Shoppable media

This article is part of a series of articles from the WARC Guide to shoppable media.

Unlike search, retail is likely to remain a fragmented marketplace. Brands must therefore ensure they understand the nuances and intricacies of each leading platform.

In 2020, Amazon cemented its place as the third-largest digital media platform, behind only Google and Facebook. Brands have found much success with Amazon Advertising, as what it lacks on time on site, it more than makes up for with efficacy and transparency.

Other retailers have noticed, and we expect to see more and more retailers roll out Sponsored Ads auctions. As they do, brands have a unique first-move advantage while auction density is low in these emerging platforms.

Understanding platform nuances

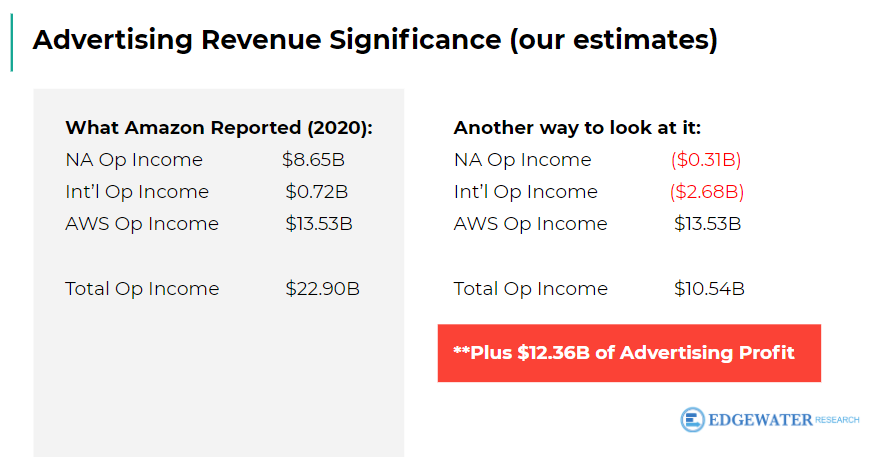

As we think about why retailers are so interested in adding ad platforms, this chart from Edgewater Research makes a compelling case.

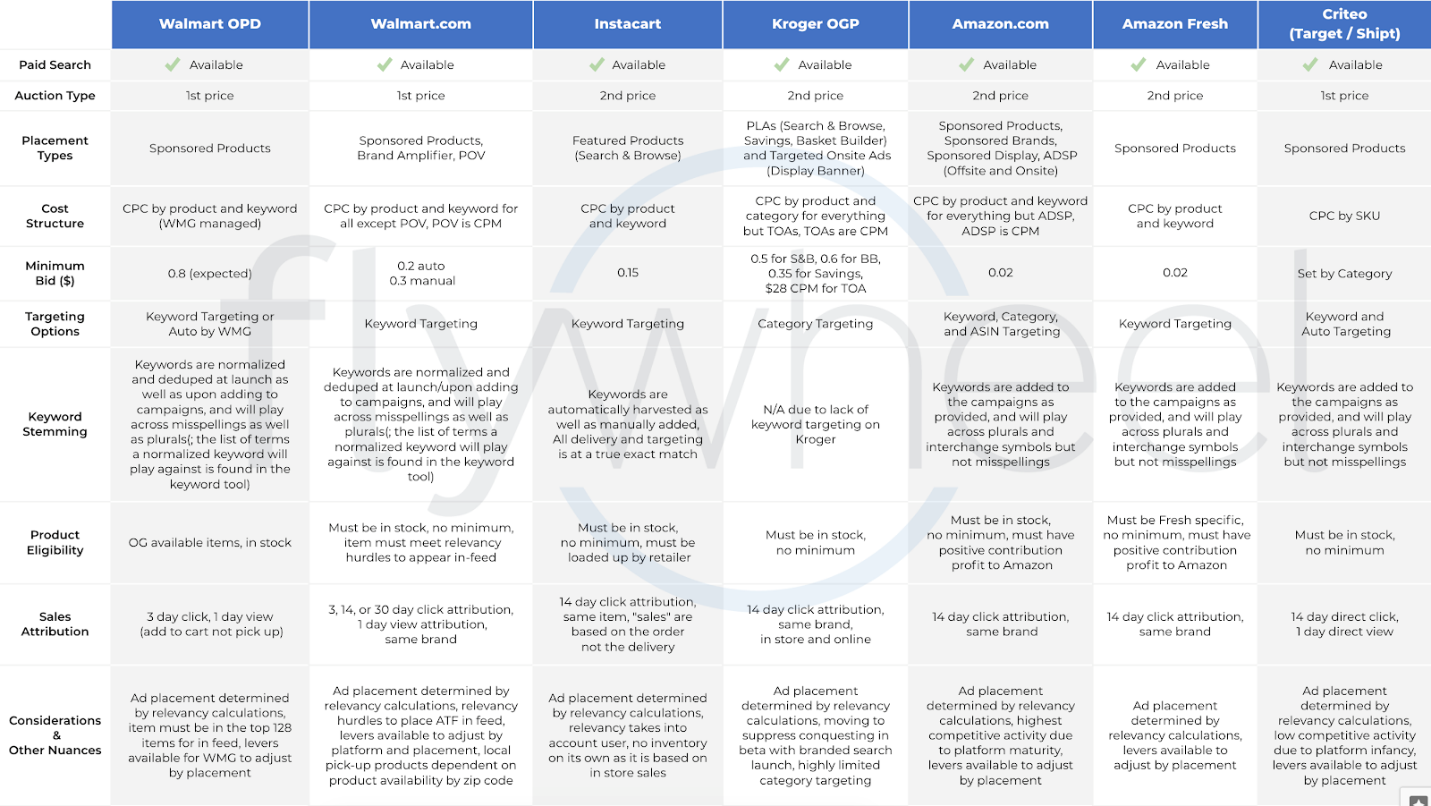

However, each of the retailer biddable platforms have nuance around auction type, eligibility, stemming, and attribution. Brands should familiarise themselves with the nuance, especially when comparing performance across platforms. Below is a quick comparison across many of the more popular platforms in the US.

An additional consideration is figuring out how incremental each unit is relative to the SKU, and how the advertising may shift the mix to either a more or less profitable SKU, both for the advertiser and the retailer. Think of this as a planograming exercise, except instead of the set resetting every six months, it resets every 15 minutes – and instead of obsessing over a six-foot set, the brand needs to obsess over customer search queries.

Instacart recently released data on the importance of place, explaining that click-through-rate (CTR) is 20% higher for the top three placements of paid search compared to the next top three slots of organic search results, and 550% higher than the next three paid search placements. Brands need to think through time and place for all investments.

Walmart’s unique reach opportunity

Earlier this year, Walmart announced it was teaming up with the Trade Desk to create a new DSP that leverages Walmart’s unique first party data. At the same time, Walmart rebranded its media arm to Walmart Connect, a clear nod to its unique, scaled ability to connect online and offline.

“We've built a substantial business that can serve clients in a way no one else can – as a closed loop omnichannel media company,” said chief customer officer Janey Whiteside in a press statement. The combination of the Trade Desk’s leading DSP with Walmart’s unique first-party data and vertical integration to screens in store should provide brands unique reach opportunities.

With the cookie on its way out and IDFA promising a decline in third party data, retailers have a chance to exponentially grow their media offering as they have the strongest buying singles. However, they also have a tension to the transactional nature of e-commerce sites, where decreasing time on site is typically the goal.

Low dwell time will typically decrease RPM, especially if sold on a CPM basis. As such, look for retailers to figure out new ways to reach customers where customers are spending time – Amazon via Fire TV and Walmart via the 170,000 screens it has installed across its 4,500 stores.

Investment in upper-funnel tactics

As brands invest in upper-funnel tactics, the need for advanced metrics becomes more and more important.

Amazon Marketing Cloud recently became an open beta and the insights it unlocks is substantial: what percentage of Sponsored Ads sales were preceded by a DSP view, what time of day is the DSP more effective, and – of course – solving for reach and frequency.

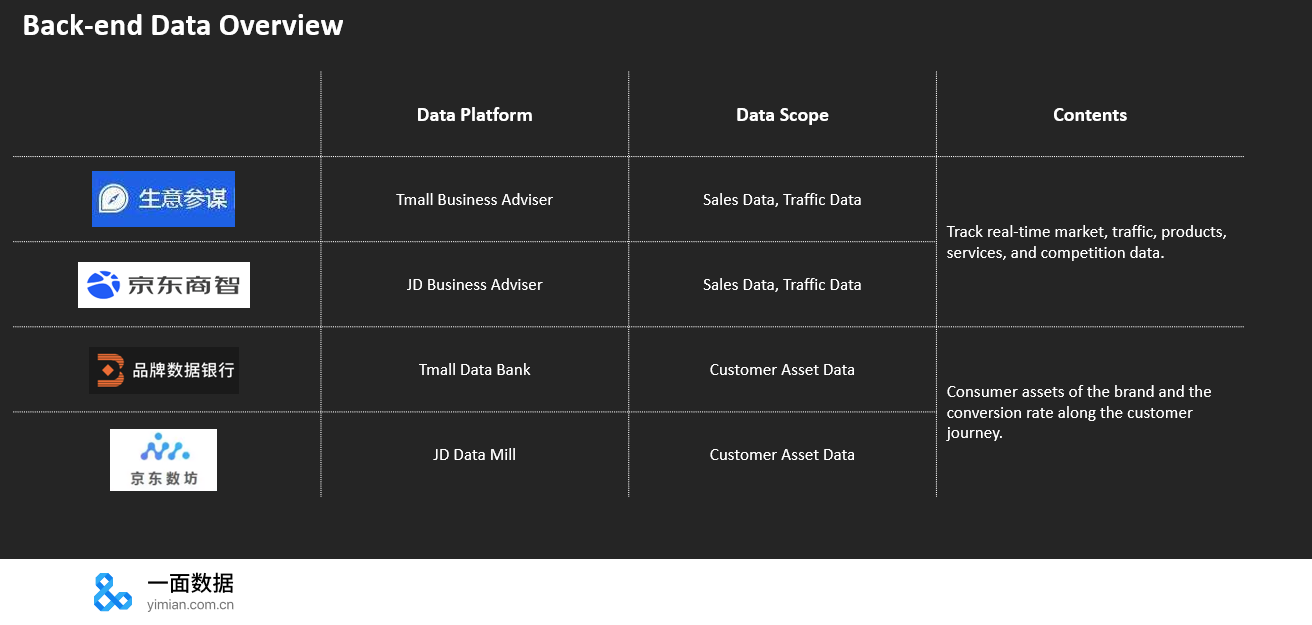

In many ways, Amazon is catching up with Chinese retailers in providing a granular (though privacy-focused, via minimum cohort sizes) analysis of customer behaviour. From my colleagues at Yimian, here’s a quick overview of data platforms across some of the leading Chinese sites.

For 2021, we expect to see retailers looking to both expand existing Sponsored Ads and DSP offerings, as well as thinking through incremental offerings.

For Amazon, the Sponsored Display and Sponsored Brands Video placements are unlocking both unique inventory, as well as the ability to get further out of the aisle – thereby driving more incremental sales.

For Walmart, Online Pickup and Delivery inventory is now self-serve, enabling brands to reach customers at this critical point of purchase. Instacart and Kroger are opening up richer data. And PromoteIQ and Criteo are giving brands both increased reach and targeted retailer precision.

For brands and agencies alike, I’d encourage folks to spend as much time as possible understanding the nuance and intricacies of these various platforms. This isn’t a space like search where one platform will dominate. Retail has always been, and I expect it to continue to be, fragmented.

Read more articles from the WARC Guide to shoppable media.

The WARC Guide to shoppable media

Deep-dive deck

Shoppable media as an omnichannel strategy

Patrick Deloy and Nathan Petralia

Influencer marketing’s impact on shoppable media

Kaho Yamada

What you need to know about interactive audio ads

Flora Williams

Fake it until you make it: Managing the transition before full social media shoppability

Yulia Livne

Shoppable ad formats: The pros and cons

Nate Shurilla