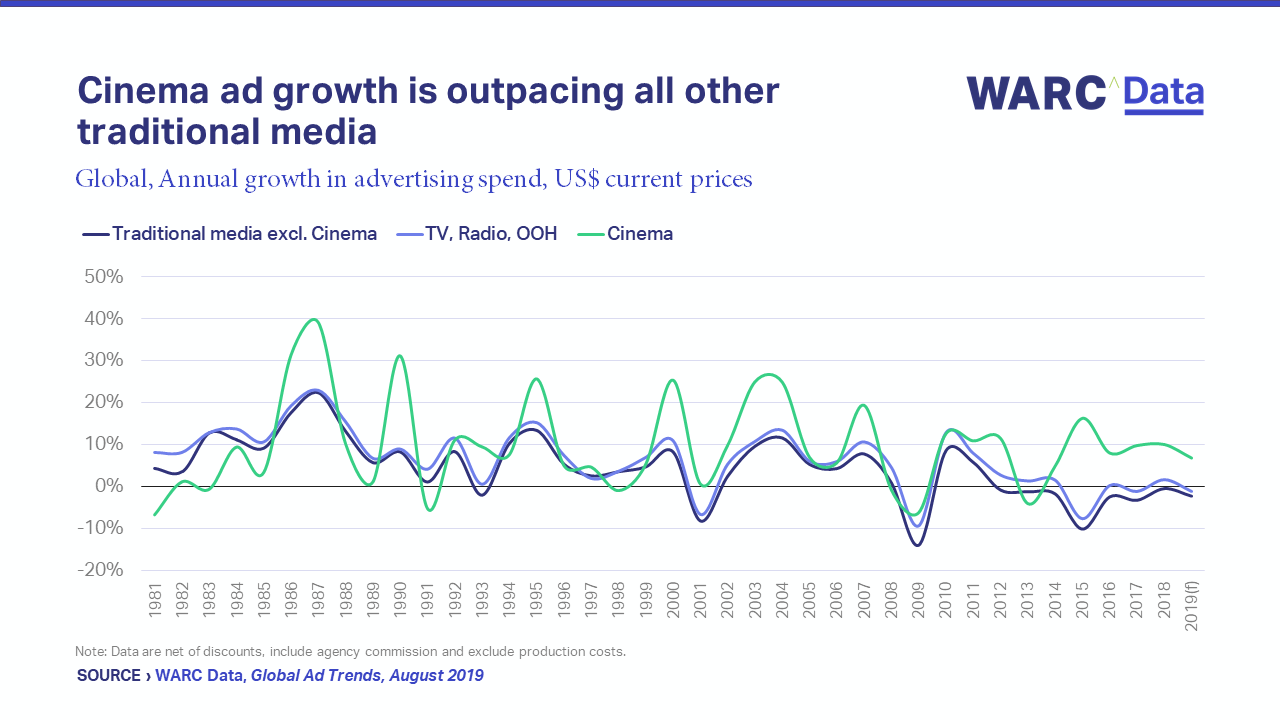

While small at 0.7%, cinema’s share of global adspend has slowly ticked upwards over the last four decades, and has dipped only twice since 1980 – once in 1994 and again in 2013. And when compared to other traditional media, cinema ad growth has generally tracked ahead of the pack since 1981, but consistently so since 2014.

In a multichannel age, where all conceivable kinds of content are available to us at any moment, anywhere, the romantic in me finds it heartening that a medium more than a century old is seen to be thriving.

Netflix has yet to hit Western box offices, and China is booming

Cinema admissions in the UK reached a record high in 2018, at 177m. This equated to £1.43 ($1.91) in advertiser spend per admission last year, up from 18 pence in 1980 and a penny in 1961.

North American admissions were up 5% to 1.6bn (43 cents spent per admission), according to the Motion Picture Association of America (MPAA), while the UNIC recorded a similar footfall (1.3bn, with 75 cents spent on ads per admission) in Europe last year.

But China is the real growth engine. Admissions rose by almost 6% to 1.72bn in 2018, equating to $0.91 in advertiser spend per visit. This is up from 12 cents just five years earlier. Further, IHS figures suggest that the number of cinema screens in China increased by 9,303 last year alone, or 26 per day on average.

Ancillary research by the European Audiovisual Council, published this month, shows that China is now the largest export market for European films, while PwC believes that China will become the largest cinema market in 2020, with box office receipts totaling $12.3bn – ahead of the US on $11.9bn.

China is already the largest cinema ad market, with RMB11.9bn (US$1.8bn) expected to be spent this year. This equates to a 47.3% share of global cinema adspend when measured in Purchasing Power Parity terms, which removes fluctuations in exchange rates. By this measure, we see that China has accounted for three quarters (74.9%) of global growth in cinema ad investment since 2015, on average, and we expect it to contribute 87.4% towards growth this year.

Consumers now spend more on streaming movies than visiting the cinema

Despite healthy box office takings, data from IHS show that the amount consumers spend on digital home entertainment, including on online subscriptions such as Netflix, surpassed the amount spent at the cinema globally for the first-time last year ($42.6bn versus $41.1bn). This landmark had already been reached in the US during 2015.

Over the course of an average year, a Netflix subscription will cost a consumer US$113.16. This compares to the $45.55 a North American will spend at the cinema, with the equivalent figures for the UK and the EU at $25.13 and $11.04 respectively.

A US moviegoer visited the cinema five times on average in 2018, which roughly equates to 263m Americans seeing a movie every two months. But with almost three-quarters (74%) of Americans now using an online subscription to watch a film at least 2–3 times each month, viewership in the living room may have now reached parity with – if not exceeded – the silver screen.

But the experiential nature of cinema places it in a different bracket to OTT services such as Netflix, which instead occupy a similar space to traditional TV. This, coupled with the exclusivity of box office hits – particularly franchises – should ensure any downward pressure from such services is minimal in the short term.

Attentive audiences ensure cinema ads get noticed in a brand safe environment, and younger attendees have a positive affinity with the medium

Cinema offers advertisers access to younger, more affluent audiences who have an affinity for the medium. This enables ads to be screened in a brand safe environment where they will be noticed, often in a location that is close to a retail outlet and, by extension, a point of purchase (41% of consumers surveyed by DCM stated that they went for food or drink after seeing a movie).

Captive audiences viewing high-quality ads in an emotional atmosphere is a draw for advertisers. Research by Ebiquity has found that Cinema outperforms all other media at triggering an emotional response, guaranteeing a safe environment, and getting ads noticed.

This is reinforced by the IPA’s TouchPoints 6, which finds that cinema delivers a more positive emotional experience than any other AV channel. Eighty four percent of time spent at the cinema is associated with positive emotions for 16+ adults, compared to 60-65% for live TV, longform VOD and short online video.

Kantar Millward Brown has also found that among 'Gen Z' (16–19 year-olds), cinema is the most popular traditional advertising medium, with 59% feeling 'positive’ about it (compared to 34% for print, 38% for TV and 50% for outdoor).

With all this in mind, are brands under-investing in cinema? New net adspend figures from WARC and Nielsen suggest this may be the case.

In the US, cinema draws less than half a percent (0.4%) of all media spend across 19 product verticals on average. Seven product categories allocate more than this, most notably food, for which cinema accounts for 1.5% of all media spend. But this is far below the 2.7% DCM recommends, with the industry body noting that some sectors, like travel & tourism, see optimal levels of campaign ROI when allocating as much as 11%.

You can read a free sample of this month’s Global Ad Trends by following this link.