This article is part of the March 2021 Spotlight US series, “Media strategies for a shifting US landscape.” Read more

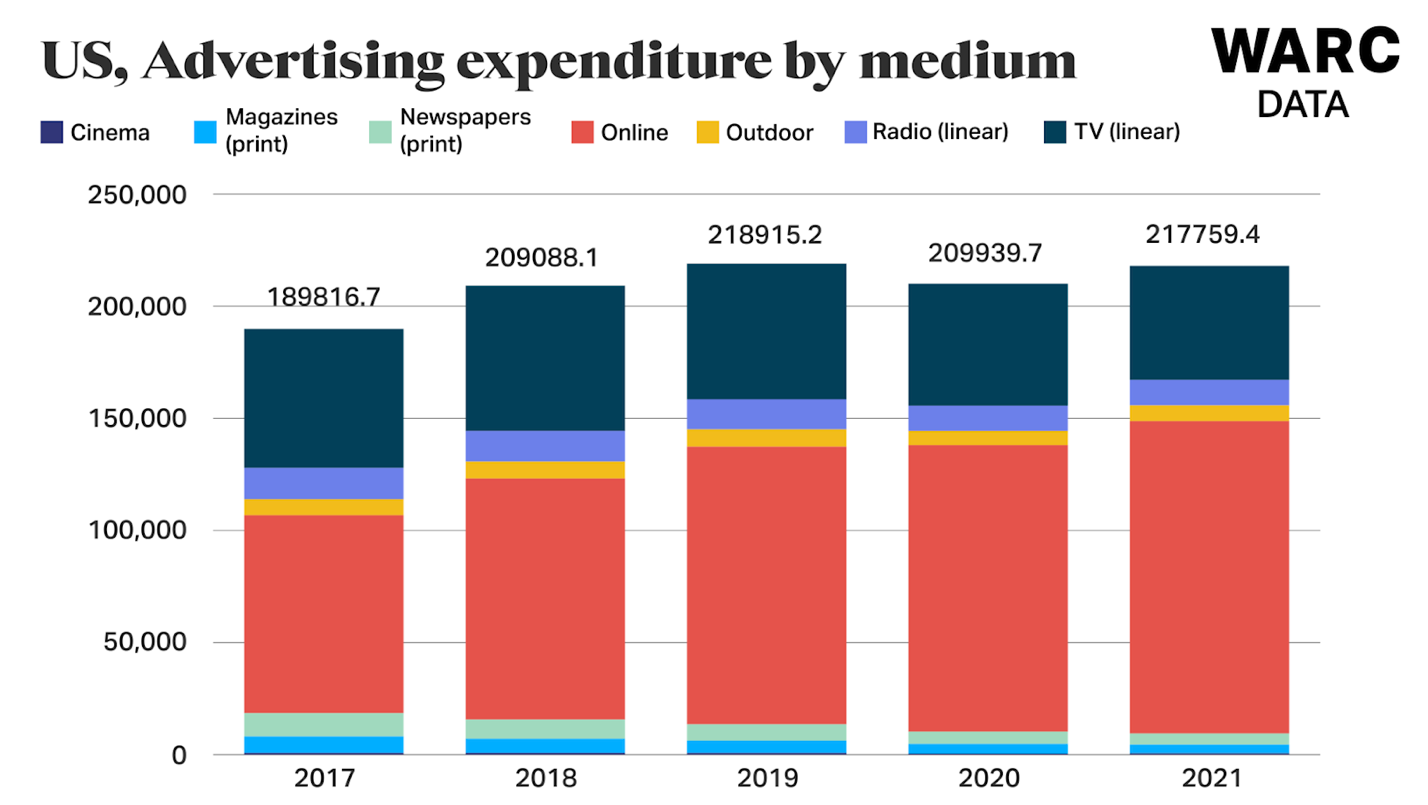

Getting one’s head around the behemoth that is the US media marketplace is a tough task. Even in a build-back year, ad spending in the US is expected to reach $218 billion, just under the amount that was spent in pre-pandemic 2019, according to WARC Data. To put that figure in perspective, the US alone is far bigger not just than any other country, but any other region in the world.

In this second installment of our Spotlight US series, “Media strategies for a shifting US landscape,” we look at a market with so many moving parts that some of the big trends have little to do with COVID-19. The industry is also wrestling with systemic racism and further privacy regulation, among other issues.

Our team of expert authors examines the following themes:

1. How the upfront is changing and should change, albeit slowly

Ben Jankowski, SVP/Media at Mastercard and co-chair of the ANA’s Media Leadership Committee, is one of the leaders in the US media industry who has been calling for the $20 billion US TV ad sales upfront market, held each spring, to change, calling for alterations to timing, financial flexibility and data. While admitting to slow progress, he in this video interview, he explains how awareness is rising about how to move forward. Mike Piner of Mediahub states the case for how the upfront could work better by reflecting different types of marketer KPIs rather than raw audience guarantees.

2. Why it’s primetime for challenger brands

The fact that many channels have been a buyer’s market for the last year has allowed challenger – and often digitally-focused – brands to come into media marketplaces they otherwise might not have heavily invested in, or even entertained. As Simulmedia CEO Dave Morgan points out in his story on data-driven linear TV, brands have been entering all forms of TV advertising, often at a lower price point. The online car seller Carvana spent $73 million in the medium in the first half of 2020, and the online food delivery category upped its TV impressions by 34%.

This has played out in sports sponsorship too, as A1 CEO Jim Andrew notes in his article on how sponsorship will change going forward. Brands reflecting the pandemic lifestyle, such as Pit Boss Grills and Sony PlayStation, have entered the market.

3. Ways to prepare for the post-cookie world

According to Kantar, only 40 percent of marketers are preparing for when Google phases out third-party cookies and Apple makes its IDFA (identity for advertisers) opt-in, despite concerns from two-thirds of them about how they will target going forward. One way brands can start to prepare, according to John Nardone, CEO of Flashtalking, is to identify what tier of first-party data they have, which will help inform how they plan, but even those with the best and most actionable first-party data – like Amazon and Walmart – will probably need to work with multiple identity partners to navigate the coming cookie-less terrain. Jane Ostler at Kantar outlines the company’s direct integration deals with publishers, who stand to become key linchpins in the digital ecosystem going forward.

4. Why breakthroughs in data and analytics are transforming TV advertising

Is it possible that digital’s targeting loss will be TV’s gain? That’s one conclusion that could be drawn from advances in data-driven TV advertising, where a variety of factors are coming together to open up the market to new possibilities. First, from a privacy standpoint, as Jane Clarke of the Coalition for Innovation in Media Measurement emphasizes that the content and advertising data coming from set-top boxes and Smart TVs is privacy compliant, making it a safe space for marketers. CIMM has developed recommendations on how to commingle these two powerful data sets to give media owners and brands further granularity into consumers. Simulmedia’s Morgan points out how this data is being used in linear TV, allowing brands to start small, learn and optimize, at budgets that are higher than digital, but nowhere near what they would have to spend in traditional TV. But Jim Spaeth and Alice Sylvester of Sequent Partners caution that the industry needs to work together on data and analytics breakthroughs to truly transform the medium.

5. Providing scale for under-represented publishers

In a country wrestling with the effects of systemic racism, and a digital media world dominated by the enormous scale of Google, Facebook and Amazon, there’s been a concerted effort over the year by publishers and media agencies to create ad marketplaces that allow brands to invest in under-represented publishers, many of them from the Black, Hispanic and LBGTQI+ communities, bringing scale to content that has been overlooked by marketers. Samantha Skey, CEO of SHEMedia, explains the creation of the company’s Meaningful Marketplaces, and why they deliver not just for publishers and brands. According to Mastercard’s Jankowski, there’s also been a brand-side awakening about how brand safety guidelines – such as inclusion/exclusion lists – have unintentionally and specifically hurt the prospects of minority content creators, which the industry is now seeking to remedy.

This Spotlight US also takes a look at how consumers have reacted to local TV advertising during the pandemic, from Bill Day, svp/strategy at Magid, and, from Ben Speight of Lockard & Wechsler, how brands should rethink their approach to TV planning, especially now that the majority of new subscribers to streaming services are over the age of 40.

It’s another sign that media has fundamentally changed, for consumers, media owners, brand owners, and agencies. We hope you enjoy this edition.

Read more in this Spotlight series

Mastercard's Ben Jankowski on the upfront, cross-platform, sponsorship and media buying's slow, but steady, evolution

Cathy Taylor

The three tiers of first-party data strength and what they mean for brand’s identity strategies

John Nardone

The data and analytics breakthroughs that can complete the transformation of TV advertising

Jim Spaeth and Alice Sylvester

Buying ads with under-represented publishers – at scale – lets marketers vote their values

Samantha Skey

Recommendations for co-mingling set-top box data and Smart TV ACR Data

Jane Clarke, Howard Shimmel, and Gerard Broussard