Car-makers like Ford, General Motors and Toyota once ruled the airwaves and print pages, but automotive ad budgets have dwindled over the last decade.

Let me take you back to the heady days of 2007, when the sun was shining and the vibes were good (well, the banks hadn’t yet collapsed). I’d just completed a post-graduate qualification in magazine journalism – in hindsight, arguably a 21st century equivalent of buying a horse and cart in Detroit in 1900 – and was ready to embark on a career reporting on marketing and media.

The past is a foreign country, and they shared content differently back then. The weekly magazine I joined dedicated a single page to all things ‘digital’ (for context, we reserved the same number of column inches for the latest news in sponsorship, design and door-drops). Many of the companies making the news (the usual CPG giants and grocery retailers) remain among the most talked-about advertisers today – but there are a few major exceptions, most notably in the world of automotive.

It’s easy to forget how important car brands were to the health of the ad market. A 15-year-old report by Ad Age lists automotive as the biggest-spending category in the US, having invested $22.2bn in 2006, equivalent to a 22.7% share of total national spend, ahead of personal care (20.0%) and entertainment and media (9.8%). A ranking of the top 20 highest-spending advertisers included no fewer than seven car-makers, led by General Motors (GM) in third place.

Times change, and so has the automotive industry’s place in the global ad market. The brands themselves – from Volkswagen to Toyota – are overwhelmingly still with us, but they have faded from prominence as media fragmented and digital platforms ascended into a dominant position.

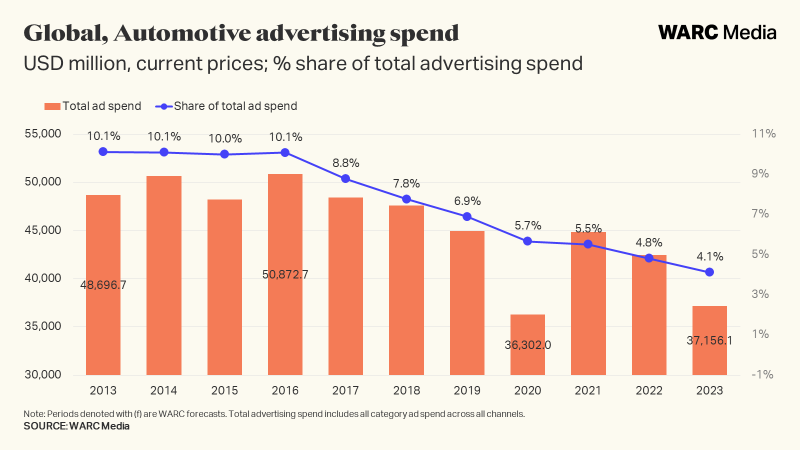

Aside from a post-COVID splurge in 2021, global automotive ad spend has declined every year since 2016. Total investment fell by 5.3% to $42.4bn in 2022, according to WARC Media, and is forecast to decline a further 12.4% in 2023 – by far the biggest contraction in spend anticipated across any product category. A similar pattern of shrinking investment can be seen at an advertiser level with Ford, GM and Nissan.

In the decade since 2013, automotive’s share of total worldwide ad spend has dropped from 10.1% to a forecast 4.1% this year.

Where is the money (not) going?

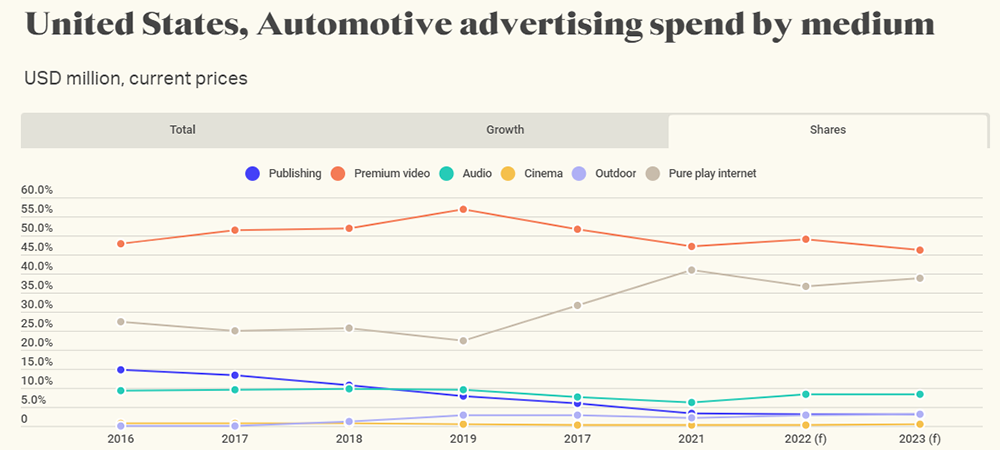

As with many sectors, automotive investment in publishing media has collapsed over the last decade – from more than $8bn in 2016 to less than $2bn in 2022 – while spending on legacy channels like TV, audio and OOH have also declined since pre-pandemic times.

In contrast, spending on digital channels has increased, with the prime beneficiaries being social media (+57.5% in 2021) and search (+51.7%). Among social platforms, Instagram is expected to earn the most from automotive investment in 2023, taking a 30.3% share of social budgets, according to WARC Media.

North America has long been a key market for the car industry – so much so that more than half (56.0%) of all ad investment by car companies will be spent in the US, WARC Media data shows. Thankfully for US media owners, automotive ad spend in that market has held up better than it has at a global level. WARC Media forecasts US automotive ad investment will grow by 7.7% this year to reach $20.8bn, following a 3.8% contraction in 2022.

A key difference in the US market is the continued pre-eminence of video over pure-play internet, despite a huge (+52.6%) increase in spend on channels like search and social in 2021. Premium video is forecast to account for 46.2% of US automotive ad budgets in 2023, while investment in audio media formats is also increasing, driven by growing spend in both local radio and online streaming.

The Elon-phant in the room

There are some good reasons for a recent dip in spending by car companies.

The industry is grappling with the effects of a trio of structural challenges: economic instability and cost of living pressures, unprecedented supply chain disruption resulting from war in Ukraine and cooling relations between China and the West, and a complex shift from combustion engine to electric vehicle (EV) production.

Moreover, Tesla, the most valuable car marque on the planet according to Kantar’s BrandZ index, famously claims to not spend a penny on paid advertising of any kind – a fact which has marketing consultants everywhere trying to figure out how other brands can be more like Tesla.

Tesla’s growth is not simply a question of media hype: its Model Y product was the third biggest seller in the UK last year. In this context, co-founder and CEO Elon Musk’s unwillingness to match Tesla’s share of market with an equivalent share of voice is a pain-point for media owners. One only wonders if Musk’s new-found appreciation for ads as owner of Twitter may prompt a change in approach.

The significant increase in paid search points to another potential issue, namely that car marketers are increasingly focused on performance, and may be dialling back on the creation of future demand. At a time when research consistently shows that younger people in regions like Europe are less enamoured with the idea of car ownership, this is approach carries clear risks.

This may turn out to be transitionary moment, and – revitalised by the popularity of EVs – car companies may push the accelerator pedal on advertising spend to win sales in a new-look personal mobility market. For the time being, however, that former engine of ad spend growth appears to have fallen silent.