This month: advertising’s winners and losers as the year ends, engaging sports fans during COVID-19 and how mobile video is becoming the focus in Asia.

Triopoly reaches new high but SME advertising struggles

Advertising budgets have been through a whirlwind and the last few months of 2020 look challenging for some.

For Alphabet, Amazon and Facebook, it’s like nothing ever happened. The group’s collective advertising revenue reached $63.7bn in the third quarter of this year, a new high and paving the way for a strong Q4. WARC Data believes the group accounted for 72% of online adspend last year and this looks set to top three-quarters in 2020.

However, the small businesses that many media owners, like Facebook, rely on look less confident.

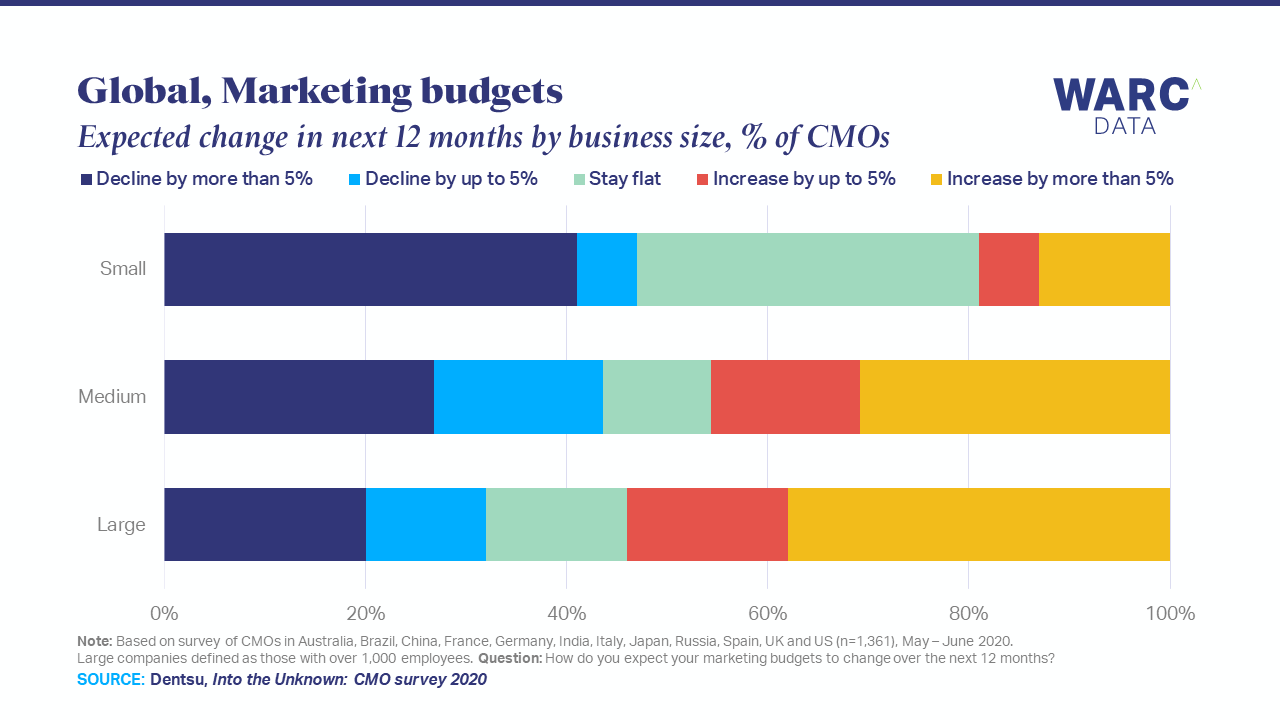

Nearly one-half (47%) of small businesses plan to cut their marketing spend over the next 12 months, with the majority of this being a reduction of at least 5%. In the United States, half of SMBs say the economic situation is ‘poor’.

In contrast, big brands look more confident in bouncing back. A smaller one-third (32%) of CMOs at large businesses, those with over 1,000 employees, plan to cut their marketing budgets over the next year. Instead, over half (54%) plan to raise budgets in an attempt at capturing online shoppers over the Christmas period.

However, half of consumers are set to alter their spending this holiday season so brands are going to need an engaging strategy in order to capture consumer attention. A clear message will be vital, particularly as marketers need to balance the need of some consumers wanting to make Christmas more special with others grappling with financial uncertainty. This mixed messaging and subdued spending presents fresh challenges for brands in an already difficult 2020.

In terms of what this means for the 2020 and 2021 advertising market, WARC Data clients should look out for the latest analysis in November’s Global Ad Trends. The full report will be available at the end of this month, while non-clients can register their interest here.

Engaging sports fans on and off the field

Sport has made something of a post-pandemic return, but clubs and brands are going to have to broaden their approach to keep audiences engaged.

Firstly, fans are still eager to watch matches and tournaments on TV, just as they would before the outbreak. Data from BARC India and Nielsen show that live TV viewing of the Indian Premier League has grown by one-third compared to last year.

However, the strongest growth in viewership was among female and older audiences, suggesting an opportunity for clubs and sponsors to reach a broader demographic than before COVID-19.

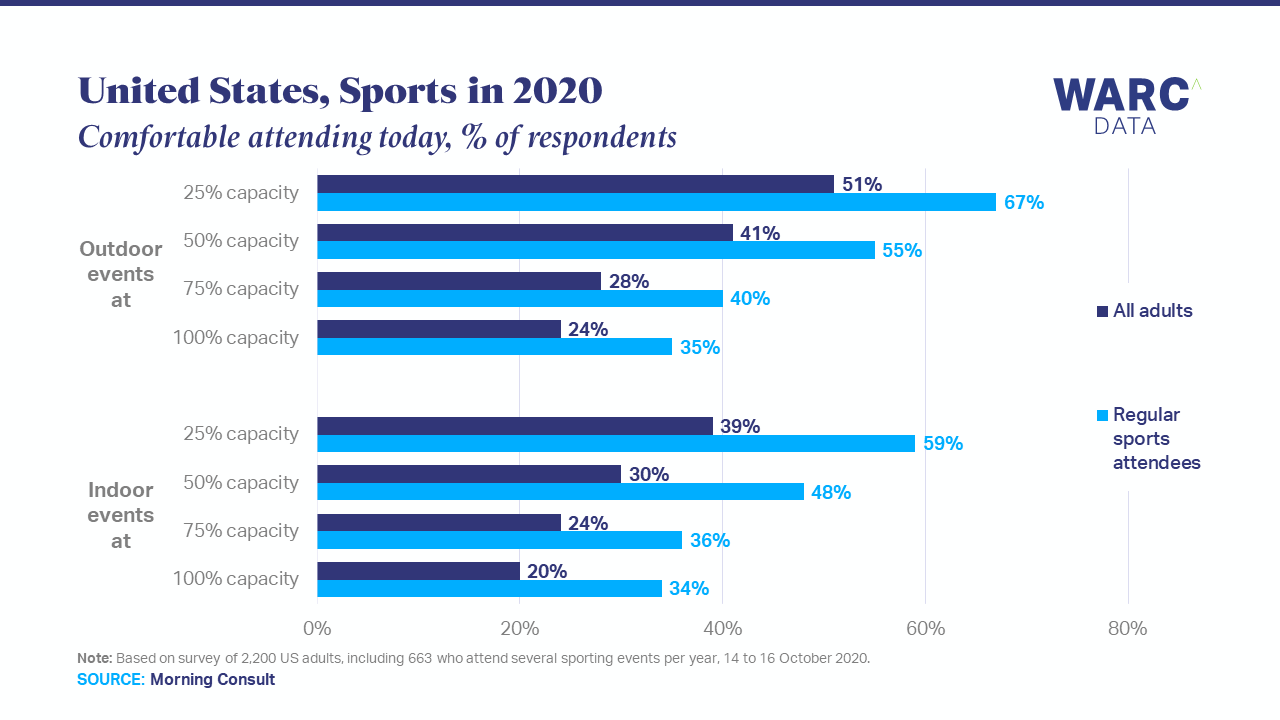

Secondly, sports fans are eager to return to live events but there’s strong interest for digital content as a supporting measure.

Half of Americans (51%) say they would be comfortable attending an outdoor sports event at 25% capacity, a share that rises to two-thirds (67%) among sports fans.

As well as this, one-third of football fans in the UK say they are interested in exclusive or behind the scenes content, the most popular way to enjoy the sport beyond attending matches. A sustained increase in Twitch audiences and hours watched since April also suggests audiences are turning to digital channels for competitive viewing.

As a result, clubs and brands have new opportunities to engage audiences and maybe even attract new supporters. This is particularly important in a year when sports sponsorship investment is expected to fall 37% and brands are looking for ways to add value to their strategies.

There’s evidence of success already. Football clubs Real Madrid and Chelsea offer two contrasting approaches to drive community involvement, while consumer electronics brand Bose shows how to shift a sponsorship strategy from on-field events to off-field digital activities.

However, sports clubs looking to build a direct-to-consumer offering need to be careful – sharing rights with social platforms like Facebook may be a ‘red herring’ and undervalue the content.

Marketers respond to consumer enthusiasm for mobile video

Video activity has seen a rapid boost this year and marketers in Asia Pacific are focusing their budgets and strategy on the format, according to the latest WARC research.

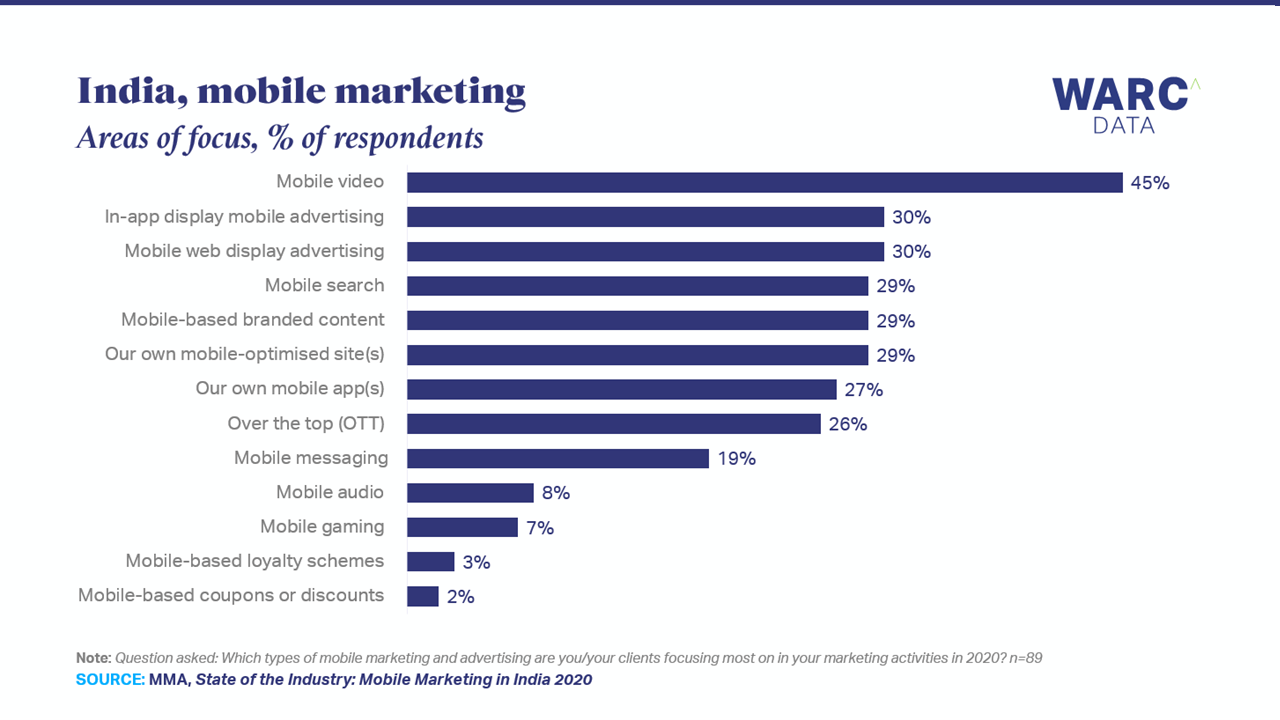

Mobile video is by far the most common area of focus this year for Indian marketers, with nearly one-half (45%) of those surveyed saying so. Brands will be hoping to tap into consumers’ reliance on video platforms for educational and entertainment purposes. Additional research finds YouTube’s Indian audience topping 325 million adults.

However, social video proves most important in Indonesia – almost one-half (46%) of marketers say live social content is one of the most significant consumer behaviours for the marketing industry.

Mobile commerce follows in second, at 44%, though Indonesian brands shouldn’t view these two as separate. Livestreamed commerce provides audiences with an opportunity to watch entertaining video content and discover new products.

Brands have responded with stronger investment as well – half of marketers in Asia Pacific allocate at least 25% of their budget to mobile marketing, an eight-percentage point increase from 2019.

However, this will be wasted investment if marketers don’t identify the right metrics to track – half of those interviewed believe metrics and measurement to be the biggest barrier to growth.

WARC Data clients can access the latest research on mobile marketing trends in Asia Pacific, India and Indonesia while a free sample report can be downloaded here.