Brands focusing ad investment on premium video inventory are being punished by legacy ad tech models, argues Cadi Jones, Commercial Director EMEA at Beeswax.

Earlier this month, we celebrated World Television Day. As the availability video inventory increases, including more connected TV, there are some big questions that anyone involved in this space need to ask themselves.

In recent years, online video has grown to account for one-third of all internet display spend. Video has grown because it’s just so effective. Money follows results. A recent Videa study showed that marketers now consider digital video to outperform against TV. In a separate study by LeadCrunch, video was used significantly more for both lead generation and lead nurturing than display ads.

As WARC flagged in its 2020 Marketer’s Toolkit pack, connected TV (CTV) is a key area of focus for many brands. CTV is growing even more rapidly than video: eMarketer predicts that CTV ad spend in the US will reach $6.94bn this year, and total $10.81bn by 2021. While YouTube picks up around 40% of that spend, 30% currently goes to two independents, Roku and Hulu. More than 50% of CTV inventory is currently bought programmatically.

In the UK, more than three-quarters of digital video is now bought programmatically, but the original platforms and tools were not designed with video in mind. Instead, video was kept siloed in specialist platforms. While video functionality has now been built into most demand-side platforms (DSPs), in some it can still be difficult to achieve strong performance, and usability issues persist. To me, however, the biggest problem is not with technology, but with the commercial model that powers all traditional programmatic entities: taking revenue share.

How we got here

Currently, if you’re a publisher with video supply and you want to monetise that inventory programmatically, you appoint a supply-side platform (SSP) to surface your inventory and convert your ad slots into bid requests. Similarly, if you’re an advertiser who wants to respond to those bid requests, you’ll need a DSP to translate those bid requests into responses, including the price that you’re willing to bid. This applies to CTV as much as to other forms of video.

Historically, both DSPs and SSPs have operated on revenue share commercial models, taking a percentage from the transaction as it is processed. That worked when programmatic advertising mostly trading low-cost remnant supply. Now the market is more mature, with programmatic video representing 43.4% of transactions and averaging a CPM of $30, the revenue share model seems punitive. It costs platforms on both the supply- and demand-sides the same to transact on video formats, but because the CPM pricing is so much higher on video formats, the revenue share amount works out as a much higher number.

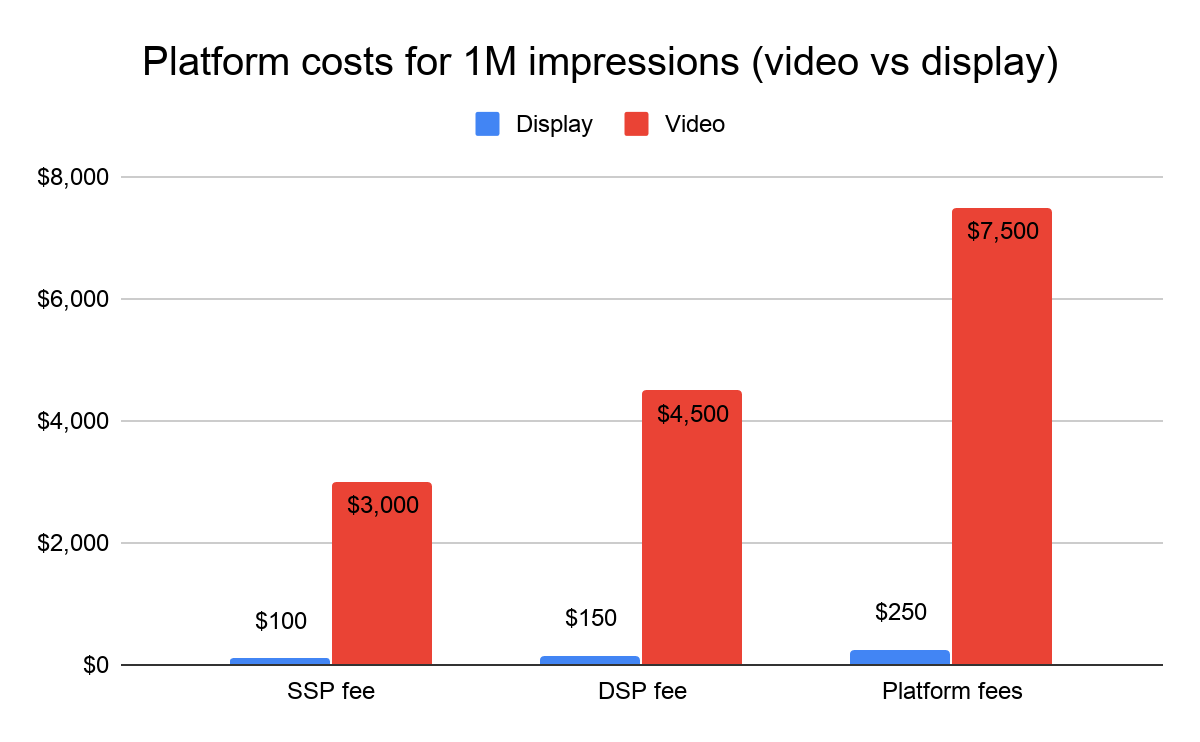

By way of example, using WARC’s own research, when buying an impression at $1, the publisher will receive $0.28. If we assume a 15% take-rate from the DSP, that’s $0.15, and the SSP’s 10% equates to $0.10. When translating those numbers against a premium publisher’s video content or CTV inventory at a CPM of $30, those take rates equate to $4.5 and $3.

However, unless the DSP is actually serving the ad creative (resulting in a minor increase in cost), the operating costs of delivering a video campaign are the same as when delivering a standard display campaign.

As the chart below shows, the costs can be very different indeed to both buyer and seller. This effectively means the margin is much greater for the ad tech platforms involved if they are working on a percentage of media (revenue share) model.

Everyone understands that the programmatic platforms (Beeswax included) are running businesses, not charities. However, the revenue share model clearly penalises the publishers of premium content (especially video, which sells at a higher CPM price point) to a much greater extent, as well as the buyers who want to access this premium inventory.

Alternative models

Increasingly, we’re seeing both the buy-side and sell-side questioning the value that they are getting from partners taking a share of the revenue. As The Ozone Project’s Commercial and Operations Director Danny Spears said, “The question that should always be asked is ‘What do I get for paying more?’.”

While brands will pay a higher CPM for advertising against premium content to deliver greater ad effectiveness and ROI, the percentage-based fee models of certain ad tech vendors simply means they can take a higher cut from premium publishers – versus long-tail publishers – for nothing extra in return. Working with fixed-fee/SaaS partners creates a fairer, more sustainable relationship that ultimately allows premium publishers to reinvest further in great content.

Brands are increasingly in-housing their creative strategies, with companies such as Lego, Danone and Diageo seeing significant benefits by being able to get quicker sign-off, a greater range of creative, and closer access to audience data for iteration on creative assets. However, where this has previously been difficult is in video, as these are more complex to manage. A new breed of creative company has emerged to help brands with this, allowing for dynamic video content production based on the brand’s first party data.

Even within the complex creative area, pricing needs to relate to the work required – with Sublime’s team working to incentivise best practice and superior user experience. Andrew Buckman, Sublime’s new CEO, has seen significant change in this space over the last two-and-a-half years: “Brands from all sectors, from travel and entertainment to finance and telco, are now looking for innovation across their video formats to capture attention and increase campaign results. But in today’s climate, this needs to be priced in a way to incentivise usage, and not disincentivise it.”

As CTV continues to evolve and develop, there will be many more acquisitions such as Roku’s recent purchase of DataXu, as there are currently only two options for buyers and sellers of CTV inventory: either you decide to become a tech player, buying a company and maintaining the software necessary to run these transactions, or you work with a partner on a fixed monthly fee model.

If you’re responsible for delivering video – whether on the buy side, sell side or creative side – you heard it here first. If you’re paying a percentage of media spend, “rev share” or any other percentage model linked to the cost of the video play, you are paying too much.