Discounts are central to Black Friday and Cyber Monday, and a survey from brand tracking company Tracksuit suggests they may not harm brand equity, writes Stephen Whiteside from WARC.

Consumer excitement around Black Friday and Cyber Monday is usually based on a hunger for accessing deals and discounts on a wide range of products. Marketers, however, are often more ambivalent, and worried about the impact of cutting prices on long-term brand equity.

To help agencies, clients and retailers gain a deeper understanding of this issue, Tracksuit, the brand tracking company, surveyed 1,013 consumers in the US and 1,044 in the UK, with the latter country representing a useful point of comparison given the Black Friday/Cyber Monday period is a relative newcomer on the domestic marketing calendar.

Overall, Tracksuit found that roughly 70% of participants in both nations made a purchase from a Black Friday or Cyber Monday sale in 2022, demonstrating the sizable consumer reach of this occasion. (According to one recent forecast, Cyber Monday will deliver $12 billion in US e-commerce spending alone in 2023, with Black Friday pegged to generate $9.6 billion.)

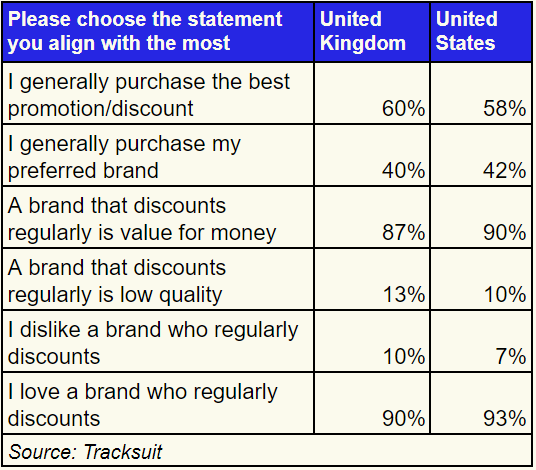

More broadly, Tracksuit discovered that 93% of American contributors to its survey “love” a brand which regularly cuts prices, and that 90% of their British counterparts held the same opinion. These figures stood at 90% and 87% respectively when it came to the view that “a brand that discounts regularly is value for money.”

Just 10% of US respondents, by contrast, thought brands running discounts with this level of frequency could be described as “low quality”, rising to 13% in the UK.

The role of discounts in the purchase mix

In providing a wider insight into the role of discounts in the shopping mix, Tracksuit’s analysis revealed that 73% of Americans “generally wait for a sale or discount” before making a purchase, as do 68% of the British sample.

Similarly, a 58% share of US participants “generally purchase the best promotion/discount” when shopping, whereas 42% of consumers typically opt for their preferred brand. Such totals came in at 60% and 40% in turn in the UK.

In combination, this suggests that loyalty – at least in self-reported terms – often takes second place to financial considerations (with current issues around inflation potentially being an additional stimulus for that habit).

Tracksuit’s data also highlighted the greater role of discounts for purchases that are perceived as “indulgent or expensive”, as over 80% of the interviewees from the two featured countries normally wait for a drop in prices before making these acquisitions.

Online leads, but shoppers travel across channels

Among the individuals who snapped up a bargain in the Black Friday and Cyber Monday sales last year, fully 91% of participants in the UK and US did so online, offline or both.

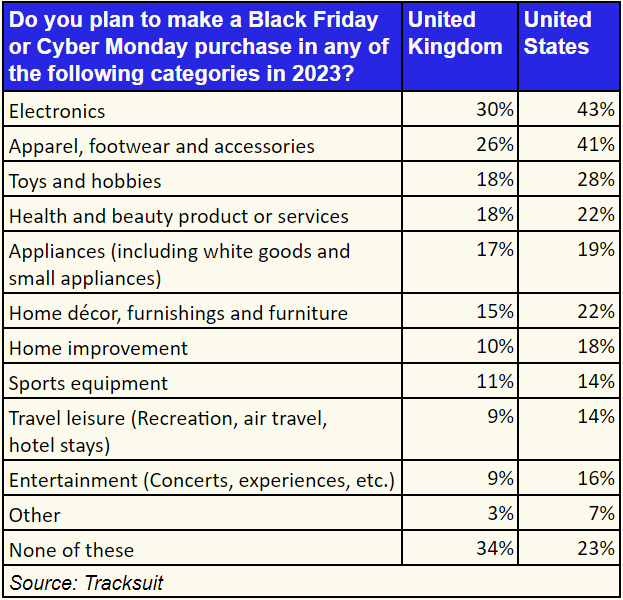

For 2023, electronics is the most popular category for anticipated purchases on both sides of the Atlantic, with over 40% of respondents in the UK and US referencing a desire to acquire these goods.

Tracksuit’s study drilled down into this vertical by seeking out information from all the survey participants regarding how they would approach buying a new TV set. As a starting point, waiting for a sale – like Black Friday or Cyber Monday – was mentioned by 54% of US shoppers and 42% of their British counterparts.

In an indicator of the cross-channel nature of such decisions, a 74% share of British consumers, and 66% of their American peers, would also check pricing online – figures hitting 68% and 58% in turn for visiting a physical store to view an item in-person.

Looking at online product reviews was mentioned by a majority of UK and US shoppers, too, while advice from in-store associates, and friends and family, had an influence for at least three in ten of contributors to the poll.

Equivalent trends were observable for finding the right pair of sneakers – a product of interest, in part, as apparel, footwear and accessories was the second-ranked category in the US (41%) and UK (26%) for consumers who expect to make a Black Friday/Cyber Monday purchase in 2023.

In detailing the likely process for buying a new pair of sneakers – or “trainers” in the UK – more than six in ten (65% in the UK, 62% in the US) of the entire panel would check pricing online during their purchase journey.

Visiting a physical store (64% in the US, 57% in the UK) was equally popular, and came in well ahead of reading online reviews (36% in the US, 31% in the UK). The lower scores here compared with buying a TV – as further evidenced in declines for seeking guidance in-store or from family and friends – probably reflect the fact that sneakers are not as big-ticket a purchase.

Elsewhere among planned Black Friday/Cyber Monday acquisitions in 2023, toys and hobbies, health and beauty and appliances made up the top five categories; next on Tracksuit’s list were home décor, home improvement, sports equipment, leisure travel and, finally, entertainment.

For each of these verticals, purchase intent was higher in the US than the UK, showing that this sales event is not – or, perhaps, not yet – as deeply entrenched in the shopping psyche in the latter market.

But, whatever the country, Tracksuit’s data suggests the nuanced use of discounts – and an expansive understanding of shopper habits across channels – can help marketers engage a large number of consumers without necessarily hurting brand perceptions.