YouGov's Ervin Ha looks at how luxury brands have fared in Hong Kong as the ongoing pandemic shifts consumer sentiment and purchase priorities.

The pandemic has undoubtedly had an impact on businesses and consumer spending, and luxury brands are no exception. We took a look at how luxury brands have fared in Hong Kong as of late, and how different ‘categories’ of luxury brands have been impacted, and what the average luxury brand buyer looks like in Hong Kong.

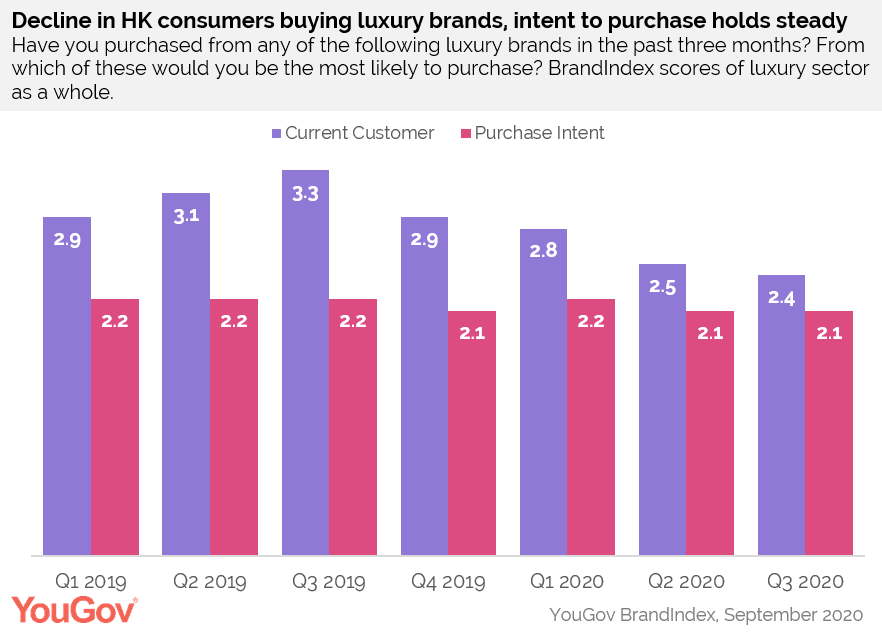

Examining the luxury sector as a whole, our YouGov BrandIndex looks at the Current Customer score, which measures which brands consumers purchased from in the past three months. Comparing the luxury sector’s Current Customer score in 2019 and 2020, there is a clear decline in Hong Kong consumers buying luxury goods as a whole. In 2019, its lowest score was 2.9, but this year its highest score is 2.8. However, though data suggest that fewer people are purchasing from luxury brands, the intent to purchase holds steady. The luxury sector’s Purchase Intent score – which asks which brands people are most likely to purchase, has remained largely unchanged from the year prior.

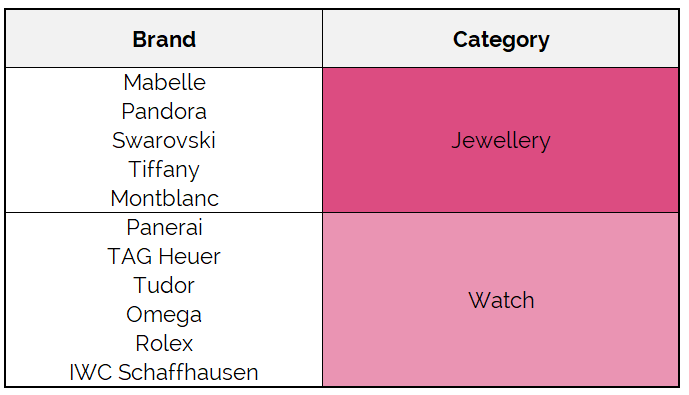

While there has been an overall decline in luxury brand consumers as a whole, not all brands performed the same. In this survey, they have been categorised by ‘Affordable Luxury’ (i.e. Coach, Michael Kors), ‘Accessible Core Luxury’ (i.e. Gucci, Prada) and ‘Premium Luxury’ (i.e. Cartier, Hermes). They have also been categorised under ‘Jewellery’ (i.e. Tiffany, Pandora) and Watch (i.e. Tag Heuer and Rolex).

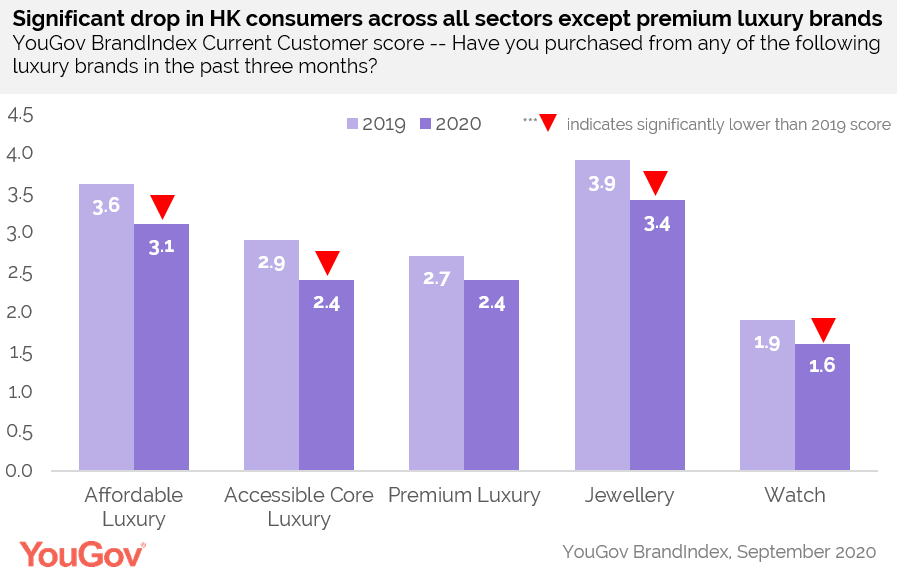

The overall decline in customers for luxury brands is notable across all categories with the exception of ‘Premium Luxury’. It is the only category that doesn’t show a significant drop from the year prior.

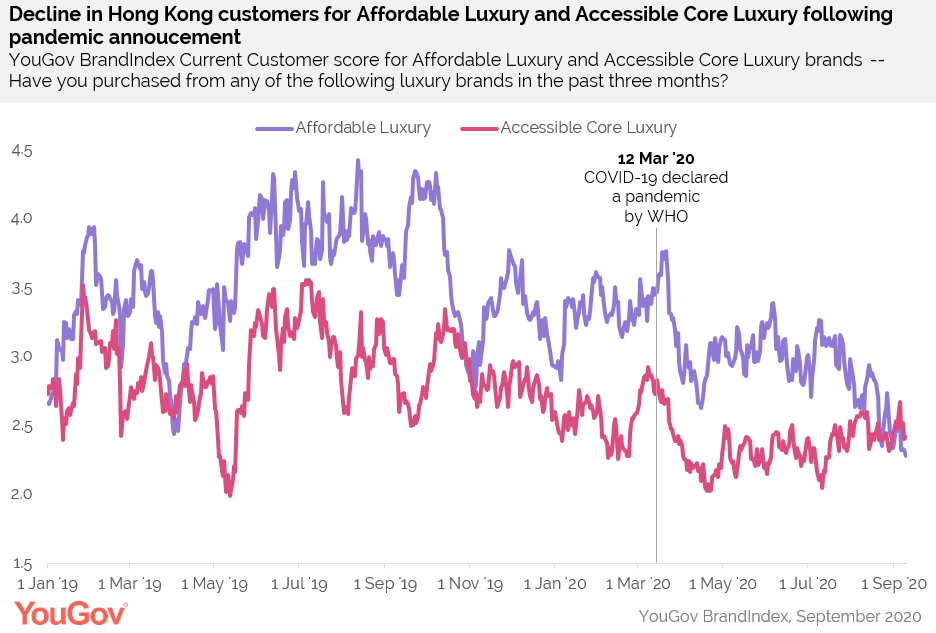

The two categories that were most noticeably hit by the pandemic, however, are ‘Affordable Luxury’ and ‘Accessible Core Luxury’ brands. On 12 March 2020, when the World Health Organisation (WHO) declared COVID-19 a pandemic, the Affordable Luxury sector recorded a Current Customer score of 3.2 and for Accessible Core Luxury, its score was 2.8. Since then both have been on a decline and fallen to 2.3 and 2.4 respectively.

What does the average luxury fashion consumer look like? YouGov Profiles reveals this by comparing demographics between the national population (nat rep) against a luxury fashion consumer. For example, though only 53% of the Hong Kong population are female, 54% of luxury fashion consumers are female – making them more likely to be female than male. They are most likely to have a personal income between HKD 15,000 and 29,000 (41% vs. 35% nat rep). Luxury fashion consumers are also very likely to be over the age of 45 (58% vs. 30% nat rep).

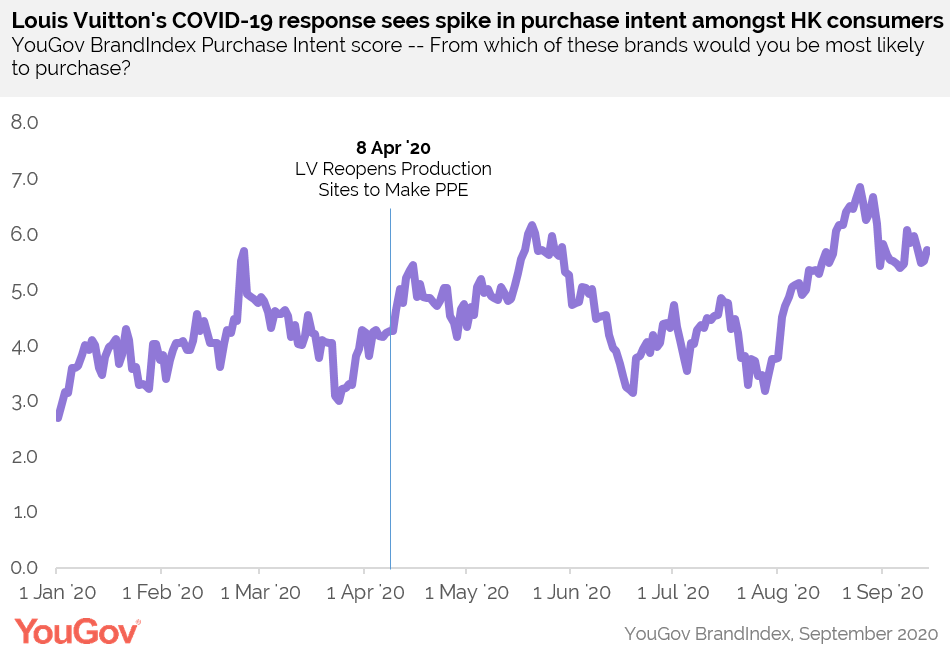

It is not all doom and gloom for luxury brands, however. For one luxury brand, they actually saw an increase in their Purchase Intent score during the pandemic. Early on when the pandemic broke in Europe, Louis Vuitton was the first luxury fashion house to announce that they would be re-opening production sites to make PPE (personal protective equipment). This decision by the brand coincides with a rise in their Purchase Intent score, which has been on an upward trend since. This means that now more Hong Kong consumers are looking to purchase from the brand. Though other luxury brands followed suit, they did not enjoy the same uptick in scores.

Many businesses have been hit hard by the pandemic, and the luxury fashion sector is no exception. There has been a notable decline in Hong Kong consumers buying from luxury brands this year, with the exception of ‘premium luxury’ brands. It’ll be interesting to monitor if this changes in the following year, and if it will be the same profile of luxury fashion consumers post-pandemic.