COVID-19 has upended adspend forecasts. Here, James McDonald, WARC Data’s managing editor, explains the reasoning behind the revised outlook presented in the latest AA/WARC Expenditure Report.

It was with no great joy that we yesterday (April 30) published the latest projections for how the novel coronavirus outbreak (COVID-19) has impacted UK advertising.

The figures are sobering: ad investment is set to fall 16.7% – or £4.2bn – from its 2019 peak to a total of £21.13bn this year. The deterioration of advertising trade, we believe, will be focused primarily in the second and third quarters of this year, though the aftershocks are expected to last into the fourth and early 2021.

While we anticipate growth for 2021 as a whole it will not be enough to offset the deficit this year. Indeed, ad investment would need to rise by a further 5.6% in 2022 in order to match the 2019 total but, while this is on a par with growth rates prior to the outbreak, it cannot be assumed when post-Brexit trade negotiations are ongoing.

Our projections are based upon the information we are receiving directly from the industry –including through conversations with media owners and agencies. However, given the rapidly changing pace of this downturn, they must be taken as no more than guidance.

Here we take the opportunity to explain the reasoning for our outlook by key media and formats.

Paid search

Spend on paid search rose by 17.8% – or £1.2bn – to a total of £8.0bn last year. The format now accounts for almost one in three pounds invested in advertising in the UK – Google continues to be the main beneficiary.

We believe growth in the search market eased to 9.2% during the first three months of the year, a rate that is in line with Google’s earnings release on Tuesday. Parent company Alphabet did not provide guidance for Q2 2020 performance, noting only that it would be “a difficult one”. We expect search spend to fall by as much as 30% during the quarter – the first recorded decline within the sector.

The format is relied heavily upon by the small and medium sized enterprises (SMEs) whose ad budgets have evaporated as a result of deteriorating economic conditions. Pivotal Research estimates as much as a half of Google’s ad income is from such businesses, and their recovery is likely to be far slower than more established brands over the coming quarters.

Further, performance marketing is simply no longer practical for a number of large product verticals, most notably travel & tourism and automotive. Overall, we expect paid search investment in 2020 to come in 12.1% lower versus 2019, at £7.0bn.

Television

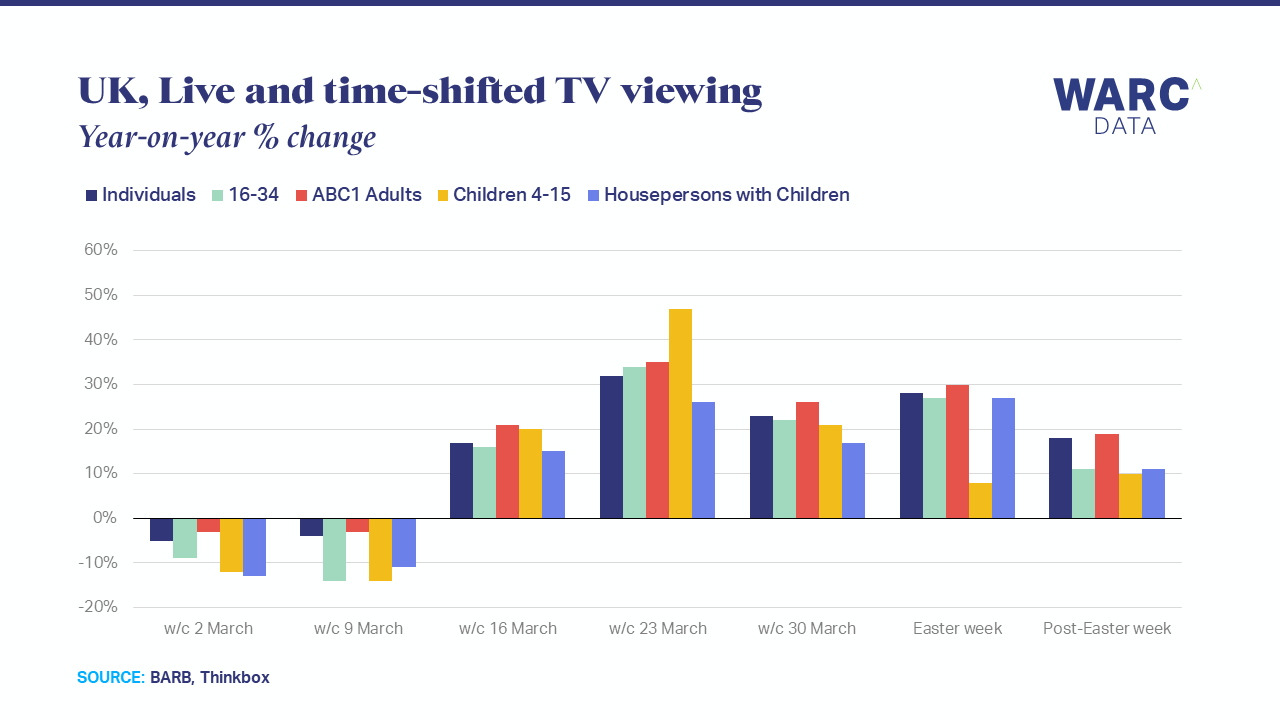

Data from BARB and Thinkbox show live TV viewing has grown by 22.7% on average since 9 March, but our conversations with the industry lead us to believe the TV ad market will contract by almost a half in the second quarter.

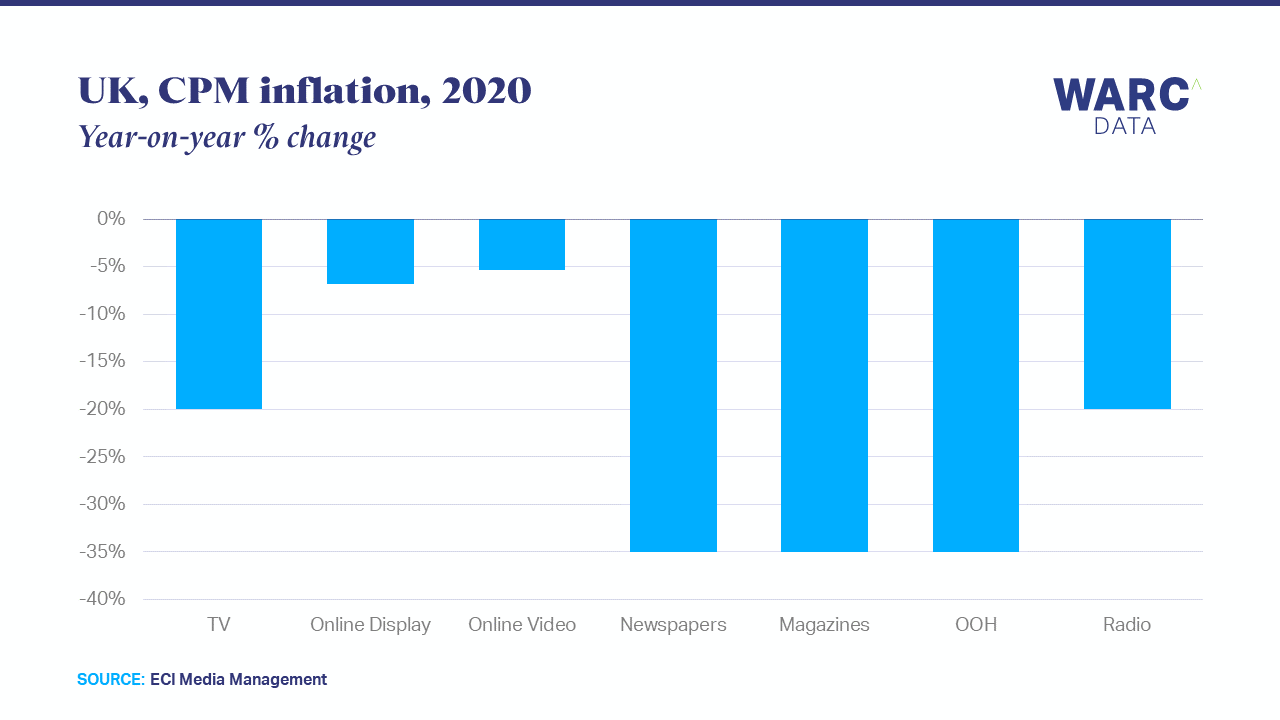

CPM projections from ECI Media Management show costs falling by a fifth in 2020 due to reduced demand, and our full-year forecast for TV ad investment growth is now -19.8%, equivalent to a £976m reduction in broadcaster revenue versus 2019.

The feasibility of producing or adapting creative in the present conditions means many brands simply cannot advertise. Aside from the product sectors currently experiencing paralysis, the postponement of live sport has also hit the market in the short term. The volume of gambling ads – core to sporting content – is also set to reduce heavily as part of an agreed moratorium with UK government.

ITV is looking to practical solutions during this difficult period, with chief executive Carolyn McCall stating the pandemic can be used as a “catalyst” for a new approach to content creation. Partnerships, such as those with JustEat and BT, enable branded content which specifically addresses viewers’ lives during lockdown.

Britbox is also providing a new revenue stream. While the BVOD ad market is projected to be down in line with the wider industry over the coming months, its rebound is expected to be stronger than most at +21.9% next year.

Social media

Advertiser investment in social media has grown continuously since monitoring began in 2014. Spend rose by almost a quarter in 2019 to a total of £3.6bn – equivalent to 14.1% of all UK adspend. IAB data show that the vast majority of investment is directed towards video formats.

The money is following eyeballs. IPA research finds that social media accounts for almost a quarter (23%) of weekly commercial media time among all adults, rising to a 39% share among 16–34 year-olds. In 2015, shares were 18% and 29% respectively.

We estimated that social spend rose 17.0% in the UK in Q1 2020, which was bang on Facebook’s global earning’s release yesterday – though EMEA growth stood at 15.6%. Facebook reported strong rises in gaming advertising and stability in the technology and e-commerce categories – those still spending have been helped by a lower CPM (down 16%) due to a reduction in demand. Travel and automotive brands have cut spend markedly, though, and this has continued into April.

Despite strong performances historically, we do not believe social media to be shielded from the present downturn for reasons similar to paid search. Pivotal estimates that SMEs – those most vulnerable at present – account for two in five dollars spent on Facebook ads. We feel then that social media is also set to record its first annual decline on record during the second quarter.

Out of home

The out of home sector is among the most directly affected, with lockdown restrictions severely impacting reach. Research by Kinetic – based on measurement of device traffic in OOH locations – shows a 76% reduction in roadside impressions during the week commencing 6 April.

Some campaigns – including health-orientated public service messaging from the government – continue to run, but we believe the market value will fall by just over a half – or £163.5m – during Q2 2020, a quarter (24.5%) in Q3 2020, and 18.7% during 2020 as a whole.

Digital out of home – now over half of the market – is one of only two advertising vehicles that are expected to recoup losses entirely next year.

National Newsbrands

Visits to premium UK newsbrands are up by between 30% and 60%, depending on the property, according to industry body Newsworks. This has not translated into rising advertising investment, however, partially because many brands are blacklisting COVID-related keywords when buying audiences so as to avoid the risk of negative adjacency.

WARC has surveyed national and regional newsbrands directly every quarter for over 40 years, so we are well-versed on the industry dynamics. Business pressures are indeed immense; perhaps sometimes forgotten when viewing the world through a mathematical lens there is, of course, a human cost to what the industry is experiencing. A high proportion of editorial staff have had to be furloughed, with many more taking temporary pay cuts.

Advertising revenue among publishers of national news is expected to fall by 20.5% – or £206m – in 2020, compared to the 3.3% decline forecast in January. We see growth returning in 2021 but the absolute increase of £69m would still leave a deficit of £137m when compared to 2019.

Cinema

All cinemas have temporarily closed while lockdown conditions are enforced. We remain hopeful that restrictions are able to be lifted in the second half of the year – aiding a 2.1% rise in cinema adspend in the fourth quarter – but our current projections do not account for this happening before July. As a result, the cinema ad market is expected to contract by 33.6% – or £105m – this year. These losses are expected to be regained in their entirety next year as major releases postponed in 2020 finally make their way to the big screen.

At the end of May, we will be publishing our revised international projections for advertising investment by medium, format and category, alongside new media inflation and consumption forecasts in light of COVID-19. Readers can register their interest for the report here.