Yesterday, we published a new long-term trend analysis: Global Ad Trends, a summary report which draws upon the data stored in our adspend database.

To provide some background, Warc has conducted an annual survey of global advertising expenditure since 1980, issuing questionnaires to monitoring organisations and/or ad industry bodies in each of the 88 markets we track. The survey covers TV, newspapers, magazines, internet, radio, cinema and out of home adspend. You can find a full list of our coverage here.

Once all markets are in, we harmonise the data (net of discounts, including press classified adspend and agency commission but excluding production costs) to give a more accurate, comparable picture of each country's ad market. This then allows us to identify meaningful trends in long-term advertising expenditure.

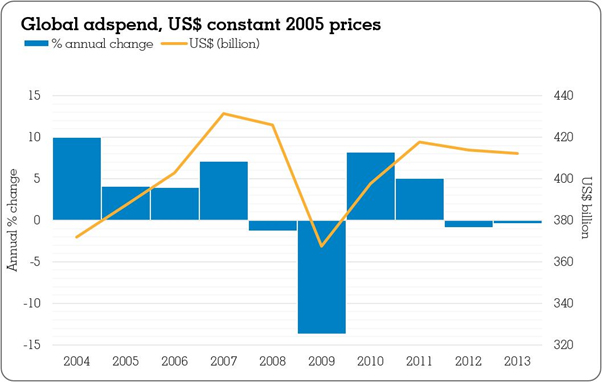

So what have we learned? Global adspend has increased from $362bn in 2004 to $512.9bn in 2013, a rise of 41.7% – or US$150.9bn – over the period. However, in real terms, factoring in inflation, the rise is less pronounced at 10.8%, or US$40.1bn. Furthermore, in the short-term, this represents the second consecutive contraction in adspend at constant 2005 prices.

(Click image to enlarge)

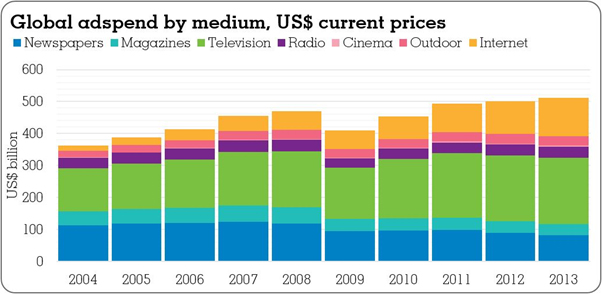

With regards to advertising expenditure via individual medium, there are some interesting sea changes at play. Despite some gloomy predictions for its future relevance, TV remains the biggest advertising medium globally with 40.8% share of total adspend, having recorded overall spend of $209.5bn in 2013. This represents significant growth of 55.7% for the channel since 2004.

Over the same period, internet advertising spend grew from $15.5bn in 2004 to $120.4bn in 2013: an increase of 675%. This equates to a ten-year rise in share of global adspend from 4.3% in 2004 to 23.5% in 2013.

This rapid expansion for internet has come at the expense of the print sector – inclusive of both newspapers and magazines – which has seen total advertising spend fall by $41.1bn over the last ten years to just $116.4bn.

Both newspapers and magazines have seen their shares of total global adspend roughly halve since 2004.

(Click image to enlarge)

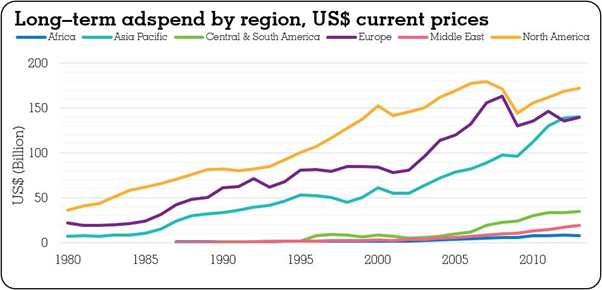

Looking at advertising budgets by region, North America remains the biggest spender, accounting for 33.6% or $172.2bn in 2013, but saw a drop of 11.1pp in total share since 2004.

Europe traditionally has been the second biggest region for ad budgets, but in 2012 – challenged by rapid growth in China – it was overtaken by Asia-Pacific. Europe accounts for 27.2% of global adspend ($139.4bn) with Asia-Pacific on 27.3% ($140.1bn).

The three remaining global regions – Central and South America, Africa and the Middle East – account for just 12% of global adspend between them, although this is a significantly higher proportion than the 4.1% recorded ten years' ago.

(Click image to enlarge)

You can find more information about Warc Data here.