Liquid Death and the drivers behind the NoLo trend | WARC | The Feed

The Feed

Read daily effectiveness insights and the latest marketing news, curated by WARC’s editors.

You didn’t return any results. Please clear your filters.

Liquid Death and the drivers behind the NoLo trend

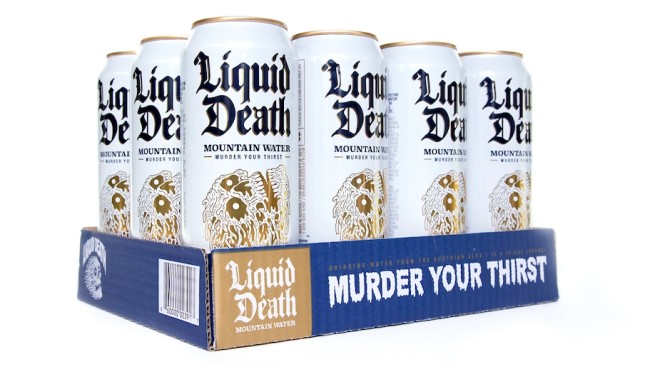

Liquid Death is a canned water company that has marketed its way to a $700m valuation at its latest funding round, exemplifying how a clever brand can meet a deeper trend toward no- and low-alcohol (NoLo) beverages.

Why it matters

Across the world, people are drinking less. Whether that’s because of a growing interest in wellness, because more people want to moderate their alcohol intake, or because it isn’t as cool as it once was, low- or no-alcohol brands are having a moment and some are doing it in very interesting ways. And then there’s a water brand marketing like a beer brand, which is even more interesting.

The bigger picture: a world of moderation

Around the world, the NoLo drinks market is booming; according to IWSR figures for 2021 it is worth a total of $10bn, across 10 major international markets – including the UK, US, and Australia.

- Some brands are reacting to new consumer demands. Treasury Wine Estates, owner of Wolf Blass wines, said this week that it would begin investing heavily into no- and low-alcohol wine following internal consumer research showing that as many as 45% of consumers seek lower or no-alcohol options, especially among under-35s, the Australian Financial Review reports.

- Others seek to smooth the transition. Heineken, for instance, which began to see some success in 2019, has enhanced its alcohol-free option by attempting to “mainstream” the category by getting it into pubs on draught to help the product blend into the occasion.

… and then there’s Liquid Death

Despite its hardcore name, the American brand – that now harbours European ambitions – sells water. That’s right: you can have it still or sparkling or you can have it slightly flavoured, but it’s still water even if it “murders your thirst”.

But its whole thing is quite tongue in cheek, involving humour and punk rock/craft beer aesthetics. It’s a combination that has now resulted in a very serious valuation of $700m at its latest funding round, according to Bloomberg.

It is set to make as much as $130m this year, up 188% from 2021 when it made $45m.

Effectively, the company’s insight was to take a water brand, make it look “fun and unhealthy like beer or an energy drink”, in the words of CEO and former agency creative director Mike Cessario, and sell it online where it began as a DTC brand, in stores, and – crucially – at concerts.

In a commoditised category, the company has shown how potent a brand can be, with $3m of merchandise sales last year, from skateboards to hoodies. According to the company, more than 50% of buyers from its DTC site also attach merchandise to the order.

“When you can actually make revenue off the marketing directly, it kind of means there’s no limit to how much you can do,” Cessario told Modern Retail in January.

In 2020, TechCrunch put it uncharitably when it said the joke was on consumers (at this point, the brand had raised a total of $23m), but the story goes to the heart of what a brand is and does in the CPG category. After all, what’s the point of branding if not to build regard, recognition, and, ultimately, charge more than your undifferentiated competitors. It’s a lesson worth noting.

Sourced from Bloomberg, WARC, Australian Financial Review, Modern Retail, The Drinks Business, VICE

Email this content