Appetite for F&B apps shows high growth in SEA, according to data.ai’s latest State of Food & Drink report. WARC Asia editor Rica Facundo speaks to Lexi Sydow, Head of Insights, to unpack the data and uncover the trends driving user acquisition, engagement and innovation in the mobile F&B category.

Key insights

- APAC is still in the user acquisition phase but engagement is setting in, with habits deepening and high downloads observed.

- Video is doing well with a “TikTok-ification” of F&B mobile apps in the shopping and recipe space, making up 80% of downloads.

- While consumers want convenience, they are also becoming eco-conscious which coincides with a larger trend around anti-food waste apps.

Give us an overview: What are the high mobile growth F&B sectors that marketers in APAC should keep their eye on? How are consumers spending their time on these apps?

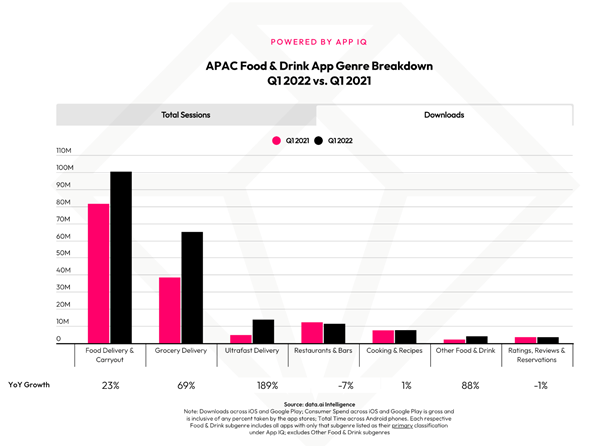

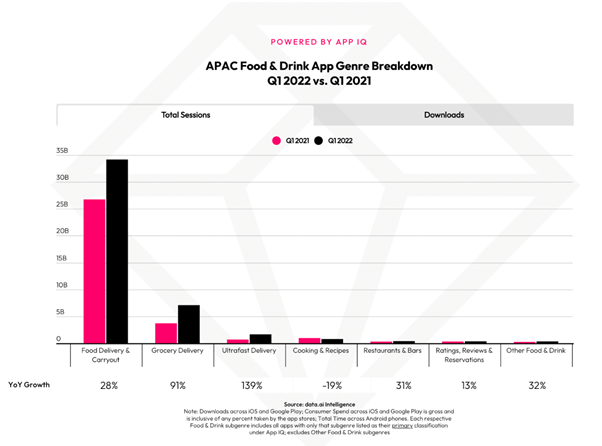

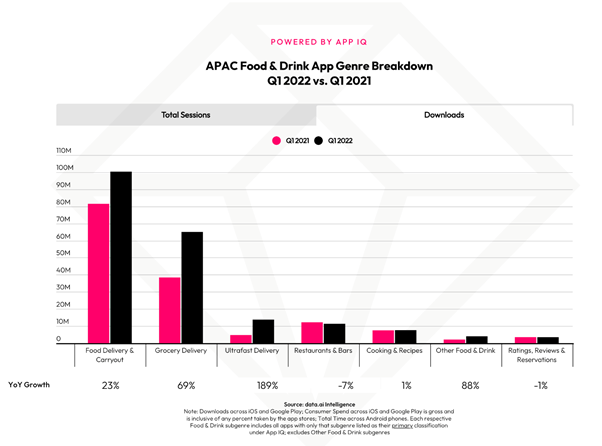

The top performing categories would be in the ultra-fast delivery and grocery segment.

Globally, downloads for ultra-fast delivery grew about 266%. However, its huge growth is still a small portion of the total market, making up only about 6% of the entire market. Whereas in APAC, the growth was strong but not quite that level. It was about 190% year on year for downloads. Additionally, downloads for grocery delivery was about 40% growth year on year globally, with about 62% growth in APAC.

We see really strong growth in sessions and APAC in general. We’ve seen double-digit growth across the board for the Philippines, Singapore, Thailand and Indonesia.

The sessions follow a similar skew to downloads with food and grocery delivery. Each session is an opportunity to purchase, research or check on the status of your order. In the ultra-fast space, there is the element of gamification in the sense of checking to see where your order is, which increases the number of sessions as well.

What stage of growth is the APAC market now?

It’s still a big spectrum where emerging markets, like India and Indonesia in particular, will still be more in the user acquisition stage. A part of that is due to the fact that more people in emerging markets are getting devices for the first time or upgrading their devices.

But in general, APAC would still be more in the user acquisition phase. However, we’re seeing a bit of a duality. Engagement patterns are starting to set in, habits deepening and beginning to ingrain but we’re still seeing high downloads, which tell us that the window is still open to be competitive in that space.

What surprised you the most about the immense growth in the mobile F&B category in APAC?

It’s not just what categories but what metrics. A lot of our usage habits were catalysed during the pandemic. Now that we’re starting to transition out of the pandemic, the question is where does this leave consumers? Do people’s habits stay?

That’s why one of the surprising things we saw was that there was still a very high level of downloads, where brands were still acquiring new users and getting people into mobile food and drink as a whole. In APAC, downloads year on year from Q1 2021 to Q1 2022 grew about 30%.

Beyond downloads, another surprising trend was about the sessions and the engagement behind those apps. Time spent globally grew 65% year on year, which is eight times faster than download growth for the sector.

This shows us that our “post-pandemic” habits have held strong and that using these apps has become part of our daily routines. When you use something like food or grocery delivery, you’re touching on things that are habitual. People eat three meals a day and have to do grocery shopping say, once a week, if not more frequently.

What tactics or features do you see working well for user acquisition and engagement in APAC?

Some of the main tactics that stand out are the strategic use of recurring subscription and auto renewal. In the grocery space, there’s a way you can do that in the app itself, where it might not be that you are subscribing to the entire grocery cart but there might be items that you’ll regularly need, such as milk once a week. This is a good way of encouraging repeat usage and delighting customers – they’re not having to remember those staple items.

From an engagement perspective, we are also seeing video features doing well and that’s something that spans beyond food and drink. It’s like a “TikTok-ification” of F&B mobile apps. We see it in shopping and in the recipe space, where a lot of recipe apps do well in many markets in Asia. This dovetails really nicely into groceries.

Overall subscription and auto renewal removes friction that can be used as a retention mechanic, whereas using video is a tactic for engagement.

Any notable local brands that are innovating in the space?

Cookpad Indonesia, a cooking and recipe app, was one of the breakout apps by downloads in Q1. Cookpad International was second for monthly active users in Q1 and then as a breakout app was second for downloads.

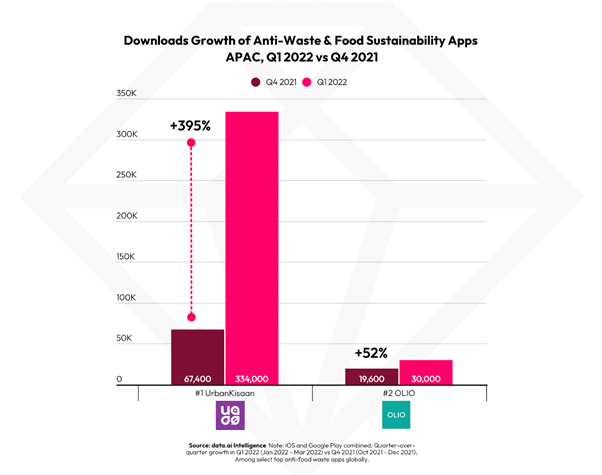

There’s also the Surplus Food Rescue app in Indonesia, which is an anti-food waste app. This is another area that we’ve seen grow across the board. Anti-food waste apps connect you to other people or businesses to get reduced or free food that may otherwise have gone to the landfill. The mechanics vary per company but it usually comes at a cost benefit for the user – maybe it’s free or given at a reduced price, and you’re supporting a local business or helping out a neighbour.

What are the trends that will shape the future of this category?

At the end of the day, delivery is the cornerstone of what people are wanting from their apps. It makes up about 80% of all downloads. But there are a few interesting trends.

- There is a larger trend around being climate aware, where sustainability, direct-from-farmer or agri grocery apps fall into.

- And then you see this converging with the rising trend of cost consciousness happening in the last quarter due to the rising price of gas.

There might be cases where the cost gets passed on to the consumer in the end, such as delivery fees going up. But part of the reason why people subscribe to these providers is that they want to get “free” deliveries. From a consumer behaviour point of view, food delivery services could also be one of those cases where they will just order this meal so that they don’t have to waste their own fuel – especially if the user subscribes to a food delivery service and doesn’t pay a fee “per delivery”.

The rise of anti-food waste apps is also another indicator of rising cost-consciousness in the category. The mechanics of each are very different. But it’s either cheaper food, reduced price, free food or food that you can share with your neighbours. And we have seen those grow significantly across downloads and monthly active users and sessions.

Seasonality is important for some markets. In Indonesia, the peak daily downloads were usually close to the holidays. From a user acquisition perspective, people were downloading apps to get groceries or food delivered during these holiday times. And that’s an important thing to know as it informs your ad strategy.

We also see extreme weather come into play, which is unfortunately becoming more common around the world. How do F&B apps play a role in getting people what they need when they can’t get out to do it themselves, while ensuring the safety of their staff?

Any barriers to overcome to improve the customer experience?

Brands need to make sure they are talking to the users at the right time and understand how the recommendation engine works. This is what will fuel repeat usage. This could be making sure products they’d like show up quickly when they are looking to place an order or in designing relevant and timely push notifications. The latter can be a hard thing to get right because if you have too many of them, do it too frequently or it’s not targeted enough, then people will start to ignore them as well, similar to “ad fatigue”.

The other factor to consider is how people want to choose how they pay. We see “buy now, pay later” functions being used by grocery delivery apps across the board. We see big players like Atome do well in Southeast Asia across country-specific apps.

Coupons and rewards are another big area to improve, which extends beyond food and drink. But we’ve seen a lot of grocery delivery app users also over-index and leverage a lot of coupon and rewards apps. This is another element of that cost-conscious consumer surfacing again.

Providers such as Starbucks have a digital gift card system. You load money onto that and then you can set up recurring payments that load onto your card in the app.

This is pretty powerful because you’re getting the definitive, recurring payment for consumers which is tied to their loyalty card. When you scan it, you’re going to get those promotional benefits. And then there’s that gamified element – being able to track and celebrate your progress with a free drink, ice cream or sandwich. Ultimately, making it fun and delighting your app users goes a long way to cultivating loyal, repeat customers. I think that’s another big one.

As this sector starts to develop in APAC, what are the key watchouts that marketers need to take note of?

Some sectors require intensive logistics. A lot of ultra-fast players are investing in physical spaces to meet demand to make sure they have staple items in stock to fulfil timely deliveries. For instance, in Australia much of the population is concentrated in three or four big cities, so brands could probably triangulate things decently. But it still is a tricky spot for most players in the space as it can be capital and logistics intensive. I think that’s an industry that’s still in the throes of trying to figure out how to navigate logistics in the effort to achieve profitability in the long run.

While there is consumer behaviour that is showing that people do want things very fast, there is also the sustainability factor and an element of the eco-conscious consumer. This is an opportunity for brands to provide consumers an ability to opt in for a more “green” experience. So maybe instead of having it delivered in 15 minutes in a regular grocery or food delivery app, you can opt to have it delivered on a green route with a cyclist.

The other watchout is around rising fuel costs. I do think that’s something that consumers will take note of soon, especially if the price is passed on to them. We are seeing electric vehicle charging apps grow significantly and correlating very closely with gas prices.