WARC Media’s Celeste Huang shares insights from the latest Global Ad Trends report on connected TV.

When I was an advertising student at university, the teacher once gave us a list of common acronyms used in TV media to memorise and be tested on by the end of the semester. Trying to grasp those all-caps letters was a real challenge: OTT, VOD, CTV, GRP, ROAS, etc. (if you are interested, here’s a great WARC guide on all the advanced TV acronyms)… what do all these words mean?! I scrambled down the full terms during the test in a rush to get it done, not knowing that years later I will be editing a Global Ad Trends report on the current state of connected TV (CTV) and actually enjoying discovering this complicated and ever-changing sector.

Nowadays, the acronyms in our industry seem to only be growing more complicated. The talk around CTV has become louder and louder. What is the CTV we are referring to? Have we come a long way and where are we with it?

CTV – defined here as professionally produced video consumed through a TV device – is a blurring field with many overlapping and intertwining definitions. The industry is yet to agree on a term to describe all – and maybe that time will never come.

However, one thing became clear as we interviewed industry experts for this report: CTV is very much TV. It’s an evolution more than a revolution. At one point, CTV was viewed as a completely new digital channel that could break through and win ad dollars that TV couldn’t touch before. That hasn’t happened yet.

CTV is going through an inevitable growing phase as linear TV ad spend dwindles and viewership migrates, new ad opportunities arise and CTV ad technology matures. This in turn will help overall TV health and growth – especially in the face of competing search, retail media and short-form video-powered social channels that take a bigger share of total ad spend.

However, when taking another, deeper look at CTV, it’s not difficult to see that it’s still in an early stage, and with the early stage come challenges: there is much to overcome to persuade marketers of its effectiveness and therefore maintain its growth momentum.

Eyeball migration drives CTV growth

CTV’s new opportunities lie in the very fact that how people consume TV is changing. As linear TV viewership declines and more people join the cord-cutting way of living, and the cost-of-living crisis results in more people staying at home streaming, new offerings are drawing in consumers, and advertisers are seeing opportunities to reach those individuals.

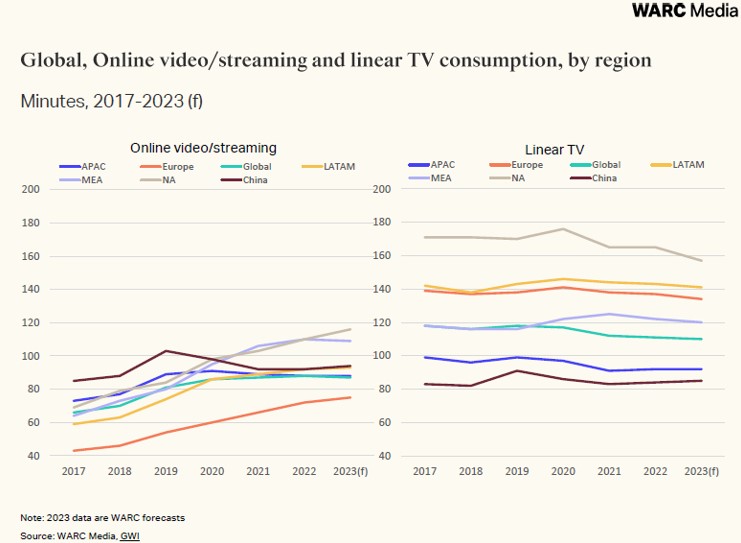

Although consumption differs greatly by region, an upward shift is happening around the world. In regions like Asia Pacific and China, where mobile penetration is historically high, online streaming has drawn level with linear TV consumption. As a result, countries like Thailand and Indonesia see more ad spend on premium video (defined as linear TV, broadcast video-on-demand, and over-the-top including YouTube) than pureplay Internet formats.

(Click on the chart to access WARC Media/GWI dashboard data)

Europe and North America see a strong uplift in time spent on online video as well, with the US experiencing a 68% consumption increase since 2017, according to GWI data. And globally, Gen Z is forecast to spend 90 minutes on average on streaming per day, versus 86 minutes on linear TV in 2023.

Note: here streaming means time spent on all the video-on-demand services plus YouTube – see how confusing these TV/video terms can be.

Subscription-based media owners including Netflix, Disney+ and Amazon Prime Video have all turned to building ad-supported tiers in the hope of sustaining subscriptions and diversifying revenue streams. In countries where broadcaster viewership has been heavy, BVOD services are also starting to benefit from shifted attention from consumers.

Consumers are also more receptive to ads: more than half of global consumers who plan to or have cancelled streaming services are supportive of ad-tiers. In the US, viewers spend almost half of their CTV viewing time on ad-supported content. Nonetheless, the rate of ad-supported plan sign-up differs greatly by platform, and engagement on ad-supported services is yet to prove itself.

Ad spend growth is steady yet modest, at the moment

(Click on the chart to access WARC Media dashboard data)

GroupM forecasts CTV ad spend will reach $42.5bn and grow 10.4% over the next five years, a rate that would be envied by many other media channels amid the uncertain macroeconomic climate.

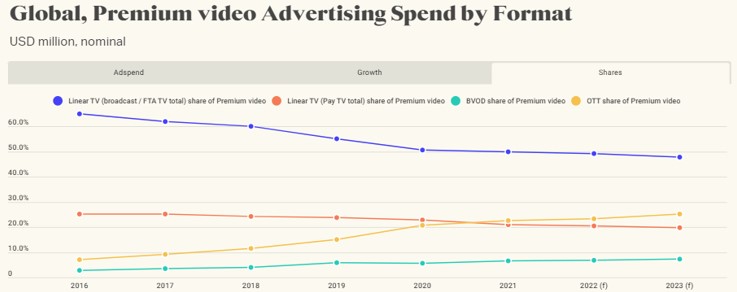

The share of premium video global ad spend, however, has decreased by 14% over the past eight years, according to WARC Media. Online video’s share of total ad spend has increased by 5% since 2016, but this has not been enough to offset a 20% decline in linear TV advertising.

CTV is still largely competing with existing TV budgets and there is still much room for growth. When put side by side with retail media – the channel with the highest growth forecast – the momentum is rather modest.

It’s undeniable that CTV’s incremental reach, addressability, and fast-developing programmatic capabilities enable TV ads to be more versatile. Many advertisers that traditionally exclude TV in their media plan now have a chance to reach TV audiences. Meanwhile, hurdles like low ad-tiers signups, limited ad inventory and fragmented viewings, are one of the many factors that are limiting budget shifting at scale.

There are also challenges like brand safety, ad fraud, lack of transparency and inconsistent measurement to be tackled by the industry as a whole. This doesn’t necessarily denote a fatal defect; it means that (C)TV is evolving, and the trajectory will not be straightforward.

To put it simply, CTV consumption is rising, and time spent overall on TV is still level, if not increasing in many markets. As a result, ad spend is shifting. At the same time, the viewing landscape is fragmented, and so is the sector’s infrastructure. CTV has the potential to continue building on its growth and attract ad dollars outside existing TV budget pools, and maybe, just maybe, with fewer acronyms and a clearer definition.

If you are a WARC Media subscriber, you can read more in the latest Global Ad Trends report, ‘Connected TV’s next episode’, now available here.

Or, request a sample report here.