Total UK advertising expenditure rose 5.0% year-on-year in Q1 2014, according to the latest data from the Advertising Association/Warc Expenditure Report released last week. We're predicting growth of 6.0% for the year as a whole and a further increase of 6.7% in 2015.

These are the headline figures – but what do they mean for the industry? There is often confusion when it comes to interpreting UK adspend data, because the AA/Warc is just one of the many organisations that release data in this field, and often the figures and forecasts seem very different to those from other sources. One of the main queries I receive at Warc tends to be "Why are your data so different to the numbers I've just seen from insert source organisation here?"

To take a recent example, a new report from a well-known research organisation informed UK marketers that advertising spend via mobile would overtake print spend in newspapers and magazines next year and TV by 2016. Yet, as you can see from the chart below, the new AA/Warc data suggest otherwise – to 2015 at least.

(Click image to enlarge)

Note: Print total includes national and regional and newsbrands and magazine brands. TV includes spot advertising, broadcaster VOD, product placement, advertiser funded programming and other revenues such as interactive fees (e.g. Shazam) and pub TV.

Source: AA/Warc Expenditure Report.

So how does the end user make sense of the different reports available and determine which dataset is going to be most useful for them? To me, there are really three key aspects to consider:

- How are the data collected?

- What is the forecasting methodology?

- How are the different sectors defined?

Invariably, what seem like similar datasets on the surface may be very different once you drill down into the detail. To complicate matters further, there is not a right or wrong answer to any of the above. It's up to the source organisation to ensure that its datasets are transparent so users can determine whether they're comparing like for like or if it's a case of apples and pears.

So let me clarify the AA/Warc methodology here:

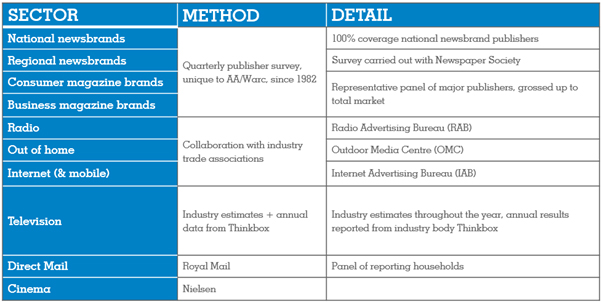

How the AA/Warc collects adspend data

Our remit is to provide comprehensive and accurate advertising expenditure for the benefit of the UK advertising and creative industries. We have to ensure that we are representative of all sectors, unbiased and independent.

The revenue figures collected are before the deduction of agency commission, but after the deduction of all negotiated discounts. With the exception of direct mail, production costs are excluded. The AA/Warc survey started in 1982, so we have quarterly and annual data for 30+ years. The methods of collection for each sector are given in the table below.

(Click image to enlarge)

The AA/Warc forecasting methodology

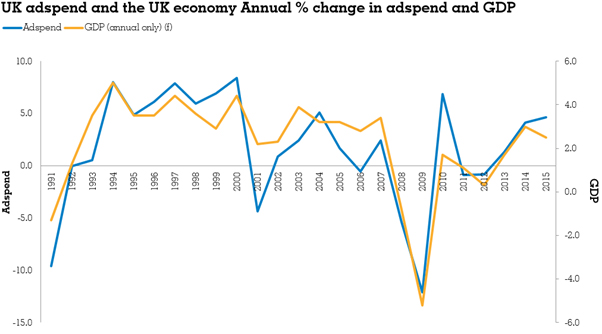

Analysis of data over the past 30 years shows a clear relationship between the annual changes in total UK adspend (excluding recruitment) after adjusting for inflation and annual changes in GDP. In fact, the changes in GDP account for around three quarters of the changes in adspend if the dotcom crash year of 2001 is excluded.

(Click image to enlarge)

Note: Adspend excludes recruitment, includes direct mail and is at constant prices.

Source: AA/Warc Expenditure Report; ONS

At the quarterly level, the relationship is less clear as there are a number of short term factors that have a bearing on quarterly results. These include global sporting events such as the Olympic Games and World Cup and other influencers such as the timing of Easter. As a result, our adspend forecasts are based on annual GDP forecasts and for these we tend to use the consensus forecast published by the Treasury. This consensus is produced monthly and is based on around 40 independent forecasts from both city and non-city organisations.

Other more subjective factors are also taken into consideration. For example, after the severe recent recession, some advertisers might well be cautious when considering increases in marketing budgets and wait until the recovery is clearly under way. This would result in a lower rate of adspend growth than would be otherwise expected in the shorter term followed by a higher rate in the longer term.

The forecast annual adspend total is broken down into quarterly figures after considering short term factors such as those identified above. The quarterly totals are then split into the Display and Classified sectors by examining the long-term share trends for each. Each element is then split by media type, for example television within the overall display sector, again by analysing the trend in the medium's share of the sector. In all cases, a number of short-term factors will also be taken into consideration.

For recruitment advertising, which accounts for less than 3% of all adspend, we have a separate model which links changes in adspend to changes in the level of unemployment. A number of structural factors are also considered here such as the trend in favour of online ad expenditure in place of print.

How are the different sectors defined?

Where possible, the AA/Warc datasets show total UK advertising expenditure and are inclusive of both Display and Classified advertising. Full detail is given about the AA/Warc data on the Expenditure Report homepage.

Of course, end users will define 'advertising spend' in different ways. It's one of the reasons that the AA/Warc has developed an adspend table builder – it allows the end user to choose what datasets are included where and create their own totals. Warc can use certain definitions for reporting purposes, but often end users will want to adapt these. For example, should total main media advertising spend include direct mail? AA/Warc does take account of direct mail in its publically reported total – but other reports do not. And this makes almost a £2bn difference to the total value of the industry in 2013. Is a TV forecast based on spot advertising only or does it include other elements such as broadcaster VOD and product placement? It can affect the overall annual forecast percentage change by 1.0pp – or £400m annually.

To ensure our methodology and data coverage best suits the needs of the industry, the AA/Warc holds regular consultations with all the relevant trade bodies. By working with the representatives of individual media we can respond to market changes and adapt our datasets accordingly.

So that's how we do it. As you can see, it's a complex issue with many variables. But it's an important one to get right. With data from the AA suggesting that every £1 invested in advertising repays £6 in economic growth, measuring the ad market is measuring a crucial driver of national wealth.

In other words, the more analytical rigour brought to bear on the issue the better.

To find out more about subscribing to the AA/Warc Expenditure Report, please visit the website or contact Suzy Young for additional information.