The rate of social commerce adoption in Southeast Asia is rapidly accelerating. Neha Khullar and Richard Reid, both of Iris Concise, Singapore, explore some of the strategies to follow.

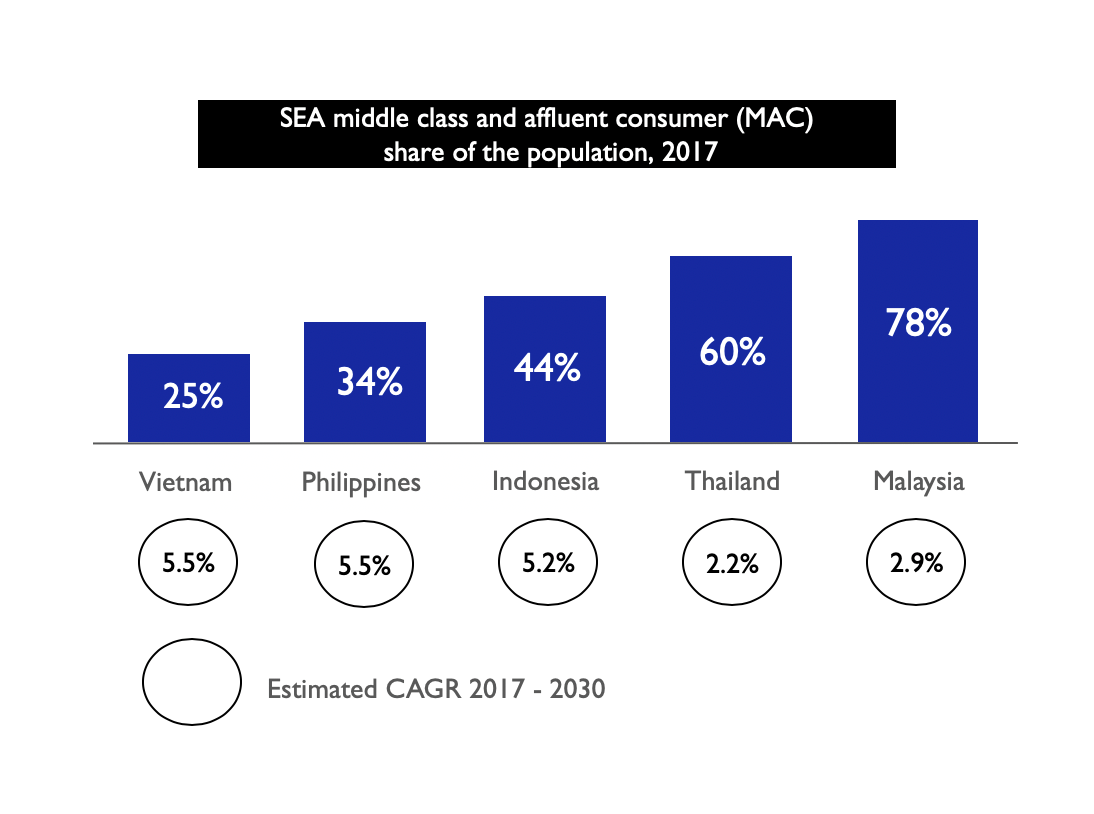

Social commerce accounted for 30% of all digital sales in Southeast Asia in 2016, thanks to a growing middle class and affluent consumer population, eager to exercise its financial prowess by amassing products and experiences.

By 2022, this number is expected to reach 60, fuelled by the entrepreneurial spirit of the region that is propelling micro-SMEs to grow their revenues by selling directly to consumers.

Social commerce involves the buying and selling of products through social media and messaging platforms such as Facebook, Instagram, Line or WhatsApp. Goods may be listed for sale, but payment and delivery are handled elsewhere.

Source: Boston Consulting Group

This gives marketers a unique opportunity and channel to engage consumers. Currently, social commerce plays a crucial role in product discovery and validation phases of the consumer journey. Few consumers today go onto social platforms with the intention to buy, but this will change as buying behaviour is inculcated via three compelling tactics:

1. Conversational commerce:

People are fast tiring of ‘hard-sell’ advertising. For example, Indonesians have the highest adoption rate (63%) of ad blockers in the entire world, up from 2017 when PageFair reported that 58% of Indonesians used an adblocker. Brands are using messaging apps to overcome these roadblocks.

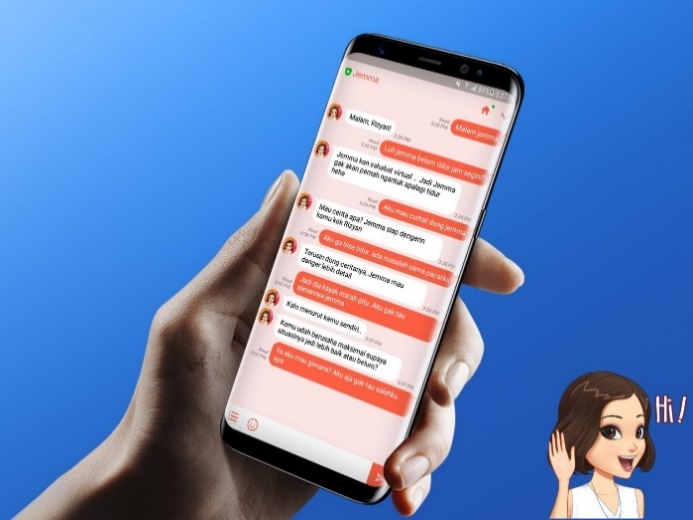

In 2016, Unilever launched a Line compatible chatbot - ‘Jemma’, to have real conversations with Indonesian women about their woes. In less than a year, Jemma managed to befriend about 1.5 million Indonesians who sent more than 50 million messages, effectively opening up a new sales channel for the brand. This significant shift from constant hard-sell to helping consumers discover the right products via a two-way dialogue and influencing the purchase is the true power of conversational commerce.

It’s human nature to want authenticity and younger brands are rising to this challenge in unique ways. They use social channels for live product demos and solve consumer queries via messaging apps – setting the language and expectations of buyer-seller interactions on social platforms.

As ‘chat’ gains prominence in the consumer journey, innovations will streamline C2B2C conversations. For example, Fingo launched in Malaysia in July 2019, allows brands to converge consumers from proliferated social channels, enabling curated one-to-one conversations.

2. Native buying:

Snapchat piloted ‘in-app checkout’ back in 2018 for US-based mobile ticketing platform, SeatGeek. In March 2019, ‘Checkout with Instagram’ was launched followed by ‘Shopping from creators’. Currently in APAC, Shop Now on Instagram links to the brand’s mobile website and the transaction is completed there with Instagram getting no details on cart abandons/drop-outs.

When these features are launched in Southeast Asia, social will truly transform into a marketplace. No marketer will be able to ignore the opportunity of a new sales channel that effectively collapses the consumer journey from first impression to purchase on social.

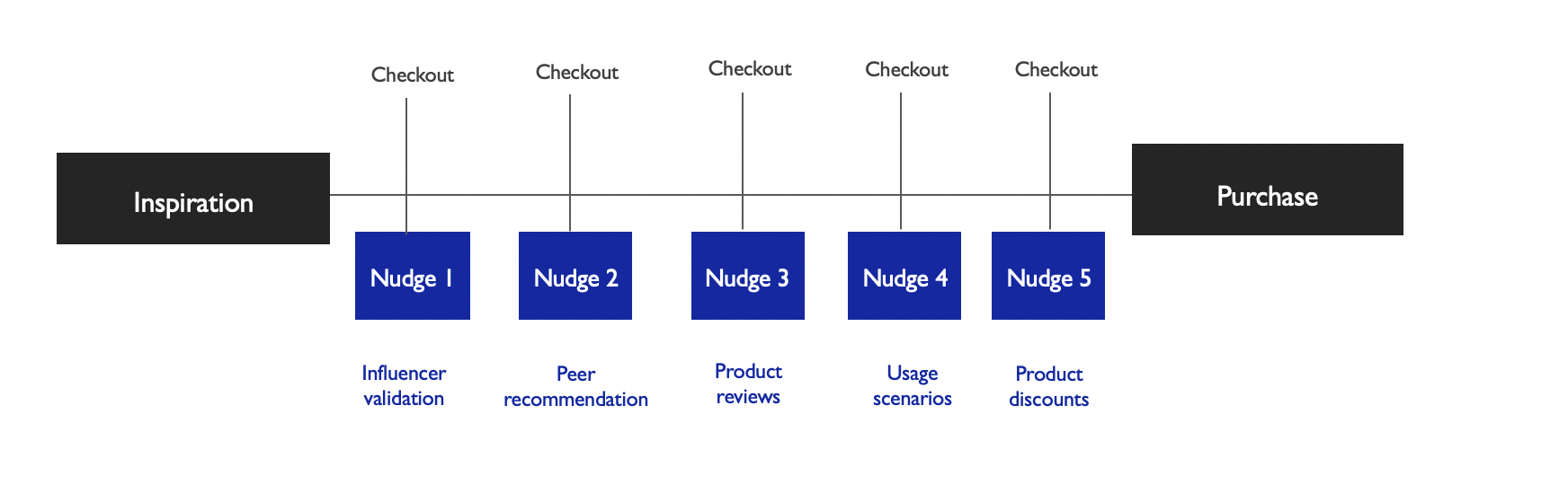

At the onset, it is evident that native buying will enable low involvement product categories to drive impulse purchases. But as native buying features evolve, social platforms will be able to leverage superior behaviour insights to created tighter user journeys, using nudges at each stage.

Source: Iris Worldwide

This will also give companies like Facebook a unique opportunity to nudge consumers from inspiration to purchase within their app ecosystem and demonstrate conversion efficacy to marketers. For example, influencer validation via Instagram, peer recommendations on WhatsApp and product reviews on Facebook.

3. Digital payments:

To fuel social commerce, platforms will provide diverse digital payment options to ensure transactions are completed within their ‘walled gardens’. Facebook materialised this intent on June 18, 2019, by launching its cryptocurrency Libra and digital wallet Calibra. But payments on social in this region will need to adapt to the unique dynamics of Southeast Asia, where cash on delivery and regional payment platforms dominate.

For example, in Thailand, Facebook partnered with Qwik, a digital payment service that provides a seller’s bank account details to interested consumers and facilitates ATM payments.

According to a 2018 Paypal report, homegrown platforms are surfacing as a preferred mode of social payment by merchants. In the Philippines, GCash is used by 54% and PayaMaya by 39% of the merchants. In Singapore DBSPaylah! is used by 42% and eNets by 32% of the merchants.

Indonesia is often touted as Southeast Asia’s most valuable untapped market in the digital finance sector because 66% of the country’s 260 million population are 'unbanked’. The number of digital finance apps in the country has grown six times since 2010, bringing the total to 140. Out of these, 19 are from e-money providers that don’t require a bank account and majority of the 18-45-year-olds use them for online shopping. Integrating these payment options will unlock social commerce for a larger segment of the population.

Future forward marketers must scrutinise their ecommerce ecosystem. In the midterm, social commerce is unlikely to replace any digital sales channel. However, a natural evolution of consumer expectations will alter the role of existing ecommerce channels in the product decision making journey.

As social adopts ecommerce features, ecommerce will adopt social features

The bulk of online sales is currently driven by bargain hunting consumers who seek price and product options, playing to the strengths of marketplaces like Lazada and Shopee.

As social commerce evolves, consumers are likely to get accustomed to curated brand journeys which elevate the entire shopping experience. Ecommerce marketplaces run the risk of alienating a significant number of shoppers tired of choice paradox.

To shield threats early on, marketplaces are already improving their app experience by deploying assisted shopping mechanics and strengthening engagement by introducing ‘shoppertainment’. To this effect, Lazada has introduced an in-app livestreaming function and Image Search feature which is used by 500,000 customers daily to find approximately 20 million products. Lazada has also launched gaming for rewards and group buy features to deliver entertaining, social ways of buying to keep consumers hooked to the app.

The winners of tomorrow in the ecommerce landscape will be the ones who understand the interplay between experiential and transactional.

Brand websites will play an assurance and product validation role in the consumer journey

Currently, brand websites are important owned platforms that allow marketers to tag individual consumers and trace their digital journey. However, they are expensive assets that require a hefty investment as compared to other sales channels. Additionally, the role of brand websites is getting muddied with companies trying to do everything on it – provide curated experiences, detailed product information, facilitate online transactions and deliver post-purchase services.

As social commerce evolves, consumers will evolve their shopping journey to fulfil very specific needs via different touchpoints. Product inspiration and post-purchase retention will become far easier to execute via social channels which allow brands to delight consumers in their natural online environments.

However, consumers will seek brand websites for very specific information that third parties cannot be trusted to accurately provide. Therefore, brand websites are likely to evolve into functional spaces offering consumers assurance of company legitimacy and detailed product information for pre-purchase validation. Marketers will have to redesign the UX of brand websites to build trust and cater to specific consumer queries and searches.

While some may argue that the increase in social commerce will drive people away from social platforms, there is no doubt it will significantly influence the ecommerce ecosystem and shopper preferences in Southeast Asia.