The Feed

Read daily effectiveness insights and the latest marketing news, curated by WARC’s editors.

You didn’t return any results. Please clear your filters.

The Future of Measurement: four key trends

The Future of Measurement: four key trends

The evolution of measurement holds enormous and powerful potential for marketers, if the industry can overcome the state of decision paralysis – in an extensive new report, WARC identifies four areas to focus on with practical steps to help.

WARC’s Future of Measurement report is based on exclusive proprietary data as well as external research and reporting.

WARC members can read the full report here.

If you’re yet to subscribe, you can read a sample of the report here.

Why the future of measurement matters

Third-party cookies will finally be eliminated from online advertising this year, but only a tiny fraction of marketers are conducting holistic measurement, with a majority not using any modelling, explains Paul Stringer, WARC’s managing editor of research and insights, in an introduction to the report.

Four big ideas

The report explores four key trends across different chapters:

- AI and the growth of synthetic data

AI is set to transform market research, but the quality of output is only as good as the reliability of the data put in. Marketers will have to grow accustomed to deploying hybrid approaches. - The third-party cookie countdown

Though 75% of marketers understand their dependency on cookies, many remain unprepared for their end; interoperability of replacement systems is a big concern. - Hurdles in holistic measurement

MMM is a hugely exciting new step in measurement, but it requires some know-how to put into practice. - Closing the sustainability gap

Sustainability requires a more nuanced definition of growth, while new regulations will put pressure on brands to measure the emissions resulting from their activities.

Key quote

“With measurement continuing to evolve in several directions at once, marketers find themselves battling multiple headwinds: not only the demise of third-party cookies, but new regulations in sustainability reporting, and, of course, the growing influence and impact of AI” – Paul Stringer, Managing Editor, Research & Insights, WARC.

What shall we watch tonight?

What shall we watch tonight?

The options for TV viewing have never been greater, but finding TV content, whether traditional or streaming, can be a frustrating and time-consuming endeavour for viewers.

How viewers find content

A report* from Comcast Advertising and FreeWheel highlights the issues:

- Only 25% of viewers surveyed say that all their content can be accessed in one place.

- Two-thirds of European viewers spend more than six minutes searching for something to watch; 46% say the difficulty in finding new content can get frustrating.

- Social circles play a big role in how viewers learn about new content: 51% of European (vs. 55% of American) viewers said they receive recommendations from friends, family, and colleagues.

- Viewers’ choices are impacted by situational factors, but genre is foundational: 75% of European viewers said that genre is a key factor in choosing what to watch.

- Channel surfing is still alive: 55% of European viewers start their content search by channel surfing or scrolling through a programme guide or app.

- Individual platforms play an important role in how viewers choose content: 53% of European viewers have found and watched content recommended on their home screen, highlighting how essential it is for content owners and advertisers to tap into this feature.

- Promos and native ads boost content consideration: 85% of US and European viewers are likely to be influenced to watch provider-recommended content if they had seen an ad or trailer previously.

Why it matters

With a huge volume of content available across multiple platforms and devices, consumers are overwhelmed with choice. Anything that enhances the discovery and navigation experience is likely to lead to more opportunity to engage viewers with relevant ads and build brand sentiment.

*Content Discovery in a Multiscreen TV World: Surfing and Scrolling in a Sea of Content analyses trends in how consumers navigate and discover content across traditional TV and streaming in the US and five European countries (UK, France, Germany, Spain, and Italy).

Sourced from FreeWheel

Amazon bullish on Prime Video ads

Amazon bullish on Prime Video ads

Q1 ad sales at Amazon were up 24% year-over-year to $11.824m, representing just over 8% of total net sales.

Why it matters

Other parts of Amazon’s business may be bigger, but advertising remains an important contributor to profitability in North America and internationally, CFO Brian Olsavsky told an earnings call.

Takeaways

- Ad growth was primarily driven by sponsored products, “supported by continued improvements in relevancy and measurement capabilities for advertisers”, said CEO Andrew Jassy.

- Amazon sees continued “significant opportunity” in sponsored products as well as in “areas where we’re just getting started like Prime Video ads”.

- Jassy believes that Prime Video ads offer brands value “as we can better link the impact of streaming TV advertising to business outcomes like product sales or subscription sign-ups, whether the brands sell on Amazon or not”.

Key quote

“I think advertisers are excited about being able to expand their ability to advertise with us in video beyond Twitch and Freevee to Prime Video shows [and] movies” – Andrew Jassy, CEO at Amazon.

Sourced from Seeking Alpha, Amazon

Why delayed gratification is key for Adidas

Why delayed gratification is key for Adidas

Adidas says it will be “disciplined” in its release of highly sought after trainer lines in order to keep demand (and therefore prices) high, as the sportswear company delivers better-than-expected results.

What’s going on

The company had around 8% revenue growth in the first quarter, and a significant return to big profits following a difficult post-Yeezy period.

The reason, says CEO Bjørn Gulden in a statement, is that the lifestyle segment, comprising some of its most desired and most venerable models, is driving that growth.

“The demand for our footwear franchises Samba, Gazelle, Spezial, and Campus is still very strong and growing.”

Leadership has maintained a firm line on buying in order to make sure both the brand and retailers are not over-inventoried. “We think that this year is about building a solid growth, building a quality growth, making sure that we and our retail partners don't need to discount.”

Maintaining control over pricing remains imperative.

The profit motive

Vitally, profitability grew 6.4% percentage points to a gross margin of 51.2%, the result of reduced discounting, healthier inventory, and a more favourable mix. In addition, in terms of raw numbers, the company is now lapping the drop in revenues that was the result from abandoning the Yeezy brand, following Ye’s controversial remarks.

But it’s worth digging into how the company is thinking about marketing as a key driver, having increased marketing by 9% in the quarter, all of which will push the percentage of marketing to sales to 12%.

“We still expect significant FX headwind. And as we said many times, we will continue to kind of overinvest in marketing and sales to build the momentum then to get the leverage as we grow,” Gulden recently told investors. “I'm very happy with the way things have developed in the last three months. It shows the strength of the brand and the strength of this company.”

In context

It’s a big year for sport with a Euros football competition and the Paris Olympics, and both events are expected to drive sales of performance lines. However, Adidas’s results follow the initially shocking news that the sports brand would no longer sponsor the German national team, as Nike agreed a much higher contract than the €50m that the deal had previously cost the brand.

Sourced from Adidas, Seeking Alpha

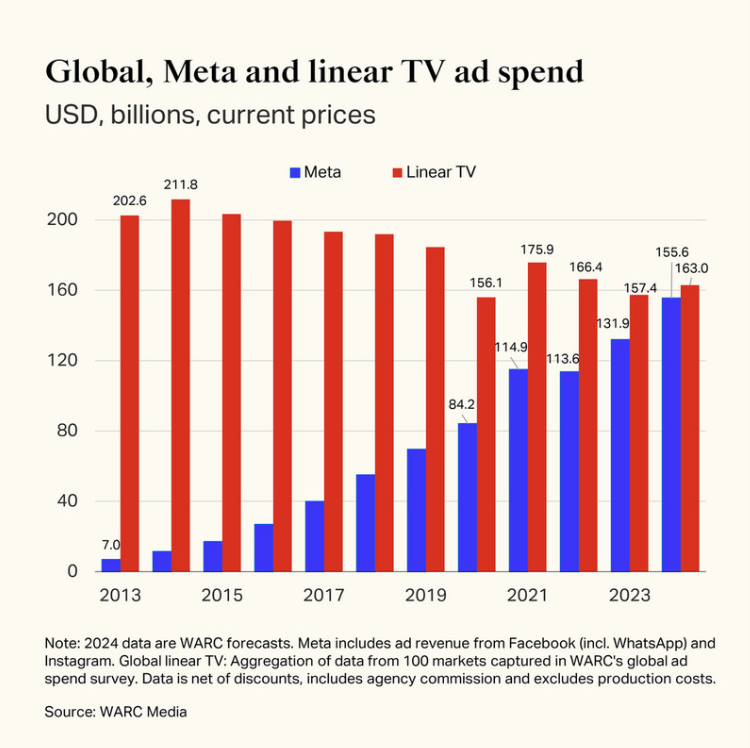

GAT: Meta on track to surpass all linear TV spend

GAT: Meta on track to surpass all linear TV spend

In just a few years, ad revenues going to Meta – owner of Facebook, Instagram, and Whatsapp – could outgrow the entire global linear TV industry, based on current trajectories; the findings of a new Global Ad Trends report indicate changes to global advertising as social media stands to become the world’s largest ad channel.

WARC Media members can find the full report here

If you’re not yet subscribed to WARC Media, you can access a sample of the report here.

Why social’s supremacy matters

Global social spend is set to total $247.3bn in 2024, up 14.3% year on year, ahead of paid search. This could see it grow to become the biggest advertising channel by spend.

But that’s a tussle among the new giants. Perhaps the more consequential shift is that on current trajectory, just the adspend going to Meta alone is set to earn more than the entire global linear TV industry.

It’s a moment that would signal a changing of the guard, not only from old media to new, but from a significant plurality of companies making money from global ad growth to a consolidated market dominated by global tech players.

What’s behind this

Both Facebook and Instagram grew by more than 20% year on year in Q1 2024, and Meta is forecast to earn $155.6bn in ad revenue this year.

- Tools like Meta’s Advantage+, which automates aspects of creative and media planning, are increasingly popular with advertisers.

- Meta reportedly increased its ad load in Q4 2023 to 19.1%, with most Reels sessions now having seven or more ads.

Elsewhere in the market

- The +18.3% year-on-year increase forecast for TikTok in 2024 marks a significant slow-down from the 87.8% growth rate it clocked up last year, despite the introduction of new search and shopping ad formats.

- Pinterest is set to enjoy a 17.3% year-on-year increase in ad revenue in 2024, while Snapchat is forecast to grow 13.7%.

- X’s ad revenue in 2024 is predicted to decline by 6.4% globally and 5.1% in the US – but this appears to be stabilising.

Editor’s view

“Much of social media’s success has been driven by Meta’s remarkable renaissance. However, social’s stronghold on budgets can also be seen in TikTok’s rise, and a return to double-digit ad revenue growth at Snapchat and Pinterest.

“However, with this dominance comes challenges, such as rising advertising loads in social environments, and the impact of AI on media planning. In this report, we take a holistic view of the global social media landscape, which shows no sign of losing momentum” – Alex Brownsell, Head of Content, WARC Media.

Pizza Hut changes direction in China

Pizza Hut changes direction in China

Pizza Hut, owned by Yum Holdings in China, is transforming from a premium casual dining brand to become a mass market operation, a direction that is reflected in its pricing policy.

What’s happening

- Joey Wat, CEO of Yum Holdings, told an earnings call that the brand was “ready for accelerated growth”, having added 400 new stores in the past year and increased city coverage by 10% to over 750 cities.

- “We aim to broaden its addressable market with a strong value proposition for mass market appeal,” he said. “Our strategy emphasises widening price points, expanding into new categories and delivering emotional value to consumers.”

- More products are now being offered at an “entry price” of less than RMB50; sales of such pizzas grew double digit in Q1.

- Similarly, more products are being targeted at the growing number of one-person meal occasions.

- “We are driving the ticket average lower at Pizza Hut,” Wat declared. “But our focus remains the same: driving incremental sales and focusing [on] profit and margins.”

Why it matters

China’s economy may have grown faster than expected in Q1, but consumer confidence is low. “Consumers are more rational in their spending in the new normal,” Wat acknowledged, “but they do respond well to our exciting offerings and campaigns.” That points to brands needing to be agile and able to respond to new trends as well as being timely and targeted in their marketing.

Key quote

“Urbanisation and long-term consumption upgrades in Tier 2 cities and below present a particularly attractive opportunity for us. Housing and living costs are more affordable there. Tremendous consumption potential has yet to be unleashed” – Joey Wat, CEO at Yum Holdings.

Sourced from Seeking Alpha, Yahoo! News

[Image: Pizza Hut]

Chinese youth embrace the single life

Chinese youth embrace the single life

A growing number of young Chinese are opting to live alone and stay unmarried, a lifestyle choice that’s affecting how they spend their money and driving a preference for niche brands over mega brands.

Why Chinese singles matter

China’s solo lifestyle movement is evolving alongside the country’s wider economic development. It’s influencing how young people shop, what they choose to do in their spare time, and the types of brands they prefer. While the Chinese government is implementing new policies to tackle its low birth rate, it might not be enough to counter the current trend and its economic implications.

What’s happening

“We’re seeing more young people embrace lifestyles that balance individual leisure time with work and what might be considered traditional family obligations,” Jacob Cooke, co-founder and CEO of marketing solutions platform WPIC Marketing & Technologies, told Jing Daily.

With more time to pursue hobbies and spend time with friends, young Chinese are spending more on items that complement a solo lifestyle, including pets and leisure sports, while valuing sustainability, self-care and healthy living, Cooke added.

Auction house Christie’s, meanwhile, has observed an uptick in young consumers from Asia. In 2023, the Asia-Pacific region accounted for 54% of Christie’s global new buyer spending, according to the South China Morning Post. The news service also reports that high-net-worth individuals in China are getting younger. The proportion under 40 years old has increased from 29% in 2019 to 49% in 2023.

Takeaways

- By 2035, China will be home to 400 million people aged 60 and above, comprising 30 percent of its total population, and making it one of the largest ‘senior single’ economies in the world.

- Women are increasingly choosing to stay single as their earning power grows, and their economic influence is contributing to new types of consumption.

- The rise of quiet luxury reflects changing lifestyles and values, with younger Chinese choosing more subtle expressions of luxury over flashier items from bigger brands.

- The Chinese government, meanwhile, is launching a ‘new era’ marriage and childbearing culture to counter its low birth rate across more than 20 cities.

Sourced from Jing Daily, South China Morning Post

Affordability bites for McDonald’s, new value propositions offer an answer

Affordability bites for McDonald’s, new value propositions offer an answer

McDonald’s must be on the side of the consumer and “laser-focused on affordability”, according to CEO Chris Kempczinski.

Context

- He told an earnings call that consumers around the world faced elevated prices across their everyday spending and were being careful – which in turn was putting pressure on the QSR industry.

- “In Q1, industry traffic was flat to declining in the US, Australia, Canada, Germany, Japan, and the UK. And across almost all major markets industry traffic is slowing,” he reported.

What it means

- “We know our customers are looking for reliable everyday value now more than ever,” Kempczinski said.

- “Staying on the side of the consumer and executing against our plan is our model for driving long-term growth regardless of the broader landscape,” he added. “As consumer pressures have mounted we have reacted with agility to proactively meet evolving customer needs.”

- That has included the launch of everyday value menus across many international markets. “Featuring value bundles at various price points, these new offerings provide smaller, more affordable meals to our customers,” he explained.

- McDonald’s will also look to get existing customers to visit more often, leveraging its digital capabilities and loyalty data.

Getting the message across

- “We always have to be finding ways to be driving consumer interest around great marketing plans,” said Kempczinski. “And if we’re doing great marketing, you can grow the business just with your core menu.”

- “When we shift marketing investment from traditional mass media like television, print and billboard ads, to collective investment in modern and digital capabilities to personalise the experience, we drive profitability,” he added.

- In the US, he sees a need to move away from local value messaging to develop “a strong national value proposition that we can then use our media scale to drive high consumer awareness on it”.

Key quote

“We must be laser-focused on affordability, which means good entry-level price points available every day. In the markets where we’re doing this well, the business is outperforming” – Chris Kempczinski, CEO at McDonald’s.

Sourced from Seeking Alpha

Coca-Cola looks to innovation and digital marketing

Coca-Cola looks to innovation and digital marketing

The Coca-Cola Company says it is innovating and delivering bigger, bolder bets, and backing them with digital marketing.

Four types of innovation

- The renovation of core brands, eg Fanta recipe refinements to improve taste.

- Re-engaging with consumers in a novel way to drive relevance of the core brands, eg Coke Creations.

- Product innovations, eg Minute Maid Zero Sugar, Jack Daniels and Coke.

- Non-product-based innovation: eg new bottle/can sizes.

What does success look like

- “We do not set ourselves an artificial strategy objective of ‘it has to be x percent [of sales] from innovation’,” CEO James Quincey told an earnings call. “As it happens, about 25% of the growth comes from innovation, but it is not set that way.”

- “As it relates to product innovation, we have a very clear set of metrics on whether it’s still growing in the fifth quarter after its launch,” he added.

Key quote

“We’re building on our innovations by driving awareness and excitement through an increasingly digital marketing media mix” – James Quincey, CEO at The Coca-Cola Company.

Sourced from Seeking Alpha

Mondelēz seeks to drive purchase frequency

Snack foods giant Mondelēz reports that shoppers in many markets are increasingly price sensitive and, in North America especially, purchase frequency is down in certain categories.

Squeezed consumers

- CEO Dirk Van De Put told an earnings call that “penetration is still pretty good, but people are much more conscious about price points”.

- “The [purchase] frequency is coming down,” he reported, “particularly with the lower income consumers, and particularly the brands that are important for them.”

- Sensitivity to absolute price points is leading many consumers to choose smaller pack sizes in biscuits and chocolates.

- Additionally, in North America, Mondelēz is seeing increased promotional intensity combined with a significant shift in sales to non-tracked channels, including club stores, dollar stores, and emerging e-commerce platforms.

What Mondelēz is doing

- The business is increasing advertising & commercial spending year-over-year in the high single-digits, “which is driving consumer and customer loyalty”.

- It is increasing total distribution points which it anticipates will help maintain or increase volumes and market share.

- It is launching additional multi-packs, but also reducing the size of some multi-packs from six to five or from 12 to 10 in order to hit particular price points.

- “For those lower income consumers who are buying very carefully and evaluating very carefully when and what and at which price they buy, we will need to become more agile in the promo mechanisms that we will play out,” said Van De Put.

Key quote

“What we need to do going forward,” said Van De Put, “is largely [about] trying to figure out in which way can we get the frequency, particularly from the lower income consumers that we would like to see.”

Sourced from Seeking Alpha

Super Bowl spots often lack memorability

Many Super Bowl ads struggle to achieve top-of-mind memorability with consumers just weeks after the big game, according to research by Spikes, the innovation consultancy.

Why Super Bowl spots matter

Big-budget ads that run during major events and occasions are a useful way of attracting eyeballs and generating short-term buzz. Better understanding the half-life of these commercial spots can help marketers determine if they truly represent value for money.

- Spikes polled 2,000 consumers in the US around two weeks after the NFL season-closer, where ad inventory costs millions of dollars, and got them to name an ad they recently watched...

This content is for subscribers only.

Sign in or book a demo to continue reading WARC’s unbiased, evidence-based insights that save you time and help you make marketing choices that work.

Radio is a cost-efficient way of boosting performance campaigns

Radio is a cost-efficient way of boosting performance campaigns

Radio advertising boosts daily web sessions by 9%, according to new research from Radiocentre into its performance marketing capabilities.

A study from the industry organisation, Radio: The Performance Multiplier, also finds that, on average, radio generates additional web sessions twice as cost efficiently as other demand generation media combined.

Takeaways

- Only 8% of a radio spot’s full potential effect is delivered in the first 20 minutes following transmission – meaning that 92% of radio’s effect is excluded by typical short-term time-window attribution approaches.

- Reallocating budget from other media into radio can turbocharge typical pure-play online performance channels, including organic search, paid search and paid social, at no extra cost.

- The best-performing campaigns are characterised by higher weekly reach and consistent use of distinctive audio brand assets.

Why it matters

Two things. Firstly, current measurement techniques appear to underestimate radio’s influence on performance outcomes – and that could be holding back investment in the medium.

Secondly, reallocating budget to radio may help brands break through the ‘performance plateau’ – the point at which the success of a traditional mix of search, social, and online display begins to level off and long-term growth is stifled.

About the research

Radiocentre and research agency Colourtext used regression modelling techniques to analyse the effect of 1.6 billion multimedia impacts on 30 million web sessions, sourced from a range of in-market campaigns, with the aim of deciphering radio’s true effects within the performance marketing mix.

Sourced from Radiocentre

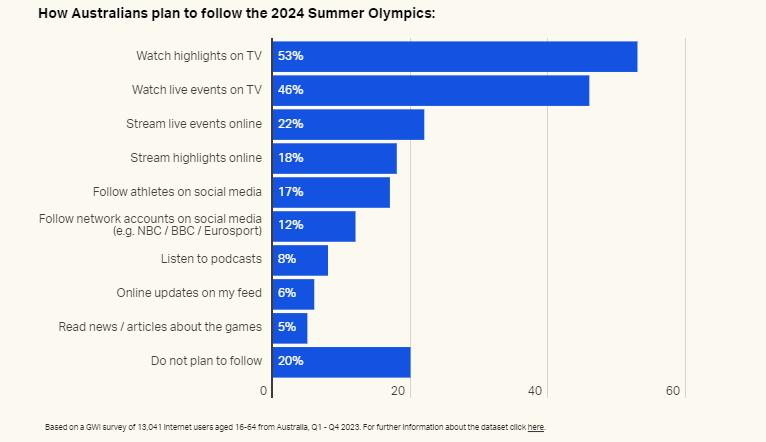

How Australians plan to tune in to the 2024 Summer Olympics

WARC’s latest Spotlight Australia infographic shows that the majority of Australians plan to follow the Olympics this year, with approximately half the country planning to watch either live events (46%) or highlights (53%) on TV, making it the most popular channel for engagement.

Only one in five says they have no plans to watch the sporting event at all.

Why live sporting events matter

Marketers increasingly prize sport for its ability to drive mass reach. Last year’s FIFA Women’s World Cup broke Australian TV viewership records during the Matildas’ semifinal match with England, drawing 11.5 million viewers...

This content is for subscribers only.

Sign in or book a demo to continue reading WARC’s unbiased, evidence-based insights that save you time and help you make marketing choices that work.

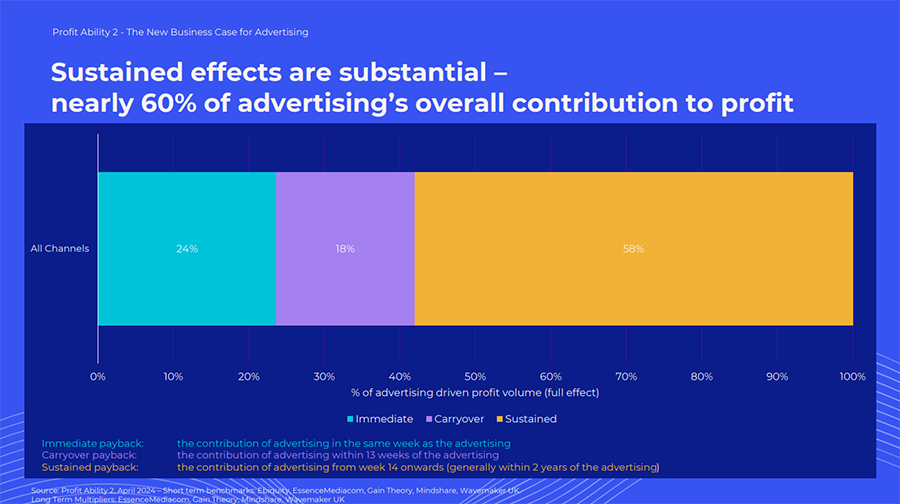

Beyond brand vs performance

Thinking in terms of brand-building or performance-driven channels ignores how advertising really works, say the authors of a major new report into the business effects of advertising spend; instead, there are three critical dimensions that marketers need to start considering.

Why new dimensions of effectiveness matter

Brand and performance have been useful groupings for channels’ respective effects, but at a time when driving value is becoming as, if not more, important than driving volume, the authors believe that much more nuance is needed when planning and modelling the full effect of advertising spend, given the long tail of effects (pictured)....

This content is for subscribers only.

Sign in or book a demo to continue reading WARC’s unbiased, evidence-based insights that save you time and help you make marketing choices that work.

How Athletic Brewing tapped the power of marketing mix models

Athletic Brewing, the non-alcoholic craft beer manufacturer, has tapped into marketing mix models to help find the right balance of growth and profitability.

Why a marketing mix model matters

Rigorously examining budget allocation can help brands better understand how to boost return on investment (ROI) and reduce non-essential spending. Marketing mix models are one way of achieving this objective at a granular level.

- As a seven-year-old company in what has become a fast-growing category, Athletic Brewing faced the challenge of driving growth in a profitable way.

- It partnered with Keen Decision System, an omnichannel marketing mix model provider that also...

This content is for subscribers only.

Sign in or book a demo to continue reading WARC’s unbiased, evidence-based insights that save you time and help you make marketing choices that work.

Connected TV and retail media central to this year’s US upfront

Connected TV and retail media central to this year’s US upfront

The US upfront is expected to be a seller’s market this year because of an improved economy, tighter inventory due to the Olympics and presidential election, and no writer’s strike, according to data from Advertiser Perceptions.

Channels including connected TV and retail media are also expected to be a greater part of the mix.

Why the US upfront sales matters

The annual upfront TV ad sales season in the US is a key indicator of the health of the media and marketing ecosystem, taking into account the popularity of programming, the size of ad budgets, the state of the overall economy, and how new media channels fit into the overall picture.

Takeaways

- Advertising Perception’s (AP) March survey of 156 US advertisers who influence upfront video budgets showed that 34% plan to increase their upfront allocation this year, and anticipate allocating a median of 45% of their upfront video budgets to CTV, up from 40% a year ago. AP believes CTV spending will outpace national linear by 2026.

- Access to media brand data (including retail data) has emerged as the number one reason advertisers say they plan to purchase TV inventory during the upfront, with brands expressing interest in products built on streamers’ first-party viewing data, retailer sales data or ACR (Automatic Content Recognition) data from Smart TV and streaming device providers.

- As currency solutions besides Nielsen receive accreditation from the Joint Industry Committee (JIC), only 41% of advertisers say they plan to transact solely on traditional currencies; 59% plan to use alternative currencies either alongside Nielsen demos or exclusively.

Key quote

“For buyers, CTV will be a more central part of upfront conversations than in years past. And with the Olympics and presidential election this year, advertisers may need to be more aggressive with their plans than in prior years if they want to lock in with specific inventory at guaranteed rates” – Eric Haggstrom, director of market intelligence, AP.

Time for FMCG brands to stand up in the plastics debate

Time for FMCG brands to stand up in the plastics debate

Some of the world’s biggest FMCG manufacturers have been making encouraging noises about how they are addressing the problem of plastic pollution but more radical change is needed than keeping screw tops attached to drinks bottles.

Context

- The UN is aiming to conclude a global plastics treaty by the end of this year which would manage plastics over their lifecycle.

- The Intergovernmental Negotiating Committee on Plastic Pollution has this week advanced discussion from ideas to treaty language, including limiting the total amount of plastic produced.

- Nearly 400 million tonnes of new plastic is produced every year, according to UNEP estimates, and that total could double by 2040; plastic also accounts for 5% of global emissions currently but that could rise too.

- The UN estimates that less than 10% of plastic generated globally gets recycled. And recent research from The 5 Gyres Institute concludes that for every percentage increase in plastic produced, there is an equivalent increase in plastic pollution in the environment.

Takeaways

- The Institute also found that 56 FCMG multinationals were responsible for at least half of the world’s plastic litter (the half of the 1.87 million items collected over a five-year period across 84 countries that had discernible branding); Coca-Cola alone was responsible for 11%.

- Most of the rubbish collected was single-use packaging for food, beverage, and tobacco products.

- In a recent earnings call, Unilever claimed to have reduced virgin plastic use by 18% over the past year, while increasing use of recycled plastic by 23%.

- Tradeable plastic credits, which would allow companies to balance the plastic waste they collect against the waste they produce, are seen as an answer by some companies.

Why plastic pollution matters

Virgin plastic is being produced faster than old plastic is being recycled and the world is awash – literally – with the results. FMCG brands and their single-use plastics are a major contributor to the problem and will play a crucial role in solving it. But as Unilever CEO Hein Schumacher noted, brands can’t do it alone: “You need the cooperation of retailers [on refill and reuse], you need the cooperation of governments in terms of law change.”

Sourced from Guardian, Financial Times, Globe & Mail, Seeking Alpha, AP

UK consumers concerned about political advertising

UK consumers concerned about political advertising

Data from UK advertising thinktank Credos shows 44% of people are concerned about political advertising, with people significantly less likely to trust political advertising (29%) than all/commercial advertising (39%).

Key stats

- Almost three-quarters of people (73%) believe that political advertising should be subject to the same rules and regulations as other forms of advertising (12% disagree and 14% don’t know).

- Two in five people (39%) believe there is too little/no regulation, while a third (33%) think it’s about right, 10% think there is too much, and 18% don’t know.

- Young people are most likely to trust political advertising (48% of 18-34s compared to just 13% of over 55s), but also had the highest levels of concern (49% of 18-34s compared to 44% of all people, 46% of 35-54s and 38% of 55+).

Why political advertising matters

With local elections in the UK this week and a general election expected within months, political advertising is a topical issue. In this climate, parties dispute the veracity of each other’s material and the editing of video destined for social media often presents a misleading picture of the other side’s intentions.

And the problem extends well beyond the UK. In Europe, regulators may be about to open a probe into Facebook and Instagram over concerns that Meta’s brands are not doing enough to counter disinformation coming from Russia and other countries that could undermine upcoming European Parliament elections.

What next?

- Media Smart, the advertising and media industry’s education programme, has partnered with the Advertising Association, the UK advertising industry trade body, to publish What’s the deal with political advertising?.

- The new 10-point guide aims to help people, especially young people preparing to vote for the first time, improve their political literacy and understand the ads they see.

- An awareness campaign will be delivered via AA and Media Smart channels online to help promote the guide, as well as through five ad executions in 300 universities and colleges through a partnership with Next-Gen Media.

Sourced from Media Smart, Financial Times, Huffington Post

Brand admin costs UK consumers £3bn a year

Brand admin costs UK consumers £3bn a year

Almost half of Brits (49%) consider brand admin (‘brandmin’) – tasks to manage their accounts or interactions with brands – to be a significant chore, but choosing to save time by ignoring it costs money.

That’s according to research from custom engagement platform Twilio which identified the most irritating experiences consumers have to endure and which have led to around half having lost their patience or becoming emotional.

‘Brandmin’ time drains

- Being put on hold (43%)

- Being passed around departments or incorrectly transferred (43%)

- Lengthy resolution processes (27%)

- Multi-factor authentication (25%)

- Complicated returns processes (22%)

- Being forced into interactions on channels they don’t want to use (18%) or having to reach out at inconvenient times (19%)

Time is money

- UK consumers spend 45 minutes a week on average on such ‘brandmin’ tasks, amounting to over 1.5 days a year.

- Almost half (47%) have given up on such tasks entirely, citing the time taken or the frustrations endured.

- Brits lost an average of £95 each in the last year at their expense – or £3bn collectively.

Why brandmin matters

Negative brand experiences inevitably have an effect on loyalty and word of mouth, as consumers complain to family and friends and choose to take their business elsewhere.

So what’s the answer?

- While it’s no surprise that brands will reach for AI to help create more streamlined customer engagement, it seems that consumers are also banking on new tech to solve the problems created by old tech.

- Over the next 12 months, customers are hoping AI can shorten waiting times (34%), provide 24/7 customer service availability (34%), put them through to the correct department the first time (28%), automatically verify their identity (22%), streamline or automate changes or cancellations to contracts (18%), or streamline resolutions to complaints and product faults (17%).

Key quote

“Brands need to rise to the occasion and remove the ‘time drain’ tasks that seem to go hand-in-hand with being a customer. Helping customers reach resolutions is the answer – it’s as simple as that” – Sam Richardson, Customer Engagement Consultant at Twilio.

Sourced from Twilio

Marketers need more AI training

Most people in the digital marketing industry are already using or experimenting with GenAI, but there’s a need for more training, according to new research from IAB Europe.

The industry body partnered with Microsoft Advertising for a survey* that leveraged IAB Europe’s network of national IABs and corporate members.

Key findings

Generative AI (GenAI) is set to revolutionise digital advertising by automating tasks, personalising content, and enabling data-driven decisions.

- Nine in ten (91%) respondents are already using or experimenting with GenAI.

- Four in ten (41%) have a specific budget assigned to experiments with and using GenAI.

- Half are fostering AI talent within the team (e.g. upskilling current teams and hiring new talent).

- Additionally, almost one-third said that their company is providing dedicated days and time for team members to learn about AI.

Beyond operational streamlining, professionals are increasingly leveraging generative AI for content creation and creative endeavours.

- More than two-thirds of respondents said they were using GenAI within their business to develop content.

- Half were using it to develop creative.

The study also highlights a clear demand for enhanced education within the industry:

- Nine in ten (89%) respondents called for more training initiatives.

- Additionally, it emphasises the importance of transparency and trust, as stakeholders navigate the integration of AI technologies into their workflows.

Why GenAI training matters

Marie-Clare Puffett, insights & industry development director of IAB Europe observes that while embracing GenAI is essential for staying ahead of the curve, it’s also necessary to address educational gaps and to foster transparency if stakeholders are to harness the full potential of the technology.

*There were 146 responses to the survey, with nearly 50% of respondents having over ten years’ experience working in the digital advertising industry across a variety of departments and markets in Europe.

Email this content