Soaring investment with Big Tech has obscured a decline in spend with media environments in which ads run alongside professionally produced content.

It’s customary to begin the calendar year in optimistic tones. As such, my apologies for the next 600-ish words – especially if your job happens to involve selling advertising at a broadcaster or publisher.

Just before Christmas, WARC released some remarkable charts that you may have missed in the festive melee of mince pies and mulled wine. These charts – enabled by WARC Media’s whizzy new interactive dashboards showing ad spend, media consumption and media costs data – painted a grim picture for media owners hosting professionally-produced content.

In short, the media market as one may have defined it 20 years ago has (at best) plateaued or even entered into decline. And this has major implications for marketers and agencies.

Trillion-dollar fantasy

We’re all familiar with the statistical sugar-rush provided by advertising investment forecasts. The most recent numbers from WARC Media’s data team suggest that, in 2024, global advertising spend will surpass $1tn for the first time, up 8.2% year-on-year.

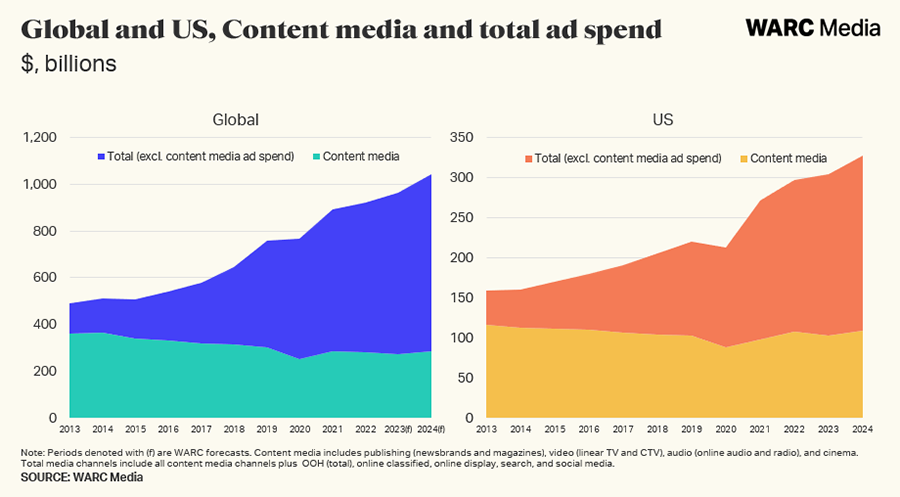

It is also widely acknowledged that a growing share of this total spend is going to digital platforms – most notably Alphabet, Meta and Amazon. Content media owners (including all forms of TV, publishing, audio and cinema) are forecast to receive only 27.2% of all global ad investment in 2024, down from 71.0% a decade earlier.

What may be less understood is the extent to which soaring levels of investment with YouTube, Instagram and TikTok, as well as the hype around TV streaming and podcasts, has obscured a decline in total spend with media environments in which ads run alongside professionally produced content.

The size of global ad investment with these kinds of media companies reached $363.2bn in 2013 but shrank to $254.1bn during 2020. A post-pandemic recovery will see spend climb back to $284.1bn in 2024, buoyed by election cycles and quadrennial sporting events, but the lack of upward trajectory is clear to see.

In fact, it’s slightly misleading to talk about channels in broad terms, when the prime beneficiaries of ad spend growth over the last 10 years amount to only a handful of platforms.

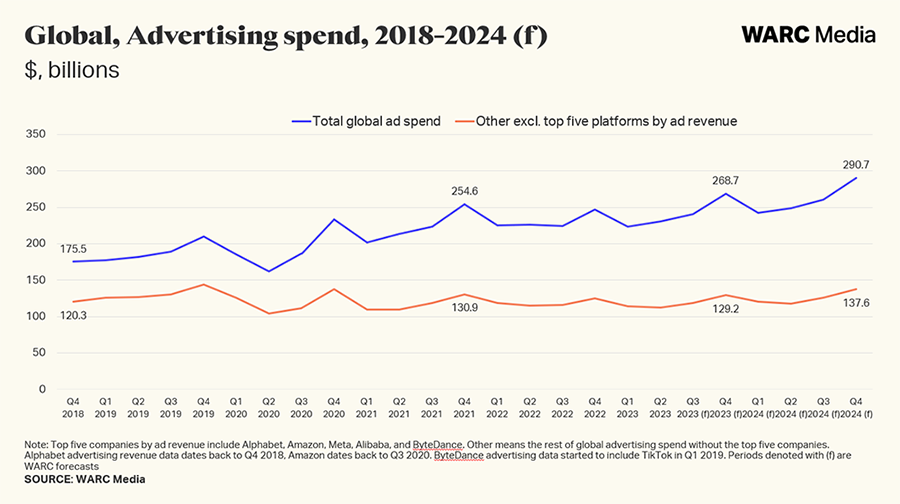

Analysis by WARC Media found that, after deducting investment with the five largest digital media owners globally (Alibaba, Alphabet, Amazon, ByteDance and Meta), the remainder of the ad market has been flat since 2018.

It’s a remarkable observation: outside of the ‘big five’, every media owner – from NBCUniversal and The New York Times, to Snap and JCDecaux, to Disney and Spotify – is competing for share of a largely fixed market. And that’s before we consider the impact of new entrants, like Netflix’s much-vaunted arrival into the ad sector.

Out of reach

What it means to be a seller of advertising has been revolutionised in recent years; the quality of content and environment is of decreasing importance versus the availability of audience data and proximity to purchase (hence the success of channels like retail media).

There is little point in publishers and broadcasters salivating over the prospect of a $1tn global ad market when most of that spend is locked away behind walled gardens. For now, at least, they are fishing in a finite pool – and success is winning a share of those budgets from those with similar propositions.

Industry analyst Brian Wieser has repeatedly noted that spending on TV-related ad inventory generally comes from a fixed budget for professionally-produced video. Despite the rise of streaming and connected TV consumption, non-TV-related budgets still remain out of reach.

Similar trends can be observed in newspapers and magazines, where investment by brands has collapsed in recent years. Modest increases in digital ad revenue have not been sufficient to compensate for the collapse of overall publishing ad revenue.

This all matters to advertisers, which require a healthy media market to reach their customers and build their brands, and desire premium media environments. Equally, marketers focusing budgets on three or four platforms may have less need for a media agency to handle that spend.

Of course, there will be media winners in 2024 but for the majority, the year will pose headaches and challenges to overcome.

Happy New Year…