This week we released our latest International Ad Forecast, taking the pulse of 12 key advertising markets to learn what the future will look like for adspend. In this edition, we have revised our forecast upwards by 1.2pp from October, expecting 2014 advertising expenditure to grow by 5.6% year-on-year in Purchasing Power Parity (PPP) terms – the highest rate of growth since 2010.

PPPs are a good gauge for comparing different markets as they show the rate at which the currency of one country would have to be converted into that of another country to buy the same amount of goods and services in each. A common example is the price of a hamburger: in London, it may cost £2, while in New York the same hamburger may be $4. This would imply a PPP exchange rate of 1 pound to 2 US dollars. Consequently, market exchange rates are taken out of the equation, and a clearer comparison can be made.

But our 5.6% growth forecast for 2014 is before inflation. In real terms, at 2005 prices, this growth amounts to 3.2%. A further rise of 5.3% – 2.7% in real terms – is predicted for 2015.

The outlook is positive for global trading conditions (as reported monthly in our Global Marketing Index), and the greater than expected economic stability globally has also benefited our focus markets. The forecast finds that on a PPP measure accounting for inflation, adspend in 2015 will match that of the historical high of PPP341bn recorded in 2007 before the global economic crisis.

Stimulus provided by major sporting events such as the Sochi Winter Olympics in February and this month’s FIFA World Cup in Brazil have also been factored in.

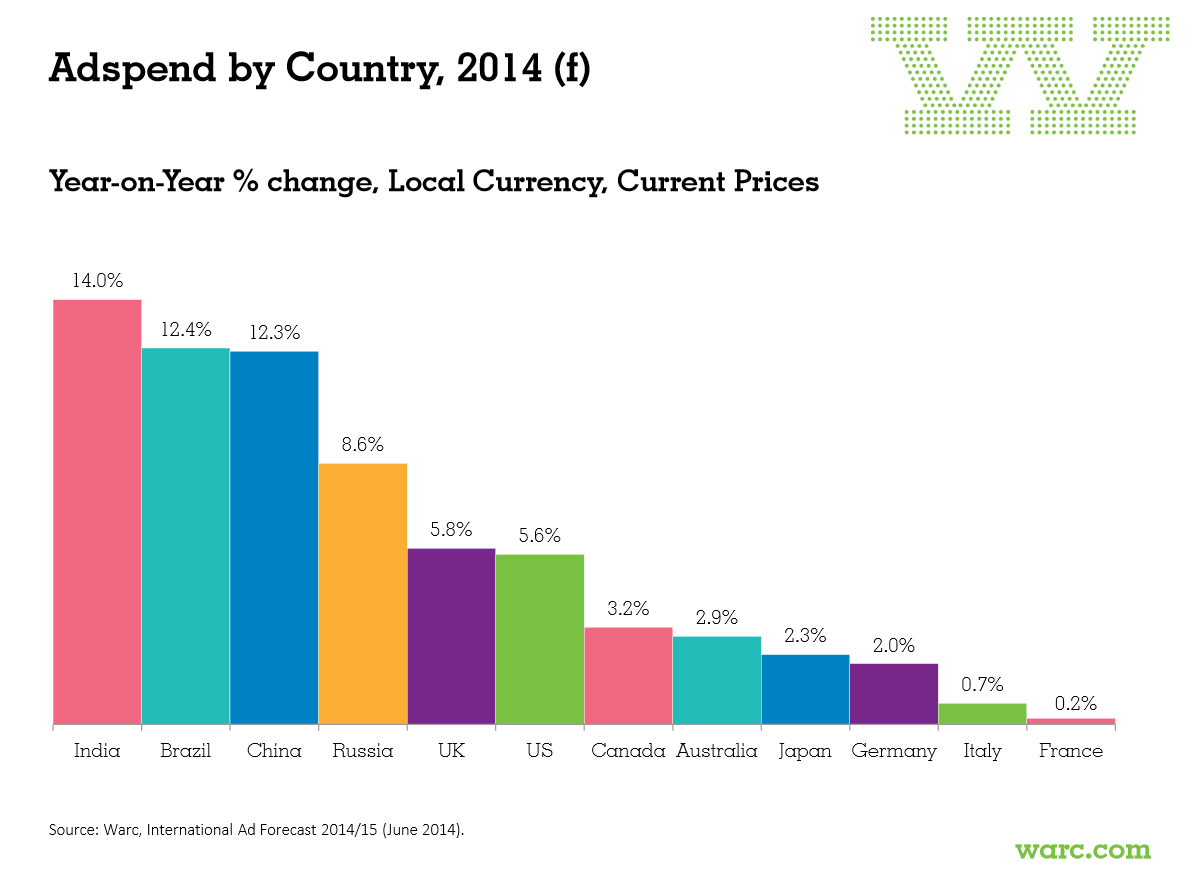

BRIC territories, as would be expected, lead in terms of annual growth at current prices, although this rate of expansion is slowing. Moreover, these markets are subject to high levels of inflation, and, when assessed in real terms, the growth rates are more closely aligned.

India is the fastest growing market before inflation – at 14% year-on-year growth – although this rate dips to a more modest 5.6% in real terms. Brazil, buoyed by the hosting of the FIFA World Cup, is expected to record growth of 12.4% at current prices this year, yet this rate is more than halved to 6.0% in real terms. The country’s growth will then slip to 2.4% in 2015 by this measure. Russia, expected to see annual growth of 8.6% at current prices, will expand by just 2.0% when measured by the constant (a slower rate than the UK and US). And so it is China, now the second-largest advertising market in the world, which will demonstrate the largest growth in real terms this year, at 9.5%.The annualised growth rates above are calculated using local currency, giving the clearest indication on a market-by-market basis. However, when comparing markets with each other, it is again better to use PPPs, which exclude the currency exchange rates that can distort data.

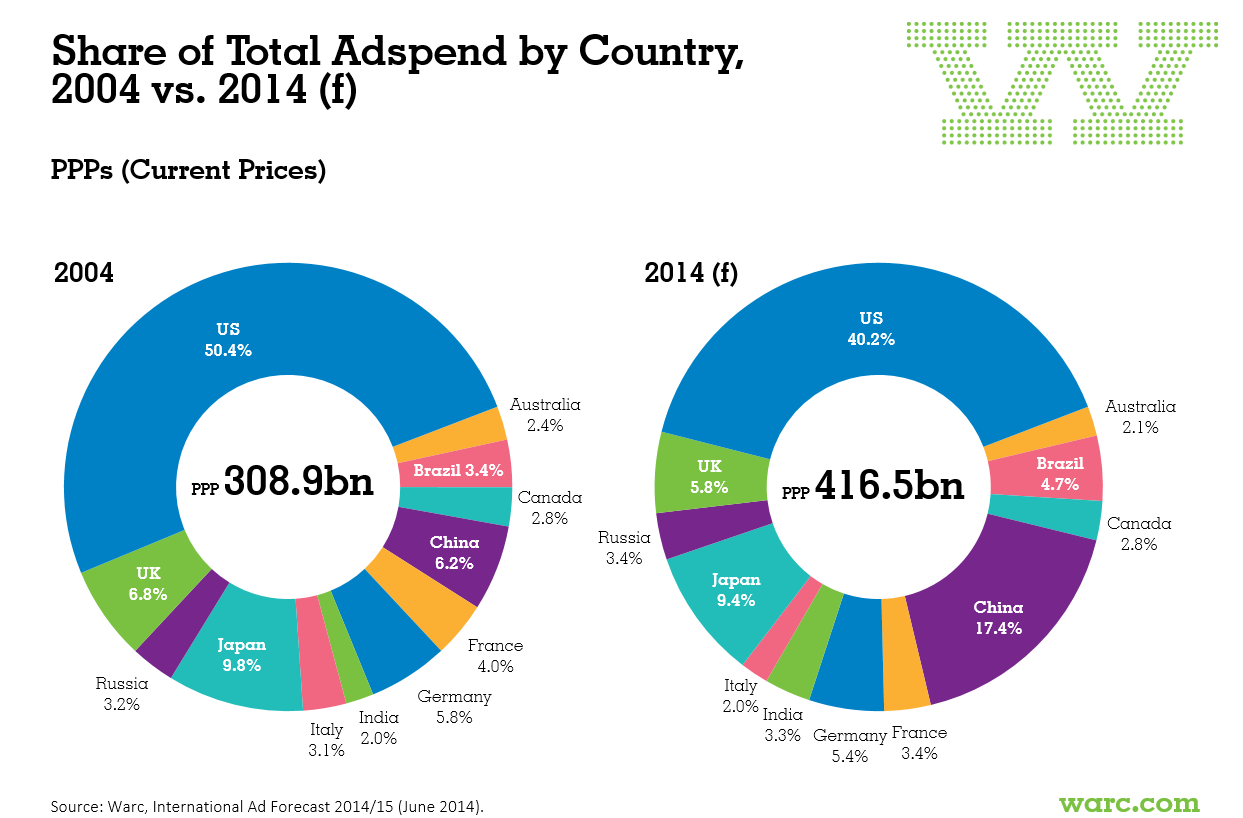

The US will maintain its adspend dominance this year, holding the largest share of the PPP416.5bn advertising expenditure recorded in our 12 markets. Among other things, the US TV, and consequently grand total has benefited from NBC’s coverage of the Sochi Winter Olympics. NBC aired a record 539 hours of Olympic coverage in February, a 21% rise compared to the 2010 Vancouver Winter Olympics which allowed for an estimated 11,000 30 second spots during 2014’s games. The US also has mid-term elections to look forward to this year.

However, the 40.2% share the US commands at present has dropped by some 10.2pp over the last 10 years, largely at the expense of Chinese growth. But the US ad market remains generally robust, and this will be the case for some time to come: we believe that advertising expenditure in America will total $175bn in 2015, a record high.

Subscribers can access the International Ad Forecast summary report and the full dataset via the dedicated page. The forecasts have also been added to our Adspend Database, along with 2013 actuals for 38 countries, with around 50 more to be added over the coming weeks.