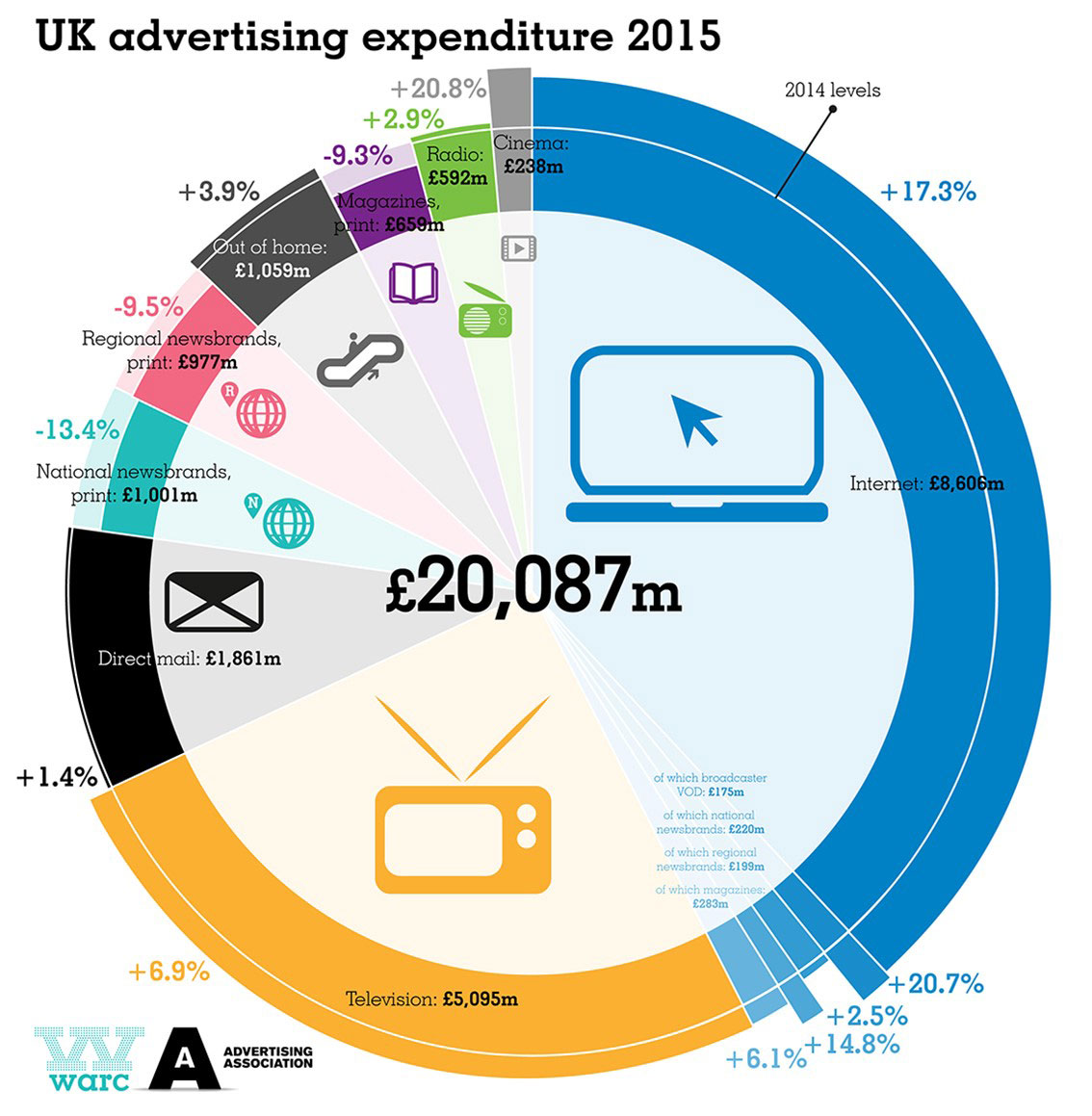

UK advertising expenditure grew at its strongest rate since 2010 last year, with total adspend of £20.1bn marking a 7.5% rise from 2014, according to the latest results from the AA/Warc UK Expenditure Report, released this week.

When comparing this to Warc's international database, we see that of the top ten advertising markets by dollar value, the UK's growth was the second-fastest last year, behind only China.

Further, in real terms (after accounting for inflation), UK adspend increased by 7.4% in 2015. This was the strongest real growth rate since 2000, when the market was recovering from the dotcom crash.

Within last year's headline total, ad expenditure on display formats rose 6.4% to £13.4bn, that for non-recruitment classified (including search) grew 9.9% to £6.2bn, while spend on recruitment advertising dipped 5.3% to £496m. Rising UK employment would normally be associated with increases in recruitment adspend, but the continuing shift from print to digital is unsettling this relationship.

By media, all channels bar print recorded increasing advertising spend in 2015. Cinema, the smallest medium by market size, recorded the highest growth in 2015, with spend rising 20.8% to £238m. The cinema total was buoyed by a strong fourth quarter in which two of the year's highest grossing films, Star Wars: The Force Awakens and SPECTRE, were released. The £90m spent on cinema advertising in Q4 2015 was 22.7% higher than a year previous, and more than the first two quarters of 2014 combined.

Click image to enlarge

Internet

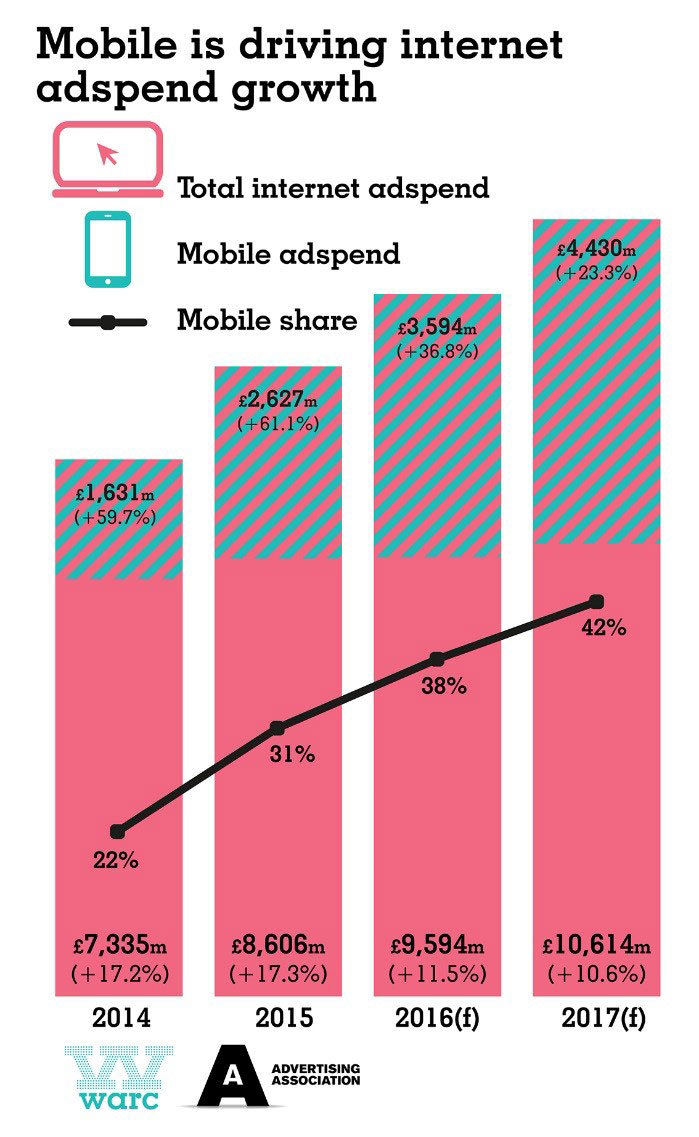

Internet, the largest ad channel in the UK since 2012, recorded adspend growth of 17.3% in 2015, to a total of £8.6bn. This is comfortably the largest total in Europe and ranks third globally, behind the US and China.

Part of the total internet growth was due to the monitoring of a new video format, outstream/in-read, which constitutes video content served outside of social media platforms (including YouTube) in a 'native' style, running a video ad as you scroll down the page reading the content. Spend on this format amounted to £148m in 2015, and removing it from the total removes, in turn, two percentage points from internet's annual growth rate.

However, the vast majority of internet growth – 78% in 2015 – can be ascribed to increasing spend on mobile formats. Mobile adspend leapt 61.1% last year to £2.6bn, a 30.5% share of the internet total. Both mobile display and search recorded adspend of £1.3bn in 2015, representing growth of 59.8% and 63.2% respectively. Interestingly, in the final quarter of 2015, spend on mobile display formats topped that for search for only the second time. This suggests that emerging digital display formats, such as native, video and social, are holding increasingly more sway with marketers.

Within the wider internet total, adspend on video rose 50.9% to £711m, while content and native advertising spend – which includes "advertorials" and ads in social media news feeds – increased by 49.9% to £776m. Spend on social formats, meanwhile, grew 65% to £922m last year, with some £517m of this specifically for mobile.

Click image to enlarge

Television

2015 was also a strong year for Television. Total TV ad revenues, inclusive of spot, sponsorship, product placement, advertiser funded programming, broadcaster VOD and others (including interactive fees, pub TV etc.) rose 7.3% to £5.3bn, the best performance since 2010 and a new adspend high.

Even when removing broadcaster VOD revenues (which are included in the Internet total), TV adspend still recorded its strongest growth rate in five years (+6.9%).

Spot adspend (some 90% of the TV total) grew 6.7% in 2015 to £4.8bn. Spot had a strong second half of the year, with adspend rising 9.6% in Q3 2015 during the UK's hosting of the Rugby World Cup. Fourth quarter adspend then increased by 5.5% from the previous year to reach £1.3bn, the highest three-month total on record.

Industry body Thinkbox noted that growing spend from online businesses helped achieve the record TV total last year. Online businesses were the second-largest product category in 2015, according to Thinkbox, with ad expenditure rising 14% to more than £500m. Facebook, the social media giant, made its first foray onto TV screens with an outlay of £10.8m last year.

Also within the headline TV figure, adspend on broadcaster VOD, including revenues for All 4, ITV Player, Demand 5 and Sky Go, reached £175m in 2015 after growth of 20.7%, while adspend on TV sponsorship rose 5.8% year-on-year to £256m. Both totals are new highs.

Click image to enlarge

Elsewhere, direct mail, the UK's third-largest advertising medium by spend, recorded annual growth for the first time in four years during 2015, with ad expenditure rising 1.4% to £1.9bn. Adspend on radio also grew last year, from a particularly strong 2014. The amount spent to secure radio spots increased by 3.1% to £489m, while branded content also recorded an uptick, of 2.0% to £103m. The radio total of £592m marked a 2.9% rise from 2014 levels.

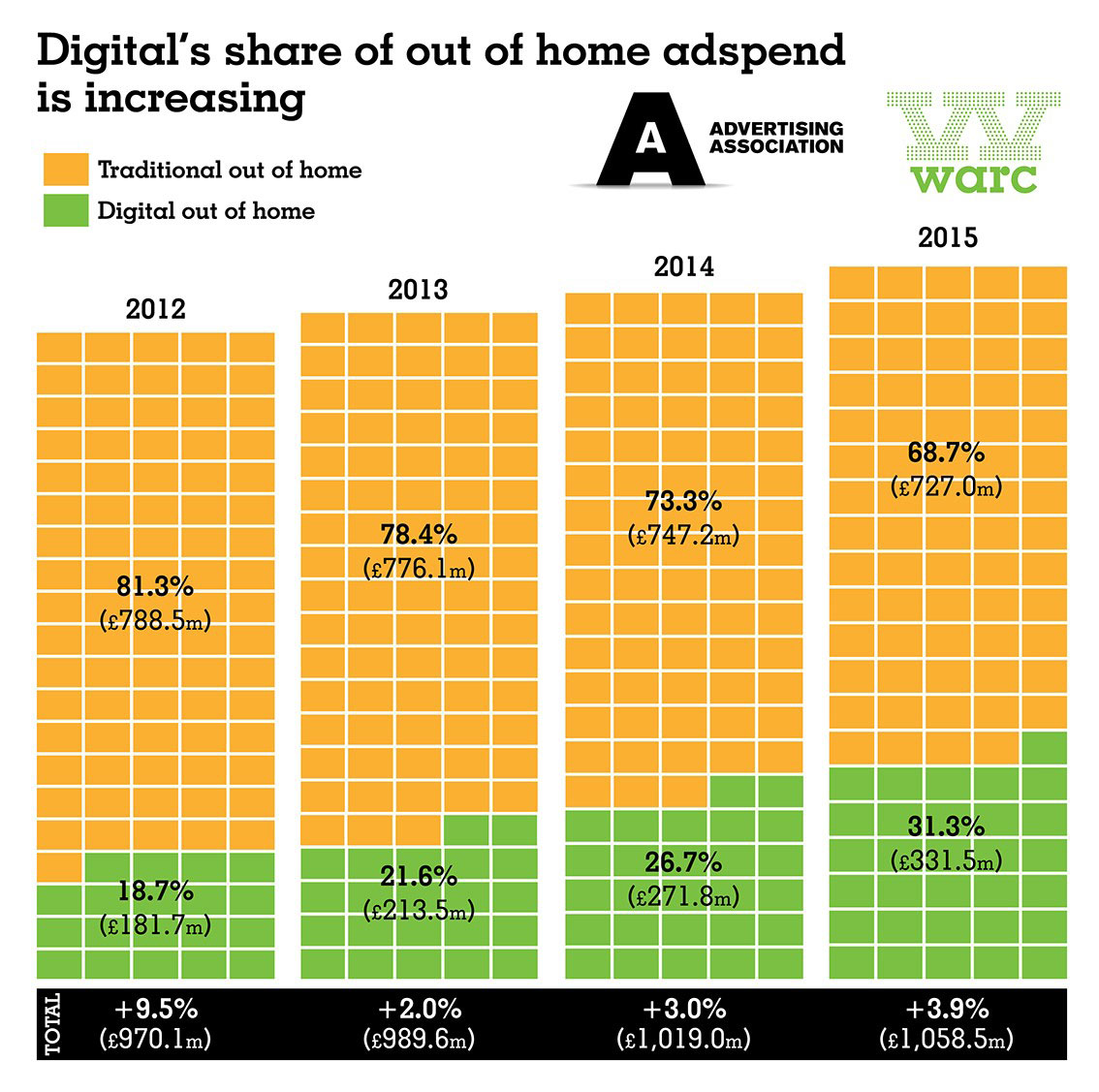

Total out of home adspend grew 3.9% in 2015 to £1.1bn, almost a third (31.3%) of which was specifically for digital panels. Digital is now driving headline growth for the sector, as spend on traditional panels has dipped in each of the last three years. The increasing penetration of digital panels and the impending launch of a new programmatic trading network should support further growth in out of home adspend over the coming years.

Total advertising revenue for newsbrands and magazine brands also contracted in 2015, by 8.7% and 5.2% respectively. Digital growth was unable to offset the steep declines in print adspend last year, though we expect softer falls in the headline total over this year and next.

We forecast healthy growth of 5.5% for UK advertising Expenditure in 2016 and 2017, as many of the emerging trends continue to play out. Official forecasts for UK GDP growth in 2016 have been cut over the recent months and we would normally have reduced our adspend growth forecasts as a result. However, we have balanced these cuts against the continuing and substantial increase in mobile adspend.

We believe advertising spend on social formats will continue to grow apace this year, as marketers mirror media consumption habits. We also expect native/advertorial content to be increasingly utilised by online publishers, partially as a combatant against ad blocking. The Euro 2016 football tournament in June will boost TV spot adspend, and the phasing in of programmatic trade and addressable ad platforms should also provide a fillip for the TV sector at large.

We also believe the UK ad market will reach a major landmark in 2017. In real terms, after accounting for inflation, UK adspend will top its pre-financial crisis level for the first time. This recovery has taken a decade to achieve.