WARC Data’s latest report finds that Amazon, TikTok, YouTube and Twitch are some of the main winners as brands pivot to reach the COVID consumer.

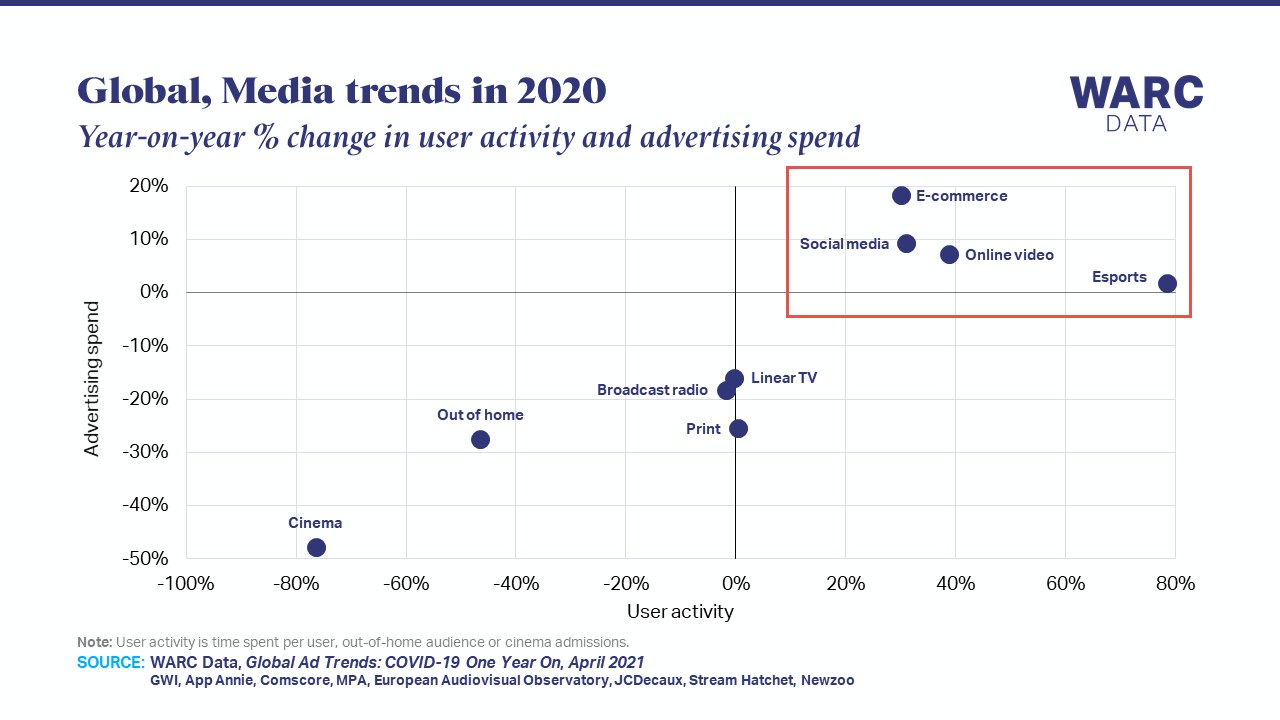

No one doubts that the media disruption from COVID-19 was both rapid and severe, but data suggest that brands were largely able to adapt to the immediate shifts in consumer behaviour. There is a clear correlation between changes in user activity and advertising spend in 2020.

While there was an uptick in consumption for many media during the initial outbreak, this had been nullified within core traditional channels by the second half of the year.

Digital media, however, have proven more attractive to audiences and advertisers.

Research from Kantar suggests marketers are focusing more on innovation, agility and effectiveness, trends that are likely to support further growth in digital media in 2021 and beyond.

E-commerce: $900bn more was spent at online retailers last year

Brands and consumers are both spending more on online shopping platforms, and this shows no sign of slowing. With advertisers wanting to be closer to the point of purchase, data show e-commerce advertising growing 30 times more quickly than the wider online ad market.

This is in response to a clear change in consumer behaviour – online’s share of retail sales more than doubled during the peak of the crisis last year, per figures from the Mastercard Economics Institute.

Each category will feel this differently, though. While some, like automotive, are less suited to online buying, others are experiencing a fundamental change – 75% of the digital shift to grocery will be permanent.

There is still a preference for in-store shopping, though, and there will likely be pent-up consumer demand as COVID restrictions ease. However, the degree to which consumers feel comfortable shopping in store varies across key demographics.

Brands can accommodate these consumer preferences by using flexibility as a strategy. The growing popularity of ‘buy online for pickup in store' (BOPIS), which has seen over a quarter of adults in the USA (26%), Mexico (28%) and India (33%) using the service more, suggests strong audience appetite for convenience.

Brands can use this to their advantage. The physical retail element of BOPIS allows companies to engage their audience a second time and this is particularly important when e-commerce has made it harder to emotionally connect with customers.

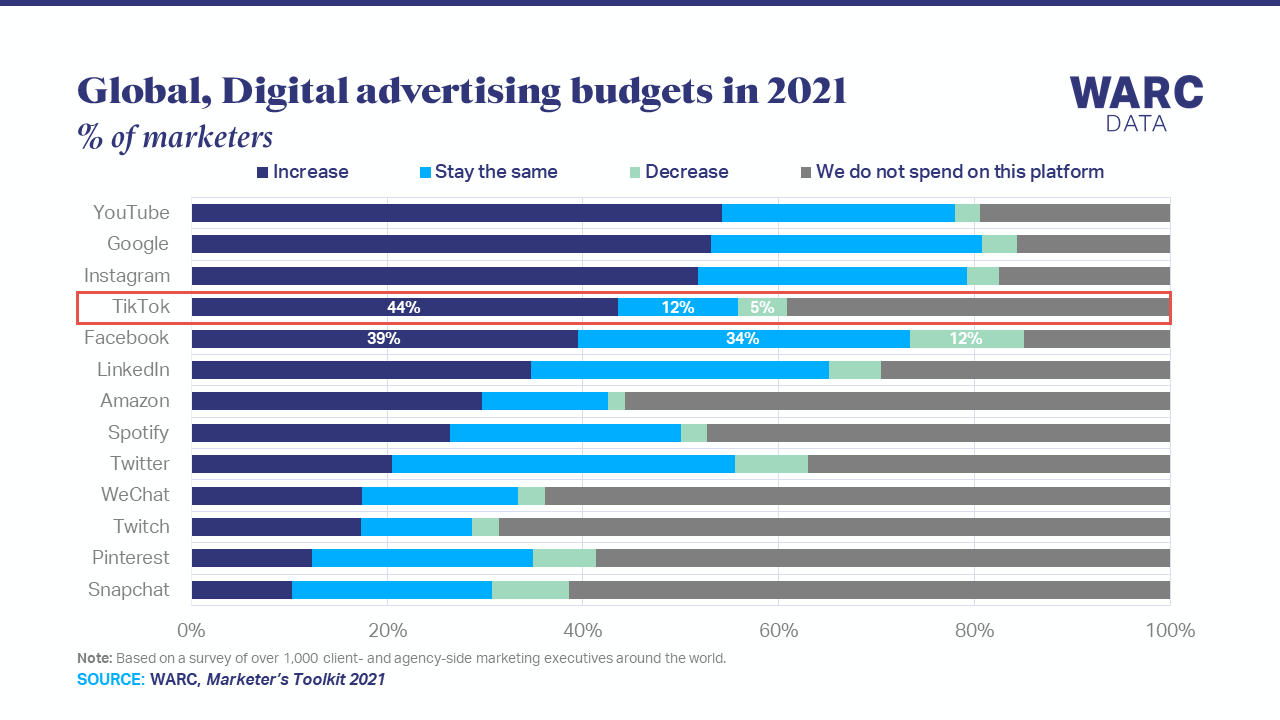

Social media: TikTok was the social winner of 2020 – user activity doubled, and brands are upping their investment

Stay-at-home orders meant there was a heightened demand for entertainment last year, with TikTok filling this need ably. Data from App Annie show that TikTok is now the social app with the highest level of user activity, having overtaken the more information-driven Facebook for the top spot in Canada (TikTok users spend 17 hours a month on the app), France (17 hours), the UK (20 hours) and the United States (22 hours).

Advertisers are also beginning to invest more; findings included in WARC's Marketer's Toolkit 2021, based on a survey of over 1,000 marketers, show that 44% of brands expect to increase spend on TikTok this year, ahead of Facebook's 39%.

Providing entertaining content may feel unfamiliar for some brands, but as TikTok users are expecting spontaneity and ‘fun’, being authentic should be the main focus.

For advertisers that do entertain audiences, TikTok’s new social shopping features mean the gap between awareness, engagement and sales is getting smaller. The first five seconds are crucial in capturing audience attention and brands that use hashtag challenges effectively can expect an impact on offline behaviour as well.

Online video: Linear TV advertising falls an estimated $34bn as YouTube, social video and brand integrations lure ad budgets away

Audiences now watch over 20 hours of mobile YouTube content each month, per App Annie, and this is eroding linear TV advertising investment. As well as this, more than a quarter (27%) of YouTube consumption is via connected TV devices, posing a direct challenge to linear video activity.

While highly creative and effective ideas are more than twice as likely to lead with TV, linear TV’s longer production times and higher ad costs made it difficult to keep up with a fast-changing consumer landscape in 2020.

Audiences are less concerned with these distinctions, though, and care more about quality content than the delivery platform – one in five (20%) consumers globally sees no difference between YouTube and linear TV consumption, per AudienceProject research. This rises even higher in the US (36%) and the UK (27%).

Netflix is also complicating the video landscape. The ad-free streaming platform is drawing audiences away from linear viewing, having added 37 million subscribers in 2020, and can deliver incremental reach for advertisers.

Brand integrations – product placement – are not new but offer a clear opportunity in today’s fragmented media landscape. Beer brand Coors was featured in the hit Netflix series Cobra Kai and reached an additional 13.4 million Americans that avoid linear programming, per Nielsen figures.

Gaming and esports: Brands tap into sponsorships, mobile creative and celebrity collaborations as audiences expand

Although typically perceived as involving only young men, gaming is attracting new audiences and offers brands a variety of creative opportunities.

Gaming-oriented streaming platform Twitch grew rapidly in 2020 and is approaching three million monthly viewers worldwide. This is likely to expand further in the future as gaming becomes more sociable and the platform expands into traditional sports content.

Brands are now recognising the opportunity that gaming presents, with esports sponsorship expected to top $600m this year for the first time, according to Newzoo forecasts.

However, the creative opportunities for brands extend beyond just sponsorship and range from celebrity collaborations and partnerships with hit games like Fortnite through to mobile branded games.

Gaming audiences are receptive to advertising, so brands can expect positive results from their investment – gamers are 7% more likely to say they buy brands they have seen advertised, per GWI. This rises even higher in key Asian markets like Japan (15% more likely), China (10%) and India (9%).

However, a third (35%) of brands say gaming and esports is not an area of greater focus in 2021, suggesting a potential missed opportunity for some.

Global Ad Trends: COVID-19 One Year On

WARC Data's latest report analyses the long-term changes and opportunities in advertising and consumption across e-commerce, online video, social media, and gaming and esports.

A free sample report is available here. WARC Data subscribers can access the full report here.